Vous aimerez peut-être aussi

- United States Bankruptcy Court Southern District of New YorkDocument108 pagesUnited States Bankruptcy Court Southern District of New YorkdrneshaPas encore d'évaluation

- The Federal Budget Process, 2E: A Description of the Federal and Congressional Budget Processes, Including TimelinesD'EverandThe Federal Budget Process, 2E: A Description of the Federal and Congressional Budget Processes, Including TimelinesPas encore d'évaluation

- CVI - Dunwoody Feasibility StudyDocument25 pagesCVI - Dunwoody Feasibility StudyTucker InitiativePas encore d'évaluation

- PVR 2015.07.02Document1 pagePVR 2015.07.02jordan.e.ferrellPas encore d'évaluation

- 10-21-13 City of Lorain Released From Fiscal WatchDocument1 page10-21-13 City of Lorain Released From Fiscal WatchThe News-HeraldPas encore d'évaluation

- New York State Dept. of Social Servs. v. Dublino, 413 U.S. 405 (1973)Document22 pagesNew York State Dept. of Social Servs. v. Dublino, 413 U.S. 405 (1973)Scribd Government DocsPas encore d'évaluation

- HB 227 Department of Legislative Services: Maryland General Assembly 2018 SessionDocument3 pagesHB 227 Department of Legislative Services: Maryland General Assembly 2018 SessionMunyambu VinyaPas encore d'évaluation

- 2012 End of Session Report - FRADocument3 pages2012 End of Session Report - FRADiana LewisPas encore d'évaluation

- Multistate Comment Letter To DHS Re Public Charge Ground of InadmissibilityDocument24 pagesMultistate Comment Letter To DHS Re Public Charge Ground of InadmissibilityWXMIPas encore d'évaluation

- See Chapter 20 of 48 U.S. CodeDocument4 pagesSee Chapter 20 of 48 U.S. CodeMetro Puerto RicoPas encore d'évaluation

- Missouri, Et Al. v. Biden, Et Al.Document62 pagesMissouri, Et Al. v. Biden, Et Al.Spencer BrownPas encore d'évaluation

- Federal Budget Sequestration 101: Perspectives Through The County LensDocument31 pagesFederal Budget Sequestration 101: Perspectives Through The County LenslaedcpdfsPas encore d'évaluation

- Division of Criminal Justice ServicesDocument19 pagesDivision of Criminal Justice ServicesNick ReismanPas encore d'évaluation

- Legislative Summary - 2014 County CouncilDocument90 pagesLegislative Summary - 2014 County CouncilAlejandro PuyPas encore d'évaluation

- 2010 Taxpayers League of Minnesota ScorecardDocument6 pages2010 Taxpayers League of Minnesota ScorecardThe Taxpayers League of MinnesotaPas encore d'évaluation

- State Minnesota: A Growing Economy That Creates Middle-Class JobsDocument5 pagesState Minnesota: A Growing Economy That Creates Middle-Class Jobsjennifer_brooks3458Pas encore d'évaluation

- Executive BudgetDocument284 pagesExecutive Budgetrmuller4Pas encore d'évaluation

- S A P S A P: Tatement of Dministration Olicy Tatement of Dministration OlicyDocument6 pagesS A P S A P: Tatement of Dministration Olicy Tatement of Dministration OlicylosangelesPas encore d'évaluation

- DeKalb GA SP DowngradeDocument5 pagesDeKalb GA SP DowngradeheneghanPas encore d'évaluation

- 3.23.11 Final - MMB - Letter To Abeler - HannDocument2 pages3.23.11 Final - MMB - Letter To Abeler - Hanntom_scheckPas encore d'évaluation

- News 2012-6-26 PendencyPlanApprovedDocument3 pagesNews 2012-6-26 PendencyPlanApprovedDvNetPas encore d'évaluation

- DISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT - Case No. 5D22-2277Document42 pagesDISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT - Case No. 5D22-2277Brandon Hogan0% (1)

- City of Oneida Department SalariesDocument1 pageCity of Oneida Department SalariesOneida Daily DispatchPas encore d'évaluation

- Senate Passes Extenders Bill: © 2006-2010, CPC Holdings, LLC Privacy Policy - Terms of Use & DisclaimerDocument1 pageSenate Passes Extenders Bill: © 2006-2010, CPC Holdings, LLC Privacy Policy - Terms of Use & Disclaimerruss willisPas encore d'évaluation

- Letter To Court - 10242012 HearingDocument3 pagesLetter To Court - 10242012 Hearinggary6842Pas encore d'évaluation

- Senate Hearing, 108TH Congress - An Overview of The Radiation Exposure Compensation ProgramDocument88 pagesSenate Hearing, 108TH Congress - An Overview of The Radiation Exposure Compensation ProgramScribd Government DocsPas encore d'évaluation

