Vous aimerez peut-être aussi

- Form ITR-1-2009-10Document7 pagesForm ITR-1-2009-10vikram_enercon3941Pas encore d'évaluation

- Form%20ITR-1Document2 pagesForm%20ITR-1vinay.bpPas encore d'évaluation

- (DD/MM/YYYY) : (Please See Rule 12 of The Income-Tax Rules, 1962) (Also See Attached Instructions)Document5 pages(DD/MM/YYYY) : (Please See Rule 12 of The Income-Tax Rules, 1962) (Also See Attached Instructions)anon-928287100% (1)

- NotificationDocument7 pagesNotificationapi-25886395Pas encore d'évaluation

- Itr 1Document2 pagesItr 1zakirhusssainPas encore d'évaluation

- 12 Itr1 10 11Document6 pages12 Itr1 10 11ramanwwePas encore d'évaluation

- Salma Bano: Indian Income Tax ReturnDocument3 pagesSalma Bano: Indian Income Tax Return9956272017Pas encore d'évaluation

- (DD/MM/YYYY) : (Please See Rule 12 of The Income-Tax Rules, 1962) (Also See Attached Instructions)Document3 pages(DD/MM/YYYY) : (Please See Rule 12 of The Income-Tax Rules, 1962) (Also See Attached Instructions)nilihitaPas encore d'évaluation

- ITR-2 Indian Income Tax Return: Part A-GENDocument6 pagesITR-2 Indian Income Tax Return: Part A-GENsatyaagsPas encore d'évaluation

- Form ITR-3Document7 pagesForm ITR-3vinay.bpPas encore d'évaluation

- Form3 2007 08Document9 pagesForm3 2007 08api-3850174Pas encore d'évaluation

- Form2 2007 08Document8 pagesForm2 2007 08api-3850174Pas encore d'évaluation

- Form3 2008 09Document9 pagesForm3 2008 09api-3850174Pas encore d'évaluation

- Itr-V: Income Tax Return Verification Form IndianDocument1 pageItr-V: Income Tax Return Verification Form Indianapi-25886395Pas encore d'évaluation

- ITR-3 Indian Income Tax Return: Part A-GENDocument14 pagesITR-3 Indian Income Tax Return: Part A-GENHarishPas encore d'évaluation

- Itr-1 A.y.2021-22Document2 pagesItr-1 A.y.2021-22Pretty AngelPas encore d'évaluation

- Form ITR-V and Acknowledgement FinalDocument4 pagesForm ITR-V and Acknowledgement FinalHarish100% (1)

- Itr2 in Excel Format For A.Y 2011 12 Financial Year 2010 11Document12 pagesItr2 in Excel Format For A.Y 2011 12 Financial Year 2010 11Ricky ChodhaPas encore d'évaluation

- Tax return summaryDocument9 pagesTax return summaryAbhijeet DeyPas encore d'évaluation

- ITR2 English PDFDocument16 pagesITR2 English PDFavantgarde bwoyPas encore d'évaluation

- ITR Ack 2010 11Document1 pageITR Ack 2010 11Kiran Avinash Priti MhatrePas encore d'évaluation

- Form PDF 860011410060114Document2 pagesForm PDF 860011410060114prakashdebleyPas encore d'évaluation

- Deductions Under Chapter VI A (Section)Document2 pagesDeductions Under Chapter VI A (Section)Vikas KumarPas encore d'évaluation

- Sahaj Individual Income Tax Return Assessment Year 2 0 16 - 1 7Document13 pagesSahaj Individual Income Tax Return Assessment Year 2 0 16 - 1 7Ganesh Babu SwaminathanPas encore d'évaluation

- Itr2 in Excel Format Taxguru - inDocument9 pagesItr2 in Excel Format Taxguru - inVishwaPas encore d'évaluation

- Form PDF 468763070040922Document6 pagesForm PDF 468763070040922kxd7mknq2fPas encore d'évaluation

- Form PDF 338831280310722Document6 pagesForm PDF 338831280310722Sumit SainiPas encore d'évaluation

- Receipt No/ Date Seal and Signature of Receiving OfficialDocument10 pagesReceipt No/ Date Seal and Signature of Receiving OfficialRAMAPPA100% (2)

- Form PDF 658202480080622Document6 pagesForm PDF 658202480080622Chandrasekhar NandigamPas encore d'évaluation

