Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- FS ModelDocument13 pagesFS Modelalfx216Pas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Buy Your First HouseDocument13 pagesBuy Your First HouseAlonzo AventsPas encore d'évaluation

- Quicknotes in Income TaxDocument13 pagesQuicknotes in Income TaxTrelle DiazPas encore d'évaluation

- Comparative Analysis 8424 and 10963Document31 pagesComparative Analysis 8424 and 10963Rizza Angela Mangalleno100% (2)

- Income Taxes For CorporationsDocument35 pagesIncome Taxes For CorporationsKurt SoriaoPas encore d'évaluation

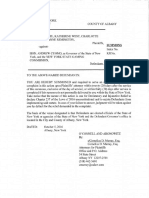

- AttyAffirmation For Omnibus Motion - FinalDocument4 pagesAttyAffirmation For Omnibus Motion - FinalJon CampbellPas encore d'évaluation

- Tax Return BillDocument4 pagesTax Return BillJon CampbellPas encore d'évaluation

- Opinion Re Legislative LawDocument4 pagesOpinion Re Legislative LawCasey SeilerPas encore d'évaluation

- Morabito DecisionDocument3 pagesMorabito DecisionJon CampbellPas encore d'évaluation

- Senate Dems Analysis of Lulus Paid To Non-Committee Chairs.Document5 pagesSenate Dems Analysis of Lulus Paid To Non-Committee Chairs.liz_benjamin6490Pas encore d'évaluation

- NYS Department of Health Aca Repeal AnalysisDocument2 pagesNYS Department of Health Aca Repeal AnalysisMatthew HamiltonPas encore d'évaluation

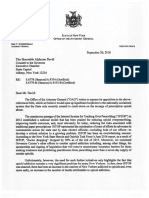

- Schneiderman Proposed Complaint For ACLU Trump Executive Order LawsuitDocument33 pagesSchneiderman Proposed Complaint For ACLU Trump Executive Order LawsuitMatthew HamiltonPas encore d'évaluation

- Chamber of CommerceDocument1 pageChamber of CommerceRyan WhalenPas encore d'évaluation

- Sexual Offense Evidence Kit Inventory Report 3-1-17Document26 pagesSexual Offense Evidence Kit Inventory Report 3-1-17Jon Campbell100% (1)

- Schneiderman Proposed Complaint For ACLU Trump Executive Order LawsuitDocument33 pagesSchneiderman Proposed Complaint For ACLU Trump Executive Order LawsuitMatthew HamiltonPas encore d'évaluation

- FHWA DOT LettersDocument4 pagesFHWA DOT LettersJon CampbellPas encore d'évaluation

- Gaddy SummonsDocument2 pagesGaddy SummonsJon CampbellPas encore d'évaluation

- Acacia v. SUNY RF Et AlDocument12 pagesAcacia v. SUNY RF Et AlJon CampbellPas encore d'évaluation

- Cuomo StatementDocument5 pagesCuomo StatementJon CampbellPas encore d'évaluation

- FOIA 2017 0037 Response Letter 15 19Document5 pagesFOIA 2017 0037 Response Letter 15 19Jon CampbellPas encore d'évaluation

- US v. Percoco Et Al Indictment - Foreperson SignedDocument36 pagesUS v. Percoco Et Al Indictment - Foreperson SignedNick ReismanPas encore d'évaluation

- Orange County CaseDocument42 pagesOrange County CaseJon CampbellPas encore d'évaluation

- US v. Kang and Kelley IndictmentDocument27 pagesUS v. Kang and Kelley IndictmentJon CampbellPas encore d'évaluation

- Stronger Neighborhoods PAC/SerinoDocument2 pagesStronger Neighborhoods PAC/SerinoJon CampbellPas encore d'évaluation

- FHWA - Presentation - NY SignsDocument112 pagesFHWA - Presentation - NY SignsJon Campbell100% (1)

- FHWA Nov 2016 LetterDocument2 pagesFHWA Nov 2016 LetterJon CampbellPas encore d'évaluation

- NY DFS LawsuitDocument77 pagesNY DFS LawsuitJon CampbellPas encore d'évaluation

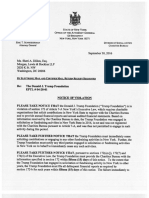

- Trump Foundation Notice of Violation 9-30-16Document2 pagesTrump Foundation Notice of Violation 9-30-16Cristian Farias100% (1)

- Stronger Neighborhoods PAC/SerinoDocument2 pagesStronger Neighborhoods PAC/SerinoJon CampbellPas encore d'évaluation

- Stronger Neighborhoods PAC/LatimerDocument2 pagesStronger Neighborhoods PAC/LatimerJon CampbellPas encore d'évaluation

