Vous aimerez peut-être aussi

- Hotel Master Critical PathDocument14 pagesHotel Master Critical Pathtaola80% (25)

- Problems On Cash Budget MBADocument3 pagesProblems On Cash Budget MBAsafwanhossainPas encore d'évaluation

- Admin Assistant III IPCRFDocument8 pagesAdmin Assistant III IPCRFJeond Jeff88% (8)

- Egypt's Foreign Currency Crisis ExplainedDocument34 pagesEgypt's Foreign Currency Crisis ExplainedShashank VarmaPas encore d'évaluation

- Philippines fiscal policy overviewDocument4 pagesPhilippines fiscal policy overviewEmmanuel Jimenez-Bacud, CSE-Professional,BA-MA Pol Sci100% (1)

- India Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBREDocument20 pagesIndia Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBRErealtywatch108Pas encore d'évaluation

- Barangay Development CouncilDocument5 pagesBarangay Development CouncilJohny VillanuevaPas encore d'évaluation

- BOM For LGUs 2023 Edition - Fin1 - UnlockedDocument329 pagesBOM For LGUs 2023 Edition - Fin1 - UnlockedNatacia Rimorin-Dizon100% (2)

- NIFK16289689Document28 pagesNIFK16289689Yuki TakenoPas encore d'évaluation

- Pakistan's Economic Performance and Prospects in FY2014Document6 pagesPakistan's Economic Performance and Prospects in FY2014Abdul Ghaffar BhattiPas encore d'évaluation

- SA's 2013 National Budget focuses on fiscal disciplineDocument7 pagesSA's 2013 National Budget focuses on fiscal disciplineBrilliant MycriPas encore d'évaluation

- Nepal's Economic Growth, Fiscal Stability and Financial Sector ReformsDocument7 pagesNepal's Economic Growth, Fiscal Stability and Financial Sector Reformsakyadav123Pas encore d'évaluation

- Prospects 2012Document7 pagesProspects 2012IPS Sri LankaPas encore d'évaluation

- Snapshot of Bosnia and HerzegovinaDocument53 pagesSnapshot of Bosnia and HerzegovinaDejan ŠešlijaPas encore d'évaluation

- Press 20140408eaDocument7 pagesPress 20140408eaRandora LkPas encore d'évaluation

- India Union Budget 2013 PWC Analysis BookletDocument40 pagesIndia Union Budget 2013 PWC Analysis BookletsuchjazzPas encore d'évaluation

- Update On Indian Economy, March 2013Document12 pagesUpdate On Indian Economy, March 2013megaacePas encore d'évaluation

- Malaysian Economy Grows 6.4% in Q4 2012Document7 pagesMalaysian Economy Grows 6.4% in Q4 2012Yana NanaPas encore d'évaluation

- Budget PublicationDocument50 pagesBudget PublicationAmit RajputPas encore d'évaluation

- Bangladesh Economic Brief 2012 May 31Document18 pagesBangladesh Economic Brief 2012 May 31Mohammad MynoddinPas encore d'évaluation

- Regional GDP Growth Slows Further to 4.7% in 1Q12Document9 pagesRegional GDP Growth Slows Further to 4.7% in 1Q12enleePas encore d'évaluation

- Case Study On NDB and DFCCDocument34 pagesCase Study On NDB and DFCCRantharu AttanayakePas encore d'évaluation

- Pakistan Economic Survey 2011-12 PDFDocument286 pagesPakistan Economic Survey 2011-12 PDFAli RazaPas encore d'évaluation

- Monetary Policy Statement September 2013 HighlightsDocument42 pagesMonetary Policy Statement September 2013 HighlightsScorpian MouniehPas encore d'évaluation

- Country Strategy 2011-2014 MoldovaDocument21 pagesCountry Strategy 2011-2014 MoldovaBeeHoofPas encore d'évaluation

- Getting To The Core: Budget AnalysisDocument37 pagesGetting To The Core: Budget AnalysisfaizanbhamlaPas encore d'évaluation

- Bangladesh Quarterly Economic Update - September-December 2012Document29 pagesBangladesh Quarterly Economic Update - September-December 2012Asian Development BankPas encore d'évaluation

- Main Indicators: GDP, State Budget, Foreign Trade, Exchange Rate, InflationDocument5 pagesMain Indicators: GDP, State Budget, Foreign Trade, Exchange Rate, InflationUrtaBaasanjargalPas encore d'évaluation