- Itr-V 2 0 0 9 - 1 0: Indian Income Tax Return Verification Form Assessment YearDocument10 pagesItr-V 2 0 0 9 - 1 0: Indian Income Tax Return Verification Form Assessment YearranaonlinePas encore d'évaluation

- Form PDF 616972870051022Document6 pagesForm PDF 616972870051022Manish AroraPas encore d'évaluation

- ITR Form-1 (Sahaj)Document1 pageITR Form-1 (Sahaj)NDTVPas encore d'évaluation

- Form PDF 638844880230723Document8 pagesForm PDF 638844880230723Srikanth Chowdary DarePas encore d'évaluation

- Form PDF 358979100180620Document10 pagesForm PDF 358979100180620Sajan JhaPas encore d'évaluation

- Form For TaxationDocument6 pagesForm For TaxationAjay PanghalPas encore d'évaluation

- ITR 4 SUGAM filing acknowledgement for AY 2020-21Document9 pagesITR 4 SUGAM filing acknowledgement for AY 2020-21SHAHABUDDIN ANSARIPas encore d'évaluation

- Form PDF 863074460241222Document6 pagesForm PDF 863074460241222Sandeep KumarPas encore d'évaluation

- Indian Income Tax Return Assessment Year 2021 - 22: SugamDocument12 pagesIndian Income Tax Return Assessment Year 2021 - 22: SugamArihant SatpathyPas encore d'évaluation

- Case Study-5 PDFDocument26 pagesCase Study-5 PDFAbhi rajouraPas encore d'évaluation

- Sahaj Individual Income Tax Return Assessment Year 2 0 17 - 1 8Document13 pagesSahaj Individual Income Tax Return Assessment Year 2 0 17 - 1 8Ganesh Babu SwaminathanPas encore d'évaluation

- Form PDF 154793880270722Document7 pagesForm PDF 154793880270722Akhila PanjalaPas encore d'évaluation

- CBDT notifies simplified one-page ITR Form 1 for FY 2017-18Document2 pagesCBDT notifies simplified one-page ITR Form 1 for FY 2017-18mahenderreddybPas encore d'évaluation

- Form PDF 689751510220622Document6 pagesForm PDF 689751510220622Asif EbrahimPas encore d'évaluation

- Itr1 PreviewDocument9 pagesItr1 Previewesha sharmaPas encore d'évaluation

- ITR-2 Indian Income Tax Return: Part A-GENDocument13 pagesITR-2 Indian Income Tax Return: Part A-GENHarish100% (1)

- Receipt No/ Date Seal and Signature of Receiving OfficialDocument4 pagesReceipt No/ Date Seal and Signature of Receiving Officialtsrahod@yahoo.comPas encore d'évaluation

- Form PDF 771791780090722Document6 pagesForm PDF 771791780090722manuPas encore d'évaluation

- Rktarai DetailDocument9 pagesRktarai DetailDeepak SwainPas encore d'évaluation

- Form PDF 820116700251122Document6 pagesForm PDF 820116700251122Anonymous PzLXgCmPas encore d'évaluation

- Form PDF 230861000130623Document6 pagesForm PDF 230861000130623Sunil AccountsPas encore d'évaluation

- Form PDF 671841130150622Document6 pagesForm PDF 671841130150622RajeshKannaSundrapandianPas encore d'évaluation

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 137628670080121 Assessment Year: 2020-21Document7 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 137628670080121 Assessment Year: 2020-21Gana C RoverPas encore d'évaluation

- Indian Income Tax Return for IndividualsDocument9 pagesIndian Income Tax Return for IndividualsGood NamPas encore d'évaluation

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsD'EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsPas encore d'évaluation

- Latest Income Tax Exemptions FY 2017-18 - AY 2018-19 - Tax DeductionsDocument90 pagesLatest Income Tax Exemptions FY 2017-18 - AY 2018-19 - Tax DeductionsTambi ThambiPas encore d'évaluation

- 2nd Semester Income Taxation Module 5 Classification of TaxpayersDocument5 pages2nd Semester Income Taxation Module 5 Classification of TaxpayersMaryrose SumulongPas encore d'évaluation