- Knapik Press Release - Knapik Secures Funding in Supplemental Budget For Southwick War MemorialDocument3 pagesKnapik Press Release - Knapik Secures Funding in Supplemental Budget For Southwick War MemorialMike KnapikPas encore d'évaluation

- What Is The HoldupDocument3 pagesWhat Is The HoldupGovernor Chris ChristiePas encore d'évaluation

- 2008 Spring Audit State Developments 2Document285 pages2008 Spring Audit State Developments 2rashidsfPas encore d'évaluation

- FY 13-14 Fiscal HighlightsDocument144 pagesFY 13-14 Fiscal HighlightsRepNLandryPas encore d'évaluation

- Housing OptionsDocument17 pagesHousing OptionsScott FranzPas encore d'évaluation

- McKee ARPA Down PaymentDocument12 pagesMcKee ARPA Down PaymentNBC 10 WJARPas encore d'évaluation

- Factsheet About Misuse of Colorado Public Funds in The Sudan For Investigators and MediaDocument11 pagesFactsheet About Misuse of Colorado Public Funds in The Sudan For Investigators and Mediama91c1anPas encore d'évaluation

- HLWD July 24 MinutesDocument3 pagesHLWD July 24 MinutesLivewire Printing CompanyPas encore d'évaluation

- United States Court of Appeals, Second Circuit.: No. 422. Docket 35519Document8 pagesUnited States Court of Appeals, Second Circuit.: No. 422. Docket 35519Scribd Government DocsPas encore d'évaluation

- Office of The City AdministratorDocument6 pagesOffice of The City AdministratorSusie CambriaPas encore d'évaluation

- LegislativeUpdate3 22 13Document1 pageLegislativeUpdate3 22 13Dave ThompsonPas encore d'évaluation

- NJ Senate Dems - 2013 State of Our State, 1-7-13Document13 pagesNJ Senate Dems - 2013 State of Our State, 1-7-13Democratic Governors AssociationPas encore d'évaluation

- Countl: Unit D S AT SO AmericaDocument16 pagesCountl: Unit D S AT SO AmericaTyler EstepPas encore d'évaluation

- IDC Campaign Finance Reform Press ReleaseDocument3 pagesIDC Campaign Finance Reform Press ReleaseNick ReismanPas encore d'évaluation

- 01956-011007 GreggDocument1 page01956-011007 GregglosangelesPas encore d'évaluation

- San Diego Pension Fraud: California Supreme Court Dismisses Criminal Charges Against San Diego City Retirement BoardDocument65 pagesSan Diego Pension Fraud: California Supreme Court Dismisses Criminal Charges Against San Diego City Retirement BoardPublicPas encore d'évaluation

- IDC Campaign Finance Reform Press ReleaseDocument3 pagesIDC Campaign Finance Reform Press ReleaseJon CampbellPas encore d'évaluation

- Counties United in Opposition To NYS Budget Proposal That Would Take $625 Million From Local TaxpayersDocument2 pagesCounties United in Opposition To NYS Budget Proposal That Would Take $625 Million From Local TaxpayersNewzjunkyPas encore d'évaluation

- IDC Recommendations 1-10-2011Document3 pagesIDC Recommendations 1-10-2011Celeste KatzPas encore d'évaluation

- Memorandum of Law: County Line Materials Recovery Facility, Town of Cayuta, County of Schuyler, State of New YorkDocument10 pagesMemorandum of Law: County Line Materials Recovery Facility, Town of Cayuta, County of Schuyler, State of New YorkSteven GetmanPas encore d'évaluation

- The Streamline Search: Options For NY Localities: Empire IdeaDocument8 pagesThe Streamline Search: Options For NY Localities: Empire IdeajspectorPas encore d'évaluation

- United States Court of Appeals, Second Circuit.: Argued March 7, 2006. Decided September 21, 2006Document16 pagesUnited States Court of Appeals, Second Circuit.: Argued March 7, 2006. Decided September 21, 2006Scribd Government DocsPas encore d'évaluation

- ST - Louis County ADA Transition Plan DRAFTDocument111 pagesST - Louis County ADA Transition Plan DRAFTBarrett ChasePas encore d'évaluation

- Village Council Letter To LGCDocument4 pagesVillage Council Letter To LGCJohanna Ferebee StillPas encore d'évaluation

- Housing Opportunity Task Force ReportDocument99 pagesHousing Opportunity Task Force Reportmariner12Pas encore d'évaluation

- LegislativeUpdate4 22-29 13Document1 pageLegislativeUpdate4 22-29 13Dave ThompsonPas encore d'évaluation

