Vous aimerez peut-être aussi

- 2016 Merrill Taxes PDFDocument8 pages2016 Merrill Taxes PDFholymolyPas encore d'évaluation

- Three Statement Financial ModelingDocument13 pagesThree Statement Financial ModelingJack Jacinto100% (1)

- Taxation Ii Atty. Deborah S. Acosta-Cajustin: Over But Not Over The Tax Shall Be Plus of The Excess OverDocument42 pagesTaxation Ii Atty. Deborah S. Acosta-Cajustin: Over But Not Over The Tax Shall Be Plus of The Excess OverRodel Cadorniga Jr.Pas encore d'évaluation

- MBA in Financial ManagementDocument14 pagesMBA in Financial Managementedmosdigitex1485Pas encore d'évaluation

- A Study On Dividend PolicyDocument75 pagesA Study On Dividend PolicyVeera Bhadra Chary ChPas encore d'évaluation

- Dividend PolicyDocument7 pagesDividend PolicyImran AhsanPas encore d'évaluation

- DD Icici UppalDocument14 pagesDD Icici Uppalferoz khanPas encore d'évaluation

- Up Land LawsDocument22 pagesUp Land LawsLakshit100% (1)

- Gitman c14 SG 13geDocument13 pagesGitman c14 SG 13gekarim100% (3)

- Project On Impact of Dividends PolicyDocument45 pagesProject On Impact of Dividends Policyarjunmba119624100% (1)

- Deductions From Gross Income Part 2 Illustrative ProblemsDocument2 pagesDeductions From Gross Income Part 2 Illustrative ProblemsJohn Rich GamasPas encore d'évaluation

- Dividend PoliciesDocument26 pagesDividend PoliciesMd SufianPas encore d'évaluation

- Gold and Au Bars Trading Full Corporate Offer To Sell - (Fco-S)Document9 pagesGold and Au Bars Trading Full Corporate Offer To Sell - (Fco-S)Fantania Berry100% (3)

- Dividend PolicyDocument23 pagesDividend Policyh3llrazr100% (1)

- Tax Reviewer VitugDocument6 pagesTax Reviewer VitugMis DeePas encore d'évaluation

- Capital Structure and Dividend PolicyDocument25 pagesCapital Structure and Dividend PolicySarah Mae SudayanPas encore d'évaluation

- Project On HDFC LoansDocument61 pagesProject On HDFC LoansPallavi80% (15)

- Impact of Dividend Policy On A Firm PerformanceDocument11 pagesImpact of Dividend Policy On A Firm PerformanceMuhammad AnasPas encore d'évaluation

- Chapter-II Literature ReviewDocument32 pagesChapter-II Literature Reviewbikash ranaPas encore d'évaluation

- Background On DividendsDocument3 pagesBackground On DividendsGustafaGovachefMotivati0% (1)

- Determinants of Dividend Policy: Evidence From GCC MarketDocument13 pagesDeterminants of Dividend Policy: Evidence From GCC MarketeferemPas encore d'évaluation

- Dividend Policy AfmDocument10 pagesDividend Policy AfmPooja NagPas encore d'évaluation

- DEVIDEND DICISION... HDFC Bank-2015Document64 pagesDEVIDEND DICISION... HDFC Bank-2015Tanvir KhanPas encore d'évaluation

- A Critical Analysis On The Impact of Dividend Policy On The Value of The FirmDocument95 pagesA Critical Analysis On The Impact of Dividend Policy On The Value of The Firmnaz100% (3)

- FinmanDocument7 pagesFinmanNHEMIA ELEVENCIONADOPas encore d'évaluation

- Whatever Dividend Policy A Company AdoptsDocument4 pagesWhatever Dividend Policy A Company Adoptsrobhanson90Pas encore d'évaluation

- Discuss The Relevance of Dividend Policy in Financial Decision MakingDocument6 pagesDiscuss The Relevance of Dividend Policy in Financial Decision MakingMichael NyamutambwePas encore d'évaluation

- Dividend Policy AssignmentDocument8 pagesDividend Policy Assignmentgeetikag2018Pas encore d'évaluation

- DividendDocument30 pagesDividendFaruqPas encore d'évaluation

- Financial Theory EssayDocument7 pagesFinancial Theory EssayHuỳnh Ngọc TuyềnPas encore d'évaluation

- Assignment Pengurusan Kewangan 2Document13 pagesAssignment Pengurusan Kewangan 2william tangPas encore d'évaluation

- Subba ReddyDocument47 pagesSubba Reddyankitjaipur0% (1)

- Dividend Policy As Strategic Tool of Financing in Public Firms: Evidence From NigeriaDocument24 pagesDividend Policy As Strategic Tool of Financing in Public Firms: Evidence From Nigeriay_378602342Pas encore d'évaluation

- Submitted For: Course Title: Course CodeDocument15 pagesSubmitted For: Course Title: Course CodeDedar HossainPas encore d'évaluation

- Dividend Policy of Indian Corporate FirmsDocument19 pagesDividend Policy of Indian Corporate FirmsRoads Sub Division-I,PuriPas encore d'évaluation

