Vous aimerez peut-être aussi

- Guide To Trinidad VATDocument25 pagesGuide To Trinidad VATJerome DanielPas encore d'évaluation

- PAYE BookletDocument19 pagesPAYE BookletIndira HPas encore d'évaluation

- TD1 Forms-2006 Amended Income Tax Form Trinidad and TobagoDocument3 pagesTD1 Forms-2006 Amended Income Tax Form Trinidad and TobagowhatdacowcowPas encore d'évaluation

- PAYE BookletDocument19 pagesPAYE BookletGarcia LeeAnnPas encore d'évaluation

- Income Tax Deduction TableDocument19 pagesIncome Tax Deduction TablekeronsPas encore d'évaluation

- 004 - TR (14) 39 Confirmed Minute 3180Document3 pages004 - TR (14) 39 Confirmed Minute 3180deadstar1Pas encore d'évaluation

- Resetting T&T's Economy - A Sustainable Response To The Covid-19 Crisis REVISED Version PDFDocument22 pagesResetting T&T's Economy - A Sustainable Response To The Covid-19 Crisis REVISED Version PDFPearce RobinsonPas encore d'évaluation

- Trinidad and Tobago Emolument Income Tax 2012Document5 pagesTrinidad and Tobago Emolument Income Tax 2012Anand RockerPas encore d'évaluation

- 79.02 - Trinidad and Tobago Central Bank ActDocument80 pages79.02 - Trinidad and Tobago Central Bank ActOilmanGHPas encore d'évaluation

- 004 - TR (15) 19 Confirmed Minute 1548Document3 pages004 - TR (15) 19 Confirmed Minute 1548deadstar1Pas encore d'évaluation

- Nigeria Withholding Tax GAZETTE 2015Document4 pagesNigeria Withholding Tax GAZETTE 2015ahmad bPas encore d'évaluation

- Trinidad & Tobago TaxDocument26 pagesTrinidad & Tobago TaxHaydn Dunn100% (4)

- Tenancy Fact Sheet Access and PrivacyDocument2 pagesTenancy Fact Sheet Access and PrivacySteve HolleyPas encore d'évaluation

- Surveying The Scene WebDocument50 pagesSurveying The Scene WebRossana CairaPas encore d'évaluation

- Beer Duty Return by Keyconsulting UKDocument2 pagesBeer Duty Return by Keyconsulting UKKeyconsulting UKPas encore d'évaluation

- Application For Extension of Landing Certificate Trinidad and TobagoDocument2 pagesApplication For Extension of Landing Certificate Trinidad and TobagoSusana Zambrana0% (1)

- Certificate of Environmental Clearance in Trinidad & TobagoDocument6 pagesCertificate of Environmental Clearance in Trinidad & TobagoHaydn Dunn100% (2)

- BIR Form 1701QDocument2 pagesBIR Form 1701QfileksPas encore d'évaluation

- ITF 12C Income Tax Self Assessment ReturnDocument4 pagesITF 12C Income Tax Self Assessment ReturnTavongasheMaddTMagwati100% (1)

- TRA Taxes at Glance - 2016-17Document22 pagesTRA Taxes at Glance - 2016-17Timothy Rogatus67% (3)

- List of Attorneys TT - 2Document16 pagesList of Attorneys TT - 2Nekeisha BishopPas encore d'évaluation

- Oregon Public Employees Retirement (PERS) 2007Document108 pagesOregon Public Employees Retirement (PERS) 2007BiloxiMarxPas encore d'évaluation

- Return For Provisional Tax PaymentDocument2 pagesReturn For Provisional Tax PaymentByron KanengoniPas encore d'évaluation

- Tutorial 9 - PIT1-Summer 2023-Sample AnswerDocument4 pagesTutorial 9 - PIT1-Summer 2023-Sample Answerkien tran100% (1)

- Total Rewards For Civil Servants - WB - MukherjeeDocument6 pagesTotal Rewards For Civil Servants - WB - MukherjeeAngel Tejeda MorenoPas encore d'évaluation

- 2316 JAKEDocument1 page2316 JAKEJM HernandezPas encore d'évaluation

- Overview of TDS: by C.A. Manish JathliyaDocument21 pagesOverview of TDS: by C.A. Manish JathliyaHasan Babu KothaPas encore d'évaluation

- Objective Type Questions and Answers On Central ExciseDocument5 pagesObjective Type Questions and Answers On Central ExciseGayathri Prasad Gayathri0% (2)

- Taxation (Bs211)Document348 pagesTaxation (Bs211)RewardMatururePas encore d'évaluation

