Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Myungsoo YooDocument5 pagesMyungsoo YooITPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- 001 SAP Collection Management Config PreviewDocument31 pages001 SAP Collection Management Config PreviewKarina NunesPas encore d'évaluation

- Effect of Price Change on Substitute GoodsDocument10 pagesEffect of Price Change on Substitute GoodsDrishika Mahajan100% (1)

- Robotic Process Automation: Bachelor of TechnologyDocument9 pagesRobotic Process Automation: Bachelor of TechnologyShivam Juneja0% (1)

- EOC22Document24 pagesEOC22jl123123Pas encore d'évaluation

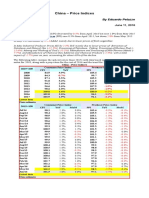

- China - Price IndicesDocument1 pageChina - Price IndicesEduardo PetazzePas encore d'évaluation

- Turkey - Gross Domestic Product, Outlook 2016-2017Document1 pageTurkey - Gross Domestic Product, Outlook 2016-2017Eduardo PetazzePas encore d'évaluation

- Germany - Renewable Energies ActDocument1 pageGermany - Renewable Energies ActEduardo PetazzePas encore d'évaluation

- India - Index of Industrial ProductionDocument1 pageIndia - Index of Industrial ProductionEduardo PetazzePas encore d'évaluation

- Analysis and Estimation of The US Oil ProductionDocument1 pageAnalysis and Estimation of The US Oil ProductionEduardo PetazzePas encore d'évaluation

- U.S. Employment Situation - 2015 / 2017 OutlookDocument1 pageU.S. Employment Situation - 2015 / 2017 OutlookEduardo PetazzePas encore d'évaluation

- China - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaDocument1 pageChina - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaEduardo PetazzePas encore d'évaluation

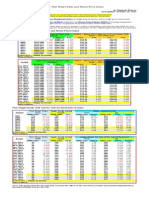

- WTI Spot PriceDocument4 pagesWTI Spot PriceEduardo Petazze100% (1)

- India 2015 GDPDocument1 pageIndia 2015 GDPEduardo PetazzePas encore d'évaluation

- Highlights, Wednesday June 8, 2016Document1 pageHighlights, Wednesday June 8, 2016Eduardo PetazzePas encore d'évaluation

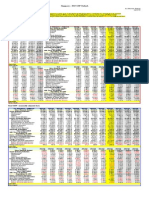

- Commitment of Traders - Futures Only Contracts - NYMEX (American)Document1 pageCommitment of Traders - Futures Only Contracts - NYMEX (American)Eduardo PetazzePas encore d'évaluation

- Reflections On The Greek Crisis and The Level of EmploymentDocument1 pageReflections On The Greek Crisis and The Level of EmploymentEduardo PetazzePas encore d'évaluation

- U.S. New Home Sales and House Price IndexDocument1 pageU.S. New Home Sales and House Price IndexEduardo PetazzePas encore d'évaluation

- México, PBI 2015Document1 pageMéxico, PBI 2015Eduardo PetazzePas encore d'évaluation

- Singapore - 2015 GDP OutlookDocument1 pageSingapore - 2015 GDP OutlookEduardo PetazzePas encore d'évaluation

- U.S. Federal Open Market Committee: Federal Funds RateDocument1 pageU.S. Federal Open Market Committee: Federal Funds RateEduardo PetazzePas encore d'évaluation

- Japan, Population and Labour Force - 2015-2017 OutlookDocument1 pageJapan, Population and Labour Force - 2015-2017 OutlookEduardo PetazzePas encore d'évaluation

- South Africa - 2015 GDP OutlookDocument1 pageSouth Africa - 2015 GDP OutlookEduardo PetazzePas encore d'évaluation

- USA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesDocument1 pageUSA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesEduardo PetazzePas encore d'évaluation

- China - Power GenerationDocument1 pageChina - Power GenerationEduardo PetazzePas encore d'évaluation

- US Mining Production IndexDocument1 pageUS Mining Production IndexEduardo PetazzePas encore d'évaluation

- Brazilian Foreign TradeDocument1 pageBrazilian Foreign TradeEduardo PetazzePas encore d'évaluation

- US - Personal Income and Outlays - 2015-2016 OutlookDocument1 pageUS - Personal Income and Outlays - 2015-2016 OutlookEduardo PetazzePas encore d'évaluation

- Mainland China - Interest Rates and InflationDocument1 pageMainland China - Interest Rates and InflationEduardo PetazzePas encore d'évaluation

- European Commission, Spring 2015 Economic Forecast, Employment SituationDocument1 pageEuropean Commission, Spring 2015 Economic Forecast, Employment SituationEduardo PetazzePas encore d'évaluation

