Vous aimerez peut-être aussi

- Credit Risk Management In and Out of the Financial Crisis: New Approaches to Value at Risk and Other ParadigmsD'EverandCredit Risk Management In and Out of the Financial Crisis: New Approaches to Value at Risk and Other ParadigmsÉvaluation : 1 sur 5 étoiles1/5 (1)

- 039482-OCR Parte1Document41 pages039482-OCR Parte1Pepe LopezPas encore d'évaluation

- U. S. Loan Syndications: Chris Droussiotis Spring 2010Document37 pagesU. S. Loan Syndications: Chris Droussiotis Spring 2010Ash_ish_vPas encore d'évaluation

- Bcreg 20230224 A 1Document13 pagesBcreg 20230224 A 1Sirak AynalemPas encore d'évaluation

- Credit RatingDocument40 pagesCredit RatingBishnu DhamalaPas encore d'évaluation

- Credit Rating System of BangladeshDocument19 pagesCredit Rating System of BangladeshshababPas encore d'évaluation

- Have Credit Rating Agencies Got A Role in Triggering 2007 Global Financial Crisis?Document5 pagesHave Credit Rating Agencies Got A Role in Triggering 2007 Global Financial Crisis?Emanuela Alexandra SavinPas encore d'évaluation

- CAMELS LiveOakBancsharesIncDocument20 pagesCAMELS LiveOakBancsharesIncSean BursonPas encore d'évaluation

- Lecture 7 Credit Risk Basel AccordsDocument44 pagesLecture 7 Credit Risk Basel AccordsAjid Ur RehmanPas encore d'évaluation

- Disclosure Requirements For BanksDocument19 pagesDisclosure Requirements For Banksmunna tamangPas encore d'évaluation

- Types of Risks in Banking Sector: DR - SMDocument30 pagesTypes of Risks in Banking Sector: DR - SMPriya DharshiniPas encore d'évaluation

- Nomura Home Equity ABS BasicsDocument24 pagesNomura Home Equity ABS Basicsxckvhbxclu12Pas encore d'évaluation

- Work 635Document58 pagesWork 635TBP_Think_TankPas encore d'évaluation

- The Non-Performing Loans: Some Bank-Level EvidencesDocument34 pagesThe Non-Performing Loans: Some Bank-Level EvidencesJORKOS1Pas encore d'évaluation

- Credit Rating BangladeshDocument41 pagesCredit Rating BangladeshSumedh PujariPas encore d'évaluation

- Chapter Sixteen Sovereign Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SixteenDocument12 pagesChapter Sixteen Sovereign Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SixteenRonak ChoudharyPas encore d'évaluation

- 2004 Report - Liq. RiskDocument12 pages2004 Report - Liq. RiskMina ZarifPas encore d'évaluation

- The Non-Performing LoansDocument34 pagesThe Non-Performing Loanshannory100% (1)

- FRB Summary Analysis of Failed Bank Reviews - Sep 2011Document60 pagesFRB Summary Analysis of Failed Bank Reviews - Sep 2011wateramericanPas encore d'évaluation

- Senate Hearing, 108TH Congress - Departments of Veterans Affairs and Housing and Urban Development, and Independent Agencies Appropriations For Fiscal Year 2004Document180 pagesSenate Hearing, 108TH Congress - Departments of Veterans Affairs and Housing and Urban Development, and Independent Agencies Appropriations For Fiscal Year 2004Scribd Government DocsPas encore d'évaluation

- Objective: Reference Books Author / Publication Credit Management IcfaiDocument8 pagesObjective: Reference Books Author / Publication Credit Management IcfaithukkerPas encore d'évaluation

- Amarak Hos HaDocument12 pagesAmarak Hos Haaarpee78Pas encore d'évaluation

- Session-2 Introduction To Credit RiskDocument40 pagesSession-2 Introduction To Credit RiskSagar KansalPas encore d'évaluation

- Classification N ProvisionDocument37 pagesClassification N ProvisionNur AlahiPas encore d'évaluation

- Tier 1 Capital RatioDocument23 pagesTier 1 Capital RatiokapilchandanPas encore d'évaluation

- Credit Documentation StandardsDocument12 pagesCredit Documentation StandardsAurangzeb MajeedPas encore d'évaluation