- 1701qjuly2008 (ENCS)Document6 pages1701qjuly2008 (ENCS)alvie_budPas encore d'évaluation

- Oregon Public Employees Retirement (PERS) 2001Document74 pagesOregon Public Employees Retirement (PERS) 2001BiloxiMarxPas encore d'évaluation

- Bir Forms PDFDocument4 pagesBir Forms PDFgaryPas encore d'évaluation

- Offences Under The The Motor Vehicles and Road Traffic RegulationsDocument2 pagesOffences Under The The Motor Vehicles and Road Traffic Regulationsjamille85100% (4)

- 62983rmo 5-2012Document14 pages62983rmo 5-2012Mark Dennis JovenPas encore d'évaluation

- DT RevisionDocument133 pagesDT RevisionharshallahotPas encore d'évaluation

- 1702 July 08Document7 pages1702 July 08Jchelle Lustre DeligeroPas encore d'évaluation

- Vat Returns Manual 2021Document25 pagesVat Returns Manual 2021mactechPas encore d'évaluation

- Tax Burden UKDocument13 pagesTax Burden UKArturas GumuliauskasPas encore d'évaluation

- Pay As You Go (Payg) WithholdingDocument70 pagesPay As You Go (Payg) WithholdingliamPas encore d'évaluation

- Citn New Professional Syllabus - Income TaxDocument214 pagesCitn New Professional Syllabus - Income Taxtwweettybird100% (2)

- History of Taxation in EthiopiaDocument6 pagesHistory of Taxation in EthiopiaEdlamu Alemie100% (1)

- Income Tax Study PackDocument68 pagesIncome Tax Study PackKempton MurimiPas encore d'évaluation

- Procedure of Appeal To The Income Tax Appellate Authority in BangladeshDocument4 pagesProcedure of Appeal To The Income Tax Appellate Authority in BangladeshMasum GaziPas encore d'évaluation

- Renewal Application Form For Trinidad and Tobago PassportDocument2 pagesRenewal Application Form For Trinidad and Tobago PassportLorinLakePas encore d'évaluation

- Income Tax Regulation No 78 2002Document20 pagesIncome Tax Regulation No 78 2002buffoxxx100% (1)

- USD Tax Tables 2022Document1 pageUSD Tax Tables 2022Godfrey MakurumurePas encore d'évaluation

- Tax Form 2013 (Trinidad)Document5 pagesTax Form 2013 (Trinidad)Natasha ThomasPas encore d'évaluation

- GSTDocument11 pagesGSTvamshi9686Pas encore d'évaluation

- CashFlow Projection MASIYADocument5 pagesCashFlow Projection MASIYAClyton MusipaPas encore d'évaluation

- Workshop Case Study: Business Activity StatementDocument21 pagesWorkshop Case Study: Business Activity StatementcollingwoodPas encore d'évaluation

- DRC VAT Training CAs Day 1-2Document40 pagesDRC VAT Training CAs Day 1-2iftekharul alam100% (1)

- Cta 2D CV 09224 M 2019feb12 AssDocument17 pagesCta 2D CV 09224 M 2019feb12 AssMelan YapPas encore d'évaluation

- Ir8a (M) 2010Document1 pageIr8a (M) 2010gk9f5e6ho1owcldxPas encore d'évaluation

- Practice Test - Financial ManagementDocument6 pagesPractice Test - Financial Managementelongoria278100% (1)

- Valencia FBT Chapter 6 5th EditionDocument8 pagesValencia FBT Chapter 6 5th EditionJacob AcostaPas encore d'évaluation

- Chapter 3Document8 pagesChapter 3lijijiw23Pas encore d'évaluation

- Ai Tax Matters Tax Basis Capital Account ReportingDocument1 pageAi Tax Matters Tax Basis Capital Account ReportingAshley OweyaPas encore d'évaluation

- Tax FinalDocument7 pagesTax FinalDinosaur KoreanPas encore d'évaluation

- Topic 5 GST Tute SolutionsDocument4 pagesTopic 5 GST Tute SolutionsHA Research ConsultancyPas encore d'évaluation

- Self Employed: TRN Requirements For Sole ProprietorsDocument14 pagesSelf Employed: TRN Requirements For Sole ProprietorsAnonymous imWQ1y63Pas encore d'évaluation

- Honey An OverviewDocument9 pagesHoney An Overviewstephen_debique9455Pas encore d'évaluation

- Vehicular Emissions TrinidadDocument4 pagesVehicular Emissions Trinidadstephen_debique9455Pas encore d'évaluation