- Highlights in Scribd, Updated in April 2015Document1 pageHighlights in Scribd, Updated in April 2015Eduardo PetazzePas encore d'évaluation

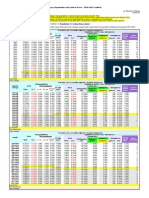

- Chile, Monthly Index of Economic Activity, IMACECDocument2 pagesChile, Monthly Index of Economic Activity, IMACECEduardo PetazzePas encore d'évaluation

- South Korea, Monthly Industrial StatisticsDocument1 pageSouth Korea, Monthly Industrial StatisticsEduardo PetazzePas encore d'évaluation

- United States - Gross Domestic Product by IndustryDocument1 pageUnited States - Gross Domestic Product by IndustryEduardo PetazzePas encore d'évaluation

- Japan, Indices of Industrial ProductionDocument1 pageJapan, Indices of Industrial ProductionEduardo PetazzePas encore d'évaluation

- Kraus 2021 Digital Transformation An OverviewDocument15 pagesKraus 2021 Digital Transformation An OverviewPatrick O MahonyPas encore d'évaluation

- Reports On Audited Financial Statements PDFDocument28 pagesReports On Audited Financial Statements PDFoptimistic070% (1)

- Case Chapter 5Document3 pagesCase Chapter 5Laras Dwi ArofatinPas encore d'évaluation

- Sign In, Audit Incident Problem ManagementDocument4 pagesSign In, Audit Incident Problem ManagementDiaz MahardikaPas encore d'évaluation

- PRICE DISCRIMINATION AND OPPORTUNITY COSTDocument15 pagesPRICE DISCRIMINATION AND OPPORTUNITY COSTjoshua xxxPas encore d'évaluation

- DNB Finance Analytics BrochureDocument9 pagesDNB Finance Analytics Brochurenownutthamon74Pas encore d'évaluation

- Managing Through The Life CycleDocument34 pagesManaging Through The Life CycleAmit ShrivastavaPas encore d'évaluation

- Organised Securities MarketsDocument4 pagesOrganised Securities MarketsNipun Sachdeva50% (2)

- IMC - Module 1Document71 pagesIMC - Module 1jameskuriakose24_521Pas encore d'évaluation

- MSc Financial Markets, Financial Institutions and Banking - Lecture 1 IntroductionDocument26 pagesMSc Financial Markets, Financial Institutions and Banking - Lecture 1 IntroductionLumumba KuyelaPas encore d'évaluation

- Shivani TA ResumeDocument2 pagesShivani TA Resumesabkajob jobPas encore d'évaluation

- 2021 05 EN Ulkomaalaisena Tyontekijana Suomessa PDFDocument20 pages2021 05 EN Ulkomaalaisena Tyontekijana Suomessa PDFSt JakobPas encore d'évaluation

- Dewar, J. International-Project-FinanceDocument559 pagesDewar, J. International-Project-FinanceFederico Silva DuartePas encore d'évaluation

- SampledatafoodsalesDocument10 pagesSampledatafoodsalesMunish RanaPas encore d'évaluation

- Director VP Program Manager in Raleigh NC Resume Mary Paige ForresterDocument6 pagesDirector VP Program Manager in Raleigh NC Resume Mary Paige ForresterMaryPaigeForresterPas encore d'évaluation

- Aspects of StaffingDocument18 pagesAspects of StaffingKASHISH JAINPas encore d'évaluation

- Foreword by DR Emmanuel Esguerra: Philippine Multimodal Transportation and Logistics RoadmapDocument2 pagesForeword by DR Emmanuel Esguerra: Philippine Multimodal Transportation and Logistics RoadmapPortCallsPas encore d'évaluation

- ĐỀ TOEIC READING - TỪ MS HOA TOEICDocument43 pagesĐỀ TOEIC READING - TỪ MS HOA TOEICTrang NguyễnPas encore d'évaluation

- Tesco's Pioneering Online Grocery StrategyDocument34 pagesTesco's Pioneering Online Grocery StrategyPratik Majumder50% (4)

- HRD and Corporate Social ResponsibilityDocument24 pagesHRD and Corporate Social ResponsibilityCamille HofilenaPas encore d'évaluation

- Safety Shoes PolicyDocument1 pageSafety Shoes PolicyMarlon BernardoPas encore d'évaluation

- Make Way For The Algorithms Symbolic Actions and Change in A Regime of KnowingDocument26 pagesMake Way For The Algorithms Symbolic Actions and Change in A Regime of KnowingAbimbola PotterPas encore d'évaluation

- Advance Multiple Choice QuizDocument4 pagesAdvance Multiple Choice QuizSamuel DebebePas encore d'évaluation

- Module 9Document12 pagesModule 9Johanna RullanPas encore d'évaluation

- BondsDocument12 pagesBondsGelyn Cruz100% (1)