- Riverview District & Riverview Education Association Recommendations FinalDocument10 pagesRiverview District & Riverview Education Association Recommendations FinalBucsintheKnowPas encore d'évaluation

- 2011 Legislative E-Report #7Document4 pages2011 Legislative E-Report #7LawrenceLeaguePas encore d'évaluation

- Gil Aguirre's Complaint Sent To DA's Office Regarding Nick ConwayDocument13 pagesGil Aguirre's Complaint Sent To DA's Office Regarding Nick ConwaySGVNewsPas encore d'évaluation

- Real Estate Services Update: January 2011Document4 pagesReal Estate Services Update: January 2011narwebteamPas encore d'évaluation

- Senate Hearing, 110TH Congress - Financial Services and General Government Appropriations For Fiscal Year 2008Document51 pagesSenate Hearing, 110TH Congress - Financial Services and General Government Appropriations For Fiscal Year 2008Scribd Government DocsPas encore d'évaluation

- Kentucky League of Cities: City Officials Legal HandbookD'EverandKentucky League of Cities: City Officials Legal HandbookPas encore d'évaluation

- Shoomi House ResolutionDocument2 pagesShoomi House ResolutionTucker InitiativePas encore d'évaluation

- Organizational ActDocument28 pagesOrganizational ActTucker InitiativePas encore d'évaluation

- Clarkston Petition To Contest Referendum VoteDocument18 pagesClarkston Petition To Contest Referendum VoteTucker InitiativePas encore d'évaluation

- Task Force Comments - LorenzDocument3 pagesTask Force Comments - LorenzTucker InitiativePas encore d'évaluation

- Final Version of House Bill 1128 For Annexations To The City of ClarkstonDocument4 pagesFinal Version of House Bill 1128 For Annexations To The City of ClarkstonTucker InitiativePas encore d'évaluation

- Organizational Act Municode 9-2014Document27 pagesOrganizational Act Municode 9-2014Tucker InitiativePas encore d'évaluation

- Tucker Districts 3-1-14 v1.0Document1 pageTucker Districts 3-1-14 v1.0Tucker InitiativePas encore d'évaluation

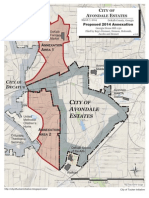

- Clarkston Annexation 2014 v1.0Document1 pageClarkston Annexation 2014 v1.0Tucker InitiativePas encore d'évaluation

- Doraville Annexation Bill HB 1139Document8 pagesDoraville Annexation Bill HB 1139Tucker InitiativePas encore d'évaluation

- AE Annexation 2014 v1.0Document1 pageAE Annexation 2014 v1.0Tucker InitiativePas encore d'évaluation

- Section 1.: TH TH STDocument3 pagesSection 1.: TH TH STTucker InitiativePas encore d'évaluation

- Briarcliff Report - Final5Document54 pagesBriarcliff Report - Final5Tucker InitiativePas encore d'évaluation

- Doraville Annexation Bill HB 1138Document7 pagesDoraville Annexation Bill HB 1138Tucker InitiativePas encore d'évaluation

- 142757Document3 pages142757Tucker InitiativePas encore d'évaluation

- Stone Mountain Annexation Feasibility Study, January 17, 2014Document36 pagesStone Mountain Annexation Feasibility Study, January 17, 2014Tucker InitiativePas encore d'évaluation

- Decatur Memo Annexation 2012Document7 pagesDecatur Memo Annexation 2012Tucker InitiativePas encore d'évaluation

- Briarcliff Districts 2-27-14 v1.0Document1 pageBriarcliff Districts 2-27-14 v1.0Tucker InitiativePas encore d'évaluation

- A Proposed City of Stonecrest, Georgia A Fiscal Feasibility Analysis December, 2013Document59 pagesA Proposed City of Stonecrest, Georgia A Fiscal Feasibility Analysis December, 2013Tucker Initiative100% (1)

- Proposed City of Lakeside, Version 4.Document1 pageProposed City of Lakeside, Version 4.Tucker InitiativePas encore d'évaluation

- Council Annexation Presentations 090313Document39 pagesCouncil Annexation Presentations 090313Tucker InitiativePas encore d'évaluation

- City of Lakeside Final CVI Study 11 - 2013Document59 pagesCity of Lakeside Final CVI Study 11 - 2013The Brookhaven PostPas encore d'évaluation

- City of Tucker Feasibility StudyDocument35 pagesCity of Tucker Feasibility StudyTucker InitiativePas encore d'évaluation

- Clarkston Annexation PlansDocument1 pageClarkston Annexation PlansTucker InitiativePas encore d'évaluation

- Decatur Memo AnnexationDocument7 pagesDecatur Memo AnnexationTucker InitiativePas encore d'évaluation