- AD Biogas News February 2014 FinalDocument40 pagesAD Biogas News February 2014 Finalstephen_debique9455Pas encore d'évaluation

- Ch2 Spreadsheet ExerciseDocument1 pageCh2 Spreadsheet Exercisestephen_debique9455Pas encore d'évaluation

- IT Concepts Course OutlineDocument26 pagesIT Concepts Course Outlinejohanan_tothPas encore d'évaluation

- The Silver Dirham HSP 2012Document21 pagesThe Silver Dirham HSP 2012stephen_debique9455Pas encore d'évaluation

- InkscapeDocument152 pagesInkscapesaif_alwaysPas encore d'évaluation

- Open AdviceDocument310 pagesOpen Advicestephen_debique9455Pas encore d'évaluation

- Syl5213 08Document11 pagesSyl5213 08stephen_debique9455Pas encore d'évaluation

- DIY Two Bucket EarthBox Sub Irrigated PlanterDocument1 pageDIY Two Bucket EarthBox Sub Irrigated Planterstephen_debique9455Pas encore d'évaluation

- Cocunut Wood FaodocDocument42 pagesCocunut Wood Faodocstephen_debique9455Pas encore d'évaluation

- Mark T. Brown Mtb@ufl - Edu: Modeling For All Scales PDF Handouts From InstructorDocument4 pagesMark T. Brown Mtb@ufl - Edu: Modeling For All Scales PDF Handouts From Instructorstephen_debique9455Pas encore d'évaluation

- Iarp AppDocument2 pagesIarp Appstephen_debique9455Pas encore d'évaluation

- Energy Beginners GuideDocument21 pagesEnergy Beginners Guidestephen_debique9455Pas encore d'évaluation

- Budget Circular No 2018 4 PDFDocument245 pagesBudget Circular No 2018 4 PDFJoey Villas MaputiPas encore d'évaluation

- EDI 820 SpecificationDocument25 pagesEDI 820 SpecificationAtulWalvekarPas encore d'évaluation

- The Cost of Capital: Sources of Capital Component Costs Wacc Adjusting For Flotation Costs Adjusting For RiskDocument37 pagesThe Cost of Capital: Sources of Capital Component Costs Wacc Adjusting For Flotation Costs Adjusting For RiskMohammed MiftahPas encore d'évaluation

- HeaderDocument3 pagesHeaderSeñar, Lorrie Jaye C.Pas encore d'évaluation

- Feasibility Study and Risk AssesmentDocument6 pagesFeasibility Study and Risk AssesmentSanjayPas encore d'évaluation

- Rate Rebasing Concepts For Public Consultation, MWSSDocument13 pagesRate Rebasing Concepts For Public Consultation, MWSSImperator FuriosaPas encore d'évaluation

- 01 - Assignment 2 - Group Case Analysis - Written ReportDocument2 pages01 - Assignment 2 - Group Case Analysis - Written ReportYogenDran SuraskumarPas encore d'évaluation

- Completing The Audit: ©2006 Prentice Hall Business Publishing, Auditing 11/e, Arens/Beasley/ElderDocument41 pagesCompleting The Audit: ©2006 Prentice Hall Business Publishing, Auditing 11/e, Arens/Beasley/ElderJohn BryanPas encore d'évaluation

- Tutorial Letter 102/3/2020: Forms of Business EnterprisesDocument15 pagesTutorial Letter 102/3/2020: Forms of Business EnterprisesXolisaPas encore d'évaluation

- SPMPDocument20 pagesSPMPÇoktiklananlar TiklananlarPas encore d'évaluation

- Curriculum - Rice MillingDocument32 pagesCurriculum - Rice MillingRiya PanjwaniPas encore d'évaluation

- Accreditation Is Not:: Benefits of Accreditation To The Accredited Conformity Assessment BodyDocument5 pagesAccreditation Is Not:: Benefits of Accreditation To The Accredited Conformity Assessment BodyFanilo RazafindralamboPas encore d'évaluation

- PM4DEV Project Management Glossary of TermsDocument26 pagesPM4DEV Project Management Glossary of TermsRaj PPas encore d'évaluation

- 461 110 Falk Torus Elastomeric Coupling CatalogDocument20 pages461 110 Falk Torus Elastomeric Coupling CatalogLazzarus Az GunawanPas encore d'évaluation

- June 2015 QP - Paper 1 Edexcel Economics IGCSEDocument24 pagesJune 2015 QP - Paper 1 Edexcel Economics IGCSEShibraj DebPas encore d'évaluation