- Skelos Opening Brief v17 - SignedDocument70 pagesSkelos Opening Brief v17 - SignedJon CampbellPas encore d'évaluation

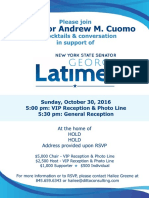

- Latimer Oct 30 EventDocument2 pagesLatimer Oct 30 EventJon CampbellPas encore d'évaluation

- DiNapoli MTA ReportDocument8 pagesDiNapoli MTA ReportJon CampbellPas encore d'évaluation

- New York State Offshore Wind BlueprintDocument24 pagesNew York State Offshore Wind BlueprintJon CampbellPas encore d'évaluation

- 2016 9 20 Letter To A David Re ISTOPDocument3 pages2016 9 20 Letter To A David Re ISTOPJon CampbellPas encore d'évaluation

- C.A IPCC May 2008 Tax SolutionsDocument13 pagesC.A IPCC May 2008 Tax SolutionsAkash GuptaPas encore d'évaluation

- The Effects of Education On CrimeDocument12 pagesThe Effects of Education On CrimeMicaela FORSCHBERG CASTORINOPas encore d'évaluation

- Article Vi: The Legislative DepartmentDocument4 pagesArticle Vi: The Legislative DepartmentJun MarPas encore d'évaluation

- Taxes During the Spanish Period: From Tribute to Cedula TaxDocument21 pagesTaxes During the Spanish Period: From Tribute to Cedula TaxJannah Fate100% (1)

- Assessment 1 - Written or Oral QuestionsDocument7 pagesAssessment 1 - Written or Oral Questionswilson garzonPas encore d'évaluation

- Bài tập trên lớp buổi 11Document4 pagesBài tập trên lớp buổi 11Thuỳ AnPas encore d'évaluation

- Gasbill 2864608891 202307 20230721180052Document1 pageGasbill 2864608891 202307 20230721180052Shahhussain HussainPas encore d'évaluation

- WINRO154 BudgetLetterRequest - Semi MonthlyCashAssistanceBudgetCalculation - SNAPBudgetCalculationForCA&CA SSICases 585277954Document6 pagesWINRO154 BudgetLetterRequest - Semi MonthlyCashAssistanceBudgetCalculation - SNAPBudgetCalculationForCA&CA SSICases 585277954schwartzdaven7Pas encore d'évaluation

- Atty Lapuz (100-112) DigestDocument4 pagesAtty Lapuz (100-112) DigestRAINBOW AVALANCHE100% (1)

- Dimma HoneyDocument9 pagesDimma HoneyAnonymous h2hxB1Pas encore d'évaluation

- ITB NotesDocument84 pagesITB NotesSadiaPas encore d'évaluation

- Dissecting The India Hospitality IndustryDocument14 pagesDissecting The India Hospitality IndustrySwapnesh R JainPas encore d'évaluation

- Using ReceivingDocument94 pagesUsing ReceivingPavlina StoqnovaPas encore d'évaluation

- Plan Fiscal Del CRIMDocument34 pagesPlan Fiscal Del CRIMEl Nuevo DíaPas encore d'évaluation

- Uniform CPA Examination. Questions and Unofficial Answers 1989 N PDFDocument97 pagesUniform CPA Examination. Questions and Unofficial Answers 1989 N PDFJeremie RealinoPas encore d'évaluation

- DT - Volume 1 - June 22& Dec 22 - CS Executive - CA Saumil ManglaniDocument281 pagesDT - Volume 1 - June 22& Dec 22 - CS Executive - CA Saumil ManglaniIshani MukherjeePas encore d'évaluation

- Micro 2013 ZA QPDocument8 pagesMicro 2013 ZA QPSathis JayasuriyaPas encore d'évaluation

- 1601 CDocument16 pages1601 CROGELIO QUIAZON100% (1)

- Priyanka RajputDocument48 pagesPriyanka RajputNitinAgnihotriPas encore d'évaluation

- The Economic of Cloud ComputingDocument17 pagesThe Economic of Cloud ComputingLouise ANPas encore d'évaluation

- MH 2223 90443 PDFDocument6 pagesMH 2223 90443 PDFHarsh PatelPas encore d'évaluation

- Central & State RelationsDocument8 pagesCentral & State RelationsVISWA TEJA NemaliPas encore d'évaluation

- PCU Capstone Project Analyzes Demand for Job Order Contact Tracers at BIRDocument3 pagesPCU Capstone Project Analyzes Demand for Job Order Contact Tracers at BIRdaniela riveraPas encore d'évaluation

- Risk Analysis ExampleDocument8 pagesRisk Analysis ExampleRyan SooknarinePas encore d'évaluation

- Municipalities & Cities Reclaim Foreshore LandsDocument2 pagesMunicipalities & Cities Reclaim Foreshore LandsIELTSPas encore d'évaluation