- Credit RatingDocument31 pagesCredit RatingAkshat JainPas encore d'évaluation

- A Case Study On Loan Loss Analysis of A CommunityDocument53 pagesA Case Study On Loan Loss Analysis of A CommunityPriya SivakumarPas encore d'évaluation

- Supervision and Regulation Report (FED Document)Document40 pagesSupervision and Regulation Report (FED Document)Crack RapPas encore d'évaluation

- Managing Credit Risk: Features of Internal RatingDocument5 pagesManaging Credit Risk: Features of Internal RatingMansi VanshPas encore d'évaluation

- What Role Did Credit Rating Agencies Play in The Credit Crisis?Document23 pagesWhat Role Did Credit Rating Agencies Play in The Credit Crisis?Omprakash SangalePas encore d'évaluation

- Padma PolyCotton Knit Fabrics Limited - 2011Document5 pagesPadma PolyCotton Knit Fabrics Limited - 2011fahim_bdPas encore d'évaluation

- Company Law ProjectDocument7 pagesCompany Law Projectanon_365581619Pas encore d'évaluation

- Group 2 Case Basel IIDocument6 pagesGroup 2 Case Basel IInisargpatel19Pas encore d'évaluation

- Pratik Tiwari Finance ProjectDocument75 pagesPratik Tiwari Finance ProjectPratik TiwariPas encore d'évaluation

- BAC Stress Testing Results - FinalDocument18 pagesBAC Stress Testing Results - FinalOSRPas encore d'évaluation

- Camel 1Document7 pagesCamel 1Papa PappaPas encore d'évaluation

- What Drives Loss Given Default? Evidence From Commercial Real Estate Loans at Failed BanksDocument35 pagesWhat Drives Loss Given Default? Evidence From Commercial Real Estate Loans at Failed BanksSushantPas encore d'évaluation

- Presented By: Rajesh Sandhya Santhosh Abhishek DamyantiDocument11 pagesPresented By: Rajesh Sandhya Santhosh Abhishek DamyantiDamyanti ShawPas encore d'évaluation

- Ben S Bernanke The Supervisory Capital Assessment Program - One Year LaterDocument6 pagesBen S Bernanke The Supervisory Capital Assessment Program - One Year LaterrunawayyyPas encore d'évaluation

- Will Credit Rating Agency Reforms Be Effective?: JFRC 20,4Document11 pagesWill Credit Rating Agency Reforms Be Effective?: JFRC 20,4Emanuela Alexandra SavinPas encore d'évaluation

- CAMELS Analysis OF CITI BankDocument31 pagesCAMELS Analysis OF CITI BankISHITA GROVER100% (2)

- Auto Loan ABSDocument26 pagesAuto Loan ABSAnonymous 0zdN4FPas encore d'évaluation

- CH-2 - NPAs, Its Emergence and EffectsDocument7 pagesCH-2 - NPAs, Its Emergence and EffectsNirjhar DuttaPas encore d'évaluation

- Pratik Tiwari Project1Document75 pagesPratik Tiwari Project1Pratik TiwariPas encore d'évaluation

- (JPMorgan) Credit Derivatives - A Primer (2005 Edition) PDFDocument36 pages(JPMorgan) Credit Derivatives - A Primer (2005 Edition) PDFsoumensahilPas encore d'évaluation

- G5 Monitoring and Identifying Risks and Intervention ToolsDocument70 pagesG5 Monitoring and Identifying Risks and Intervention ToolsJastinPas encore d'évaluation

- Ection 1: DBRS Fundamentals of Corporate Credit AnalysisDocument23 pagesEction 1: DBRS Fundamentals of Corporate Credit AnalysisPavel LahaPas encore d'évaluation

- Rating Methodology For Housing Finance Companies (HFCS) : Credit Analysis & Research LimitedDocument5 pagesRating Methodology For Housing Finance Companies (HFCS) : Credit Analysis & Research Limiteddeptlab1Pas encore d'évaluation

- Research Paper On Country Risk Analysis: by Ajinkya Yadav MBA - Executive Finance PRN - 19020348002Document18 pagesResearch Paper On Country Risk Analysis: by Ajinkya Yadav MBA - Executive Finance PRN - 19020348002Ajinkya YadavPas encore d'évaluation