- Dividend PolicyDocument8 pagesDividend PolicyToufiq AmanPas encore d'évaluation

- Dividend Policy A Comparative Study of UK and Bangladesh Based CompaniesDocument16 pagesDividend Policy A Comparative Study of UK and Bangladesh Based CompaniesMehedi HasanPas encore d'évaluation

- Dividend and Valuation PolicyDocument7 pagesDividend and Valuation Policyjeremie123Pas encore d'évaluation

- Financial Management: TO, Faridha.RDocument23 pagesFinancial Management: TO, Faridha.RSrinivasan SrinivasanPas encore d'évaluation

- Relationship Between Dividend Policy and Corporate Financial PerformanceDocument58 pagesRelationship Between Dividend Policy and Corporate Financial PerformanceRamalan AbdulmalikPas encore d'évaluation

- Dividend Policy: Chapter ObjectivesDocument2 pagesDividend Policy: Chapter ObjectivesMundixx TichaPas encore d'évaluation

- "Dividend Decision": Synopsis OnDocument14 pages"Dividend Decision": Synopsis Onferoz khanPas encore d'évaluation

- Research Papers Dividend Policy TheoriesDocument7 pagesResearch Papers Dividend Policy Theoriesgahezopizez2100% (1)

- Yu 2011Document15 pagesYu 2011atktaouPas encore d'évaluation

- Dividend TheriesDocument7 pagesDividend Theriesluciferofhell1969Pas encore d'évaluation

- Dividend Analysis at India Bulls: Project Report ON " "Document77 pagesDividend Analysis at India Bulls: Project Report ON " "Sankar BukkapatnamPas encore d'évaluation

- Chapter 14-1Document73 pagesChapter 14-1Naeemullah baigPas encore d'évaluation

- Dividend Policy: By:By Group 5: Aayush Kumar Lewis Francis Jasneet Saivenkat Ritika BhallaDocument21 pagesDividend Policy: By:By Group 5: Aayush Kumar Lewis Francis Jasneet Saivenkat Ritika BhallaMãñú PhîlïpPas encore d'évaluation

- C-5 Dividend Policy 3rdDocument12 pagesC-5 Dividend Policy 3rdsamuel debebePas encore d'évaluation

- Dividend Policy Analysis For Sun PharmaceuticalsDocument16 pagesDividend Policy Analysis For Sun PharmaceuticalsIshita SoodPas encore d'évaluation

- Finance Theory: (Suitable For CFM / FAM & CF Candidates) Corporate FinanceDocument7 pagesFinance Theory: (Suitable For CFM / FAM & CF Candidates) Corporate FinanceLal LalPas encore d'évaluation

- Impact of Dividend Policy On Share PricesDocument16 pagesImpact of Dividend Policy On Share PricesAli JarralPas encore d'évaluation

- Study of Dividend Payout PatternDocument27 pagesStudy of Dividend Payout PatternVivekPas encore d'évaluation

- Finance 1 DineshDocument15 pagesFinance 1 Dineshdinesh-mathew-5072Pas encore d'évaluation

- Impact of Dividend PolicyDocument12 pagesImpact of Dividend PolicyGarimaPas encore d'évaluation

- Project On Impact of Dividends Policy 1Document43 pagesProject On Impact of Dividends Policy 1Soma BanikPas encore d'évaluation

- Decision Areas in Financial ManagementDocument15 pagesDecision Areas in Financial ManagementSana Moid100% (3)

- Determinants of Dividend Payout Ratios: Evidence From United StatesDocument7 pagesDeterminants of Dividend Payout Ratios: Evidence From United StatesSri Wahyuningsih AhmadPas encore d'évaluation

- CHAPTER 1,2 and 3 GodspowerDocument40 pagesCHAPTER 1,2 and 3 GodspowerprincealaseiworimaPas encore d'évaluation

- FM Notes - Unit - 5Document7 pagesFM Notes - Unit - 5Shiva JohriPas encore d'évaluation

- Dividend Policy and Financial Performance of Nigerian Pharmaceutical FirmsDocument17 pagesDividend Policy and Financial Performance of Nigerian Pharmaceutical FirmsRitesh ChatterjeePas encore d'évaluation

- Dividend Policy": Term Paper - I On Corporate Financial ManagementDocument10 pagesDividend Policy": Term Paper - I On Corporate Financial ManagementbodhikolPas encore d'évaluation

- 1926-Article Text-5067-1-10-20231003Document15 pages1926-Article Text-5067-1-10-20231003Rinanti DAPas encore d'évaluation

- Journal 8Document11 pagesJournal 8Kevin LukitoPas encore d'évaluation

- Christ FM Unit 1.4 NotesDocument3 pagesChrist FM Unit 1.4 NotesDrawing MasterPas encore d'évaluation

- Southeastern Steel Company Dividend Policy Financial ManagementDocument24 pagesSoutheastern Steel Company Dividend Policy Financial ManagementJobiCosmePas encore d'évaluation

- 19752ipcc FM Vol1 Cp6Document0 page19752ipcc FM Vol1 Cp6M Waqas PkPas encore d'évaluation