- The Proposed City of StonecrestDocument1 pageThe Proposed City of StonecrestTucker InitiativePas encore d'évaluation

- The Proposed City of Tucker - Population by RaceDocument1 pageThe Proposed City of Tucker - Population by RaceTucker InitiativePas encore d'évaluation

- DeKalb County - Population by RaceDocument1 pageDeKalb County - Population by RaceTucker InitiativePas encore d'évaluation

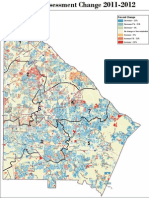

- Residential Property Assessment Change 2011 2012Document1 pageResidential Property Assessment Change 2011 2012Tucker InitiativePas encore d'évaluation

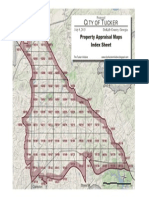

- Tucker Property Appraisal Map 1.0 SDocument1 pageTucker Property Appraisal Map 1.0 STucker InitiativePas encore d'évaluation

- Homestead AppDocument3 pagesHomestead AppCee SPas encore d'évaluation

- Facts About The Homestead ActsDocument8 pagesFacts About The Homestead ActsAnonymous nYwWYS3ntV100% (1)

- Texas Property Tax Law Changes: As of December 2021Document44 pagesTexas Property Tax Law Changes: As of December 2021jbc77Pas encore d'évaluation

- The Fiscal Impact On DeKalb County With Possible Incorporation of Dunwoody, GeorgiaDocument20 pagesThe Fiscal Impact On DeKalb County With Possible Incorporation of Dunwoody, GeorgiaTucker InitiativePas encore d'évaluation

- Residence Homestead Exemption ApplicationDocument3 pagesResidence Homestead Exemption ApplicationRJ MarquezPas encore d'évaluation

- Propertytax BasicsDocument29 pagesPropertytax BasicsO'Connor AssociatePas encore d'évaluation

- Residence Homestead Exemption Application: Form 50-114Document3 pagesResidence Homestead Exemption Application: Form 50-114lucaPas encore d'évaluation

- Estate Plannning&Asset Protection in FL - CompleteDocument900 pagesEstate Plannning&Asset Protection in FL - Completeartsan3Pas encore d'évaluation

- A Reprint From Tierra Grande Magazine © 2014. Real Estate Center. All Rights ReservedDocument5 pagesA Reprint From Tierra Grande Magazine © 2014. Real Estate Center. All Rights Reservedapi-251198534Pas encore d'évaluation

- BCAD Homestead Exemption FormDocument1 pageBCAD Homestead Exemption Formjboggs100% (1)

- HomesteadTaxCreditAndExemption (54028)Document2 pagesHomesteadTaxCreditAndExemption (54028)Gazetteonline100% (4)

- Texas Property Tax Exemptions 96-1740Document24 pagesTexas Property Tax Exemptions 96-1740jimmyboy111Pas encore d'évaluation

- Texas Property Tax ExemptionsDocument22 pagesTexas Property Tax Exemptionshuy luongPas encore d'évaluation

- 2015 Progress Texas Constitutional Amendment Ballot GuideDocument4 pages2015 Progress Texas Constitutional Amendment Ballot GuideProgressTX100% (1)

- 2023 Notice of Appraised Value: Collin Central Appraisal District 250 Eldorado Pkwy MCKINNEY, TX 75069-8023Document1 page2023 Notice of Appraised Value: Collin Central Appraisal District 250 Eldorado Pkwy MCKINNEY, TX 75069-8023Fuzzy PandaPas encore d'évaluation

- Are Your Property Taxes Too HighDocument8 pagesAre Your Property Taxes Too HighcutmytaxesPas encore d'évaluation

- Maine Municipal Issues Paper 2018Document24 pagesMaine Municipal Issues Paper 2018Lauren PorterPas encore d'évaluation

- 50-114 Residence Homestead Exemption Application PDFDocument3 pages50-114 Residence Homestead Exemption Application PDFAnonymous Pb39klJPas encore d'évaluation

- Carollo Emergency MotionDocument58 pagesCarollo Emergency MotionChris GothnerPas encore d'évaluation

- Texas Property Tax ExemptionsDocument23 pagesTexas Property Tax ExemptionsBruce WaynePas encore d'évaluation

- Dekalb Sample Ballot 2016 Gen ElectionDocument4 pagesDekalb Sample Ballot 2016 Gen ElectionAtlanta Jobs with JusticePas encore d'évaluation

- Property Tax ExemptionsDocument1 pageProperty Tax ExemptionsLexi CortesPas encore d'évaluation

- Budget BriefingDocument72 pagesBudget BriefingApril ToweryPas encore d'évaluation