- Credit Risk LectureDocument22 pagesCredit Risk LecturejknibmPas encore d'évaluation

- Sloos 202304 FullreportDocument79 pagesSloos 202304 FullreportS CPas encore d'évaluation

- Credit Appraisal IBDocument48 pagesCredit Appraisal IBHenok mekuriaPas encore d'évaluation

- 10.pak Qfipme Topic1 Hfis 13 Leveraged LoansDocument4 pages10.pak Qfipme Topic1 Hfis 13 Leveraged LoansNoodles FSAPas encore d'évaluation

- Npa 119610079679343 5Document46 pagesNpa 119610079679343 5Teju AshuPas encore d'évaluation

- FinQuiz - Smart Summary - Study Session 16 - Reading 56Document7 pagesFinQuiz - Smart Summary - Study Session 16 - Reading 56Rafael100% (1)

- Ing Vysya 2009Document15 pagesIng Vysya 2009Lavanya VitPas encore d'évaluation

- NPL Accounting BOEDocument80 pagesNPL Accounting BOETom, Dick and HarryPas encore d'évaluation

- FRM Part 1 R7Document2 pagesFRM Part 1 R7Tony NasrPas encore d'évaluation

- Advance Monthly Sales For Retail and Food Services September 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services September 2010qtipxPas encore d'évaluation

- Euro Area and EU27 GDP Up by 1.0%Document6 pagesEuro Area and EU27 GDP Up by 1.0%qtipxPas encore d'évaluation

- Speech 456Document11 pagesSpeech 456qtipxPas encore d'évaluation

- Euro Area Annual Inflation Up To 1.9%Document4 pagesEuro Area Annual Inflation Up To 1.9%qtipxPas encore d'évaluation

- Mtis CurrentDocument3 pagesMtis CurrentqtipxPas encore d'évaluation

- PR201007Document1 pagePR201007qtipxPas encore d'évaluation

- Money and Asset Prices: Indicators of Market UncertaintyDocument9 pagesMoney and Asset Prices: Indicators of Market UncertaintyqtipxPas encore d'évaluation

- Advance Monthly Sales For Retail and Food Services APRIL 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services APRIL 2010qtipxPas encore d'évaluation

- Tots ADocument2 pagesTots AqtipxPas encore d'évaluation

- Final Cat Inc ReleaseDocument34 pagesFinal Cat Inc ReleaseqtipxPas encore d'évaluation

- NewresconstDocument6 pagesNewresconstqtipxPas encore d'évaluation

- CHN Jun 10 RevDocument3 pagesCHN Jun 10 RevqtipxPas encore d'évaluation

- Advance Monthly Sales For Retail and Food Services JUNE 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services JUNE 2010qtipxPas encore d'évaluation

- Obama Administration Introduces Monthly Housing ScorecardDocument11 pagesObama Administration Introduces Monthly Housing ScorecardqtipxPas encore d'évaluation

- U.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau NewsDocument4 pagesU.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau NewsqtipxPas encore d'évaluation

- Cpi MayDocument19 pagesCpi MayqtipxPas encore d'évaluation

- International Monetary Fund: How Did Emerging Markets Cope in The Crisis?Document47 pagesInternational Monetary Fund: How Did Emerging Markets Cope in The Crisis?qtipxPas encore d'évaluation

- Q1 ProdDocument15 pagesQ1 ProdqtipxPas encore d'évaluation

- PPI March 2010Document22 pagesPPI March 2010qtipxPas encore d'évaluation

- gdp1q10 2ndDocument15 pagesgdp1q10 2ndqtipxPas encore d'évaluation

- Cpimar 10Document19 pagesCpimar 10qtipxPas encore d'évaluation

- CMA Global Sovereign Credit Risk Report Q1 2010Document17 pagesCMA Global Sovereign Credit Risk Report Q1 2010qtipxPas encore d'évaluation

- The Coca-Cola Company Reports 2010 First Quarter Financial ResultsDocument15 pagesThe Coca-Cola Company Reports 2010 First Quarter Financial ResultsqtipxPas encore d'évaluation