- GGBS InvoiceDocument4 pagesGGBS InvoiceNitin SapkalPas encore d'évaluation

- RI22507945 - Dec 28 2022 - 183245Document2 pagesRI22507945 - Dec 28 2022 - 183245vijayPas encore d'évaluation

- Catalogue Valves AhmedabadDocument15 pagesCatalogue Valves AhmedabadDipak DhamnaniPas encore d'évaluation

- Calculate Capital Gains Tax on Real Property Sales and Principal ResidencesDocument20 pagesCalculate Capital Gains Tax on Real Property Sales and Principal ResidencesClang SantiagoPas encore d'évaluation

- Chapter 6 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document71 pagesChapter 6 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarPas encore d'évaluation

- Goods and Services Tax (GST) in IndiaDocument30 pagesGoods and Services Tax (GST) in IndiarupalPas encore d'évaluation

- WB07822MTI030186Document1 pageWB07822MTI030186Tia PakhiPas encore d'évaluation

- Macro Chapter 24 - Govt and Fiscal PolicyDocument34 pagesMacro Chapter 24 - Govt and Fiscal PolicyGenesis CagubcobPas encore d'évaluation

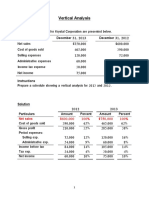

- Vertical Analysis of Financial StatementsDocument5 pagesVertical Analysis of Financial StatementsSamer IsmaelPas encore d'évaluation

- Cost of Capital 2 - The Mondigllani-Miller Theorem SummaryDocument2 pagesCost of Capital 2 - The Mondigllani-Miller Theorem SummaryAhmedPas encore d'évaluation

- Orbit C & D Block Cost SheetDocument2 pagesOrbit C & D Block Cost SheetRajesh KomatineniPas encore d'évaluation

- CAIP Notice Explains $559 Climate PaymentDocument3 pagesCAIP Notice Explains $559 Climate Paymentalex mac dougallPas encore d'évaluation

- Materials For How To Handle BIR Audit Procedures of BIR Audit - 2021 Sept 21Document83 pagesMaterials For How To Handle BIR Audit Procedures of BIR Audit - 2021 Sept 21cool_peach100% (2)

- Bid Form DRMCDocument2 pagesBid Form DRMCMelinda LlanoPas encore d'évaluation

- CIR vs. San Roque Power CorporationDocument7 pagesCIR vs. San Roque Power CorporationMIKKOPas encore d'évaluation

- Carl Conch and Mary Duval Are Married and File ADocument1 pageCarl Conch and Mary Duval Are Married and File Ahassan taimourPas encore d'évaluation

- Cinepolis & Exam 2018 - SolutionsDocument8 pagesCinepolis & Exam 2018 - Solutionsmathieu652540Pas encore d'évaluation

- Income Tax for PartnershipDocument21 pagesIncome Tax for PartnershipMaria Maganda MalditaPas encore d'évaluation

- IA2 Income TaxesDocument1 pageIA2 Income TaxesJoey Mhey BenicoPas encore d'évaluation

- Quiz 1: Tax 3 Final Period QuizzesDocument10 pagesQuiz 1: Tax 3 Final Period QuizzesJhun bondocPas encore d'évaluation

- Public FinanceDocument3 pagesPublic FinanceJorge LabantePas encore d'évaluation

- Ruling - CIR V FilinvestDocument1 pageRuling - CIR V FilinvestryanmeinPas encore d'évaluation

- Chapter 2. PITDocument77 pagesChapter 2. PITKhuất Thanh HuếPas encore d'évaluation

- Bantacs CGT Booklet Covers Capital Gains Tax RulesDocument60 pagesBantacs CGT Booklet Covers Capital Gains Tax RulesCorrimalPas encore d'évaluation

- Manila Gas Corporation v. The Collector of Internal RevenueDocument1 pageManila Gas Corporation v. The Collector of Internal RevenueRNicolo Ballesteros100% (1)

- Order-Under-Section 119-20-08-2014Document1 pageOrder-Under-Section 119-20-08-2014api-224058372Pas encore d'évaluation

- Subject: Appraisal Letter For FY 2021-22: ConfidentialDocument2 pagesSubject: Appraisal Letter For FY 2021-22: Confidentialtouseef hussainPas encore d'évaluation

- Invoice 394723 15067151Document1 pageInvoice 394723 15067151johndoesrightPas encore d'évaluation