- BBA Admin & Finance Ahmed-Yasin Hassan Mohamed ObjectiveDocument4 pagesBBA Admin & Finance Ahmed-Yasin Hassan Mohamed ObjectiveAhmed-Yasin Hassan MohamedPas encore d'évaluation

- The Measurement of Service Quality With Servqual For Different Domestic Airline Firms in TurkeyDocument12 pagesThe Measurement of Service Quality With Servqual For Different Domestic Airline Firms in TurkeySanjeev PradhanPas encore d'évaluation

- Case Study On Business Model Adopted by The Pogo Travels: Abu Sufiyan 151GCMD006 R V Institute of ManagementDocument12 pagesCase Study On Business Model Adopted by The Pogo Travels: Abu Sufiyan 151GCMD006 R V Institute of ManagementSUFIYANPas encore d'évaluation

- Business Strategies Marketing Programs at 3MDocument3 pagesBusiness Strategies Marketing Programs at 3MHarshPas encore d'évaluation

- Management Accounting Summer 20091Document18 pagesManagement Accounting Summer 20091MahmozPas encore d'évaluation

- Plant Layout and Location DecisionsDocument52 pagesPlant Layout and Location DecisionsAEHYUN YENVYPas encore d'évaluation

- Book Condensation: Stay Hungry Stay FoolishDocument12 pagesBook Condensation: Stay Hungry Stay FoolishAardityam SharmaPas encore d'évaluation

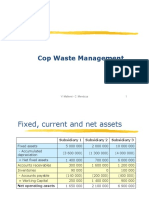

- Cop Waste Management SolutionDocument5 pagesCop Waste Management SolutionPaul GhanimehPas encore d'évaluation

- Human Resource PlanningDocument16 pagesHuman Resource PlanningSiddharth Jain100% (1)

- Impact of Digitalization On Procurement The Case of Robotic Process AutomationDocument11 pagesImpact of Digitalization On Procurement The Case of Robotic Process AutomationNassMezPas encore d'évaluation

- Chapter 18 ControllingDocument24 pagesChapter 18 ControllingAsad Uz Jaman100% (2)

- Templates For Seminar - Mav1Document43 pagesTemplates For Seminar - Mav1Jaymar RegalaPas encore d'évaluation

- Confidential Private Placement Memorandum: Offering of Preferred Limited Liability Company InterestsDocument99 pagesConfidential Private Placement Memorandum: Offering of Preferred Limited Liability Company Interestsapi-544985744100% (1)

- A Project Report ON "Customer Satisfaction in Nokia": Bachelor of Business Administration (Banking & Insurance)Document39 pagesA Project Report ON "Customer Satisfaction in Nokia": Bachelor of Business Administration (Banking & Insurance)Navneet TyagiPas encore d'évaluation

- Performance ApprisalDocument7 pagesPerformance ApprisalSHERMIN AKTHER RUMAPas encore d'évaluation

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!D'EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Évaluation : 4.5 sur 5 étoiles4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindD'EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindÉvaluation : 5 sur 5 étoiles5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)D'EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (13)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineD'EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlinePas encore d'évaluation

- Getting to Yes: How to Negotiate Agreement Without Giving InD'EverandGetting to Yes: How to Negotiate Agreement Without Giving InÉvaluation : 4 sur 5 étoiles4/5 (652)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesD'EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesPas encore d'évaluation

- Controllership: The Work of the Managerial AccountantD'EverandControllership: The Work of the Managerial AccountantPas encore d'évaluation

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)D'EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Évaluation : 4 sur 5 étoiles4/5 (33)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyD'EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyÉvaluation : 4.5 sur 5 étoiles4.5/5 (37)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsD'EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsPas encore d'évaluation

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsD'EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditD'EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditÉvaluation : 5 sur 5 étoiles5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItD'EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItÉvaluation : 5 sur 5 étoiles5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)D'EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Évaluation : 4.5 sur 5 étoiles4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelD'Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelPas encore d'évaluation

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessD'EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessÉvaluation : 4.5 sur 5 étoiles4.5/5 (28)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsD'EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsÉvaluation : 4 sur 5 étoiles4/5 (7)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetD'EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetPas encore d'évaluation

- Financial Accounting For Dummies: 2nd EditionD'EverandFinancial Accounting For Dummies: 2nd EditionÉvaluation : 5 sur 5 étoiles5/5 (10)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyD'EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyÉvaluation : 5 sur 5 étoiles5/5 (1)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookD'EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookÉvaluation : 5 sur 5 étoiles5/5 (4)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCD'EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCÉvaluation : 5 sur 5 étoiles5/5 (1)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookD'EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookPas encore d'évaluation