- Small Businesses Add 66,000 New Jobs in AprilDocument5 pagesSmall Businesses Add 66,000 New Jobs in AprilqtipxPas encore d'évaluation

- 2010 First Quarter Business Review: (Unaudited)Document19 pages2010 First Quarter Business Review: (Unaudited)qtipxPas encore d'évaluation

- Eap April2010 ChinaDocument3 pagesEap April2010 ChinaqtipxPas encore d'évaluation

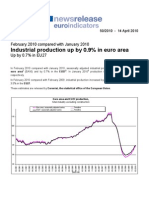

- Industrial Production Up by 0.9% in Euro AreaDocument6 pagesIndustrial Production Up by 0.9% in Euro AreaqtipxPas encore d'évaluation

- Advance Monthly Sales For Retail and Food Services MARCH 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services MARCH 2010qtipxPas encore d'évaluation

- Joint Release U.S. Department of Housing and Urban DevelopmentDocument6 pagesJoint Release U.S. Department of Housing and Urban DevelopmentqtipxPas encore d'évaluation

- Euro Area GDP Stable and EU27 GDP Up by 0.1%Document10 pagesEuro Area GDP Stable and EU27 GDP Up by 0.1%qtipxPas encore d'évaluation

- 11 Acc CH 1 Introduction To Accounting 23-24Document15 pages11 Acc CH 1 Introduction To Accounting 23-24Nathan DavidPas encore d'évaluation

- DCF Valuation - Aswath DamodaranDocument60 pagesDCF Valuation - Aswath DamodaranUtkarshPas encore d'évaluation

- Self Certified Banks (SCSBS) Under The ASBADocument120 pagesSelf Certified Banks (SCSBS) Under The ASBAsubhas10Pas encore d'évaluation

- Benificiary/Remittance Details CPQ3946000 CEN 01 2019 NTPC 12106562277Document1 pageBenificiary/Remittance Details CPQ3946000 CEN 01 2019 NTPC 12106562277manphool singhPas encore d'évaluation

- Visa Prepaid - Myanma Apex BankDocument2 pagesVisa Prepaid - Myanma Apex BankMyo NaingPas encore d'évaluation

- CH 4 - Fixed Income SecurityDocument49 pagesCH 4 - Fixed Income SecurityALEMU TADESSEPas encore d'évaluation

- Retail Banking in IndiaDocument3 pagesRetail Banking in Indiabeena antuPas encore d'évaluation

- Functions of Central BankDocument22 pagesFunctions of Central BankMd Rabbi KhanPas encore d'évaluation

- Chapters 2 and 3 HandoutsDocument8 pagesChapters 2 and 3 HandoutsCarter LeePas encore d'évaluation

- MCQ in Principles of InsuranceDocument27 pagesMCQ in Principles of InsuranceDrJay Trivedi71% (17)

- CRM Including CalculatorDocument110 pagesCRM Including CalculatorChristophe BernardPas encore d'évaluation

- 7 Steps To Understanding The Stock Market Ebook v6Document32 pages7 Steps To Understanding The Stock Market Ebook v6Afsal Mohamed Kani 004Pas encore d'évaluation

- Assignment On Sarbanes Oaxley Act 2Document4 pagesAssignment On Sarbanes Oaxley Act 2Haris MunirPas encore d'évaluation

- Your Vodafone Bill: Amount DueDocument1 pageYour Vodafone Bill: Amount DueBeyza GemiciPas encore d'évaluation

- Suraj Pal SharmaDocument3 pagesSuraj Pal SharmaShiva Vikas KumarPas encore d'évaluation

- In ProgressDocument12 pagesIn ProgressQamarulArifinPas encore d'évaluation

- Audited Consolidated Financial StatementDocument42 pagesAudited Consolidated Financial StatementAbigail EjiroPas encore d'évaluation

- 2-The Origin & Growth of BankingDocument25 pages2-The Origin & Growth of Bankingraghav4231Pas encore d'évaluation

- Annual Report 2018Document467 pagesAnnual Report 2018Tasneef ChowdhuryPas encore d'évaluation

- JpmcstatementDocument6 pagesJpmcstatementxcygonPas encore d'évaluation

- Lehman HYDocument220 pagesLehman HYZerohedge100% (1)