- B-4 Aut 2009Document4 pagesB-4 Aut 2009M Waqas PkPas encore d'évaluation

- Chap 002Document11 pagesChap 002M Waqas PkPas encore d'évaluation

- Pakistan Institute of Public Finance Accountants (PIPFA) : Registration Form (Only For Remote Area Students)Document3 pagesPakistan Institute of Public Finance Accountants (PIPFA) : Registration Form (Only For Remote Area Students)M Waqas PkPas encore d'évaluation

- Total Income, Taxable Income & Tax On Taxable Income (4, 9, 10, 11)Document0 pageTotal Income, Taxable Income & Tax On Taxable Income (4, 9, 10, 11)M Waqas PkPas encore d'évaluation

- MCQSDocument9 pagesMCQSM Waqas PkPas encore d'évaluation

- File Name SjgftamperDocument7 pagesFile Name SjgftamperM Waqas PkPas encore d'évaluation

- Library Services Internal Audit ReportDocument23 pagesLibrary Services Internal Audit Reportbahria libPas encore d'évaluation

- ACTIVITY 1 MabalaDocument5 pagesACTIVITY 1 MabalaJulie mabuyoPas encore d'évaluation

- Income Statement - Kieso 4Document34 pagesIncome Statement - Kieso 4Muhammad RezaPas encore d'évaluation

- 2010 P T D 2552Document9 pages2010 P T D 2552Shehzad HaiderPas encore d'évaluation

- Boat 20000 Mah Power Bank (20 W, Quick Charge 3.0, Power Delivery 2.0)Document1 pageBoat 20000 Mah Power Bank (20 W, Quick Charge 3.0, Power Delivery 2.0)entertainment kingPas encore d'évaluation

- GR 175410Document28 pagesGR 175410Eins BalagtasPas encore d'évaluation

- Income Tax II Illustration IFOS PDFDocument5 pagesIncome Tax II Illustration IFOS PDFSubramanian SenthilPas encore d'évaluation

- City of Fort St. John - Pandemic Effect On The Operating Budget, March 2020Document4 pagesCity of Fort St. John - Pandemic Effect On The Operating Budget, March 2020AlaskaHighwayNewsPas encore d'évaluation

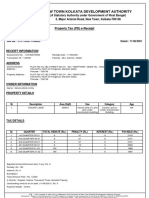

- New Town Kolkata Development Authority: Property Tax (PD) E-ReceiptDocument2 pagesNew Town Kolkata Development Authority: Property Tax (PD) E-ReceiptSSK DEVELOPERSPas encore d'évaluation

- Bengal Tiger Line Pte Ltd. Vs DCIT ITAT ChennaiDocument40 pagesBengal Tiger Line Pte Ltd. Vs DCIT ITAT ChennaiArulnidhi Ramanathan SeshanPas encore d'évaluation

- Financial Ratios Analysis of Mahindra & Mahindra Limited: Financial Accounting MBA (IB) 2015-17Document22 pagesFinancial Ratios Analysis of Mahindra & Mahindra Limited: Financial Accounting MBA (IB) 2015-17Rajat NakraPas encore d'évaluation

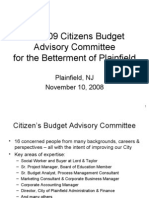

- 2008-09 Citizens Budget Advisory Committee For The Betterment of PlainfieldDocument35 pages2008-09 Citizens Budget Advisory Committee For The Betterment of Plainfielddandamon100% (1)

- RMC No 24-18 - Annexes B1-B5 - Required AttachmentsDocument3 pagesRMC No 24-18 - Annexes B1-B5 - Required AttachmentsGil PinoPas encore d'évaluation

- FICO Module Course ContentsDocument3 pagesFICO Module Course ContentsMohammed Nawaz Shariff100% (1)

- Test Bank For Corporate Finance The Core, 5e Jonathan BerkDocument13 pagesTest Bank For Corporate Finance The Core, 5e Jonathan Berksobiakhan52292Pas encore d'évaluation

- Comm. of Internal Revenue v. CA, G. R. No. 47421, May 14, 1990Document3 pagesComm. of Internal Revenue v. CA, G. R. No. 47421, May 14, 1990Gracëëy UyPas encore d'évaluation

- Thomas 2017Document42 pagesThomas 2017Afifah NurzahrahPas encore d'évaluation

- Sample Personal BudgetDocument5 pagesSample Personal BudgetJames jjPas encore d'évaluation

- Ra 7171Document3 pagesRa 7171John Paul GarciaPas encore d'évaluation

- Heavy Metal and Tube India PVT LTD Unit 1 - 272 - 17-06-2022Document1 pageHeavy Metal and Tube India PVT LTD Unit 1 - 272 - 17-06-2022pragnesh prajapatiPas encore d'évaluation

- Zero Rated TransactionsDocument4 pagesZero Rated Transactionssad nuPas encore d'évaluation

- PTI Textile Policy Presentation (Complete)Document18 pagesPTI Textile Policy Presentation (Complete)Insaf.PK100% (3)