- A Comprehensive Study On Financial Planning and ForecastingDocument66 pagesA Comprehensive Study On Financial Planning and ForecastingInternational Journal of Innovative Science and Research TechnologyPas encore d'évaluation

- Resume of Deliagonzalez34 - 1Document2 pagesResume of Deliagonzalez34 - 1api-24443855Pas encore d'évaluation

- Account Statement PDFDocument12 pagesAccount Statement PDFYuvraj Gogoi100% (1)

- Company To Trust Term SheetDocument2 pagesCompany To Trust Term SheetBobby BabPas encore d'évaluation

- Balance StatementDocument5 pagesBalance Statementmichael anthonyPas encore d'évaluation

- E-Banking Consumer BehaviourDocument116 pagesE-Banking Consumer Behaviourahmadksath88% (24)

- John Geissinger ResumeDocument2 pagesJohn Geissinger Resumekurtis_workmanPas encore d'évaluation

- Agif New PolicyDocument6 pagesAgif New PolicyRamkrishna TalwadkerPas encore d'évaluation

- View Invoice - ReceiptDocument1 pageView Invoice - Receiptspeak2ebiniPas encore d'évaluation

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsD'EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsPas encore d'évaluation

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.D'EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Évaluation : 5 sur 5 étoiles5/5 (91)

- CAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitD'EverandCAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitÉvaluation : 4 sur 5 étoiles4/5 (6)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassD'EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassPas encore d'évaluation

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessD'EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessÉvaluation : 4.5 sur 5 étoiles4.5/5 (4)

- How To Budget And Manage Your Money In 7 Simple StepsD'EverandHow To Budget And Manage Your Money In 7 Simple StepsÉvaluation : 5 sur 5 étoiles5/5 (4)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantD'EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantÉvaluation : 4 sur 5 étoiles4/5 (104)

- The Best Team Wins: The New Science of High PerformanceD'EverandThe Best Team Wins: The New Science of High PerformanceÉvaluation : 4.5 sur 5 étoiles4.5/5 (31)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsD'EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsÉvaluation : 4 sur 5 étoiles4/5 (4)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsD'EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsPas encore d'évaluation

- The 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)D'EverandThe 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)Évaluation : 3.5 sur 5 étoiles3.5/5 (9)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationD'EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationÉvaluation : 4.5 sur 5 étoiles4.5/5 (18)

- Budgeting: The Ultimate Guide for Getting Your Finances TogetherD'EverandBudgeting: The Ultimate Guide for Getting Your Finances TogetherÉvaluation : 5 sur 5 étoiles5/5 (14)

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonD'EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonÉvaluation : 5 sur 5 étoiles5/5 (9)

- The Money Mentor: How to Pay Off Your Mortgage in as Little as 7 Years Without Becoming a HermitD'EverandThe Money Mentor: How to Pay Off Your Mortgage in as Little as 7 Years Without Becoming a HermitPas encore d'évaluation

- Rich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouD'EverandRich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouÉvaluation : 4 sur 5 étoiles4/5 (2)

- Passive Income Ideas: A Comprehensive Guide to Building Multiple Streams of Income Through Digital World and Offline Businesses to Gain the Financial FreedomD'EverandPassive Income Ideas: A Comprehensive Guide to Building Multiple Streams of Income Through Digital World and Offline Businesses to Gain the Financial FreedomÉvaluation : 5 sur 5 étoiles5/5 (1)

- Debt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverD'EverandDebt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverÉvaluation : 3 sur 5 étoiles3/5 (2)

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyD'EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyÉvaluation : 5 sur 5 étoiles5/5 (1)

- You Need a Budget: The Ultimate Guide to Budgeting and Financial Planning for Everyday People, Discover Proven Methods on How to Plan Your Finances to Achieve Your Financial GoalsD'EverandYou Need a Budget: The Ultimate Guide to Budgeting and Financial Planning for Everyday People, Discover Proven Methods on How to Plan Your Finances to Achieve Your Financial GoalsÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- Radically Simple Accounting: A Way Out of the Dark and Into the ProfitD'EverandRadically Simple Accounting: A Way Out of the Dark and Into the ProfitÉvaluation : 4.5 sur 5 étoiles4.5/5 (9)

- The Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomD'EverandThe Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)