- The World Bank Group - Tajikistan Partnership Program SnapshotDocument31 pagesThe World Bank Group - Tajikistan Partnership Program SnapshotamudaryoPas encore d'évaluation

- Therefore GDP C+ G+ I + N ExDocument10 pagesTherefore GDP C+ G+ I + N Exyashasheth17Pas encore d'évaluation

- Economic and Social Survey of Asia and The Pacific 2013 - Briefing Notes For The Launch in AnkaraDocument2 pagesEconomic and Social Survey of Asia and The Pacific 2013 - Briefing Notes For The Launch in AnkaraUNDP TürkiyePas encore d'évaluation

- Bank of Tanzania Mid-Year Monetary Policy ReviewDocument58 pagesBank of Tanzania Mid-Year Monetary Policy Reviewafzallodhi736Pas encore d'évaluation

- Acroeconomic Cenario: Source: Please See AnnexureDocument2 pagesAcroeconomic Cenario: Source: Please See AnnexureehsankabirPas encore d'évaluation

- Maybank May 2013 IssueDocument12 pagesMaybank May 2013 IssueMarlon MoncadaPas encore d'évaluation

- Pakistan's Resilient Economy Shows Signs of RecoveryDocument15 pagesPakistan's Resilient Economy Shows Signs of RecoveryMian HamzaPas encore d'évaluation

- Kinh Te 2013-2014Document2 pagesKinh Te 2013-2014Olivia TranPas encore d'évaluation

- Cambodia 1433Document60 pagesCambodia 1433Tanmay SahaiPas encore d'évaluation

- Vanuatu Article IV Consultation 2013Document52 pagesVanuatu Article IV Consultation 2013Kyren GreiggPas encore d'évaluation

- State of EconomyDocument21 pagesState of EconomyHarsh KediaPas encore d'évaluation

- Investment Growth Factors Pakistan EconomyDocument5 pagesInvestment Growth Factors Pakistan EconomyaoulakhPas encore d'évaluation

- Economics GNP MalaysiaDocument14 pagesEconomics GNP Malaysiakayrul700% (1)

- Updated Sept 10 2013 - EB July 2013Document120 pagesUpdated Sept 10 2013 - EB July 2013Kyren GreiggPas encore d'évaluation

- Budget 2015-16Document100 pagesBudget 2015-16bazitPas encore d'évaluation

- 2012 Budget PublicationDocument71 pages2012 Budget PublicationPushpa PatilPas encore d'évaluation

- Update On Indian Economy November 2013 - Mega Ace ConsultancyDocument10 pagesUpdate On Indian Economy November 2013 - Mega Ace ConsultancyMegaAceConsultancyPas encore d'évaluation

- Assignment OnDocument30 pagesAssignment OnMashruk AhmedPas encore d'évaluation

- China's Economic Trend Under The Impact of The EpidemicDocument10 pagesChina's Economic Trend Under The Impact of The EpidemicRumi AzhariPas encore d'évaluation

- UBL Financial StatementsDocument23 pagesUBL Financial StatementsUsmAn MajeedPas encore d'évaluation

- India's Economic Position Despite Slowdown in GrowthDocument21 pagesIndia's Economic Position Despite Slowdown in GrowththakursahbPas encore d'évaluation

- Full AssignmentDocument37 pagesFull AssignmentMd Sifat Khan83% (6)

- The Ghanaian Cedi Depreciation - The Way To GoDocument5 pagesThe Ghanaian Cedi Depreciation - The Way To GoIsaac MensahPas encore d'évaluation

- State of The Economy 2011Document8 pagesState of The Economy 2011agarwaldipeshPas encore d'évaluation

- Monetary Policy Statement: State Bank of PakistanDocument32 pagesMonetary Policy Statement: State Bank of Pakistanbenicepk1329Pas encore d'évaluation

- Prospects 2010Document5 pagesProspects 2010IPS Sri LankaPas encore d'évaluation

- DirectorDocument49 pagesDirectorrohitkoliPas encore d'évaluation

- Press 20130117eDocument2 pagesPress 20130117eran2013Pas encore d'évaluation

- Fiscal Situation of PakistanDocument9 pagesFiscal Situation of PakistanMahnoor ZebPas encore d'évaluation

- Global Economic Prospects January 2013Document16 pagesGlobal Economic Prospects January 2013Dhananjaya HathurusinghePas encore d'évaluation

- Mustard Garment Industry: 1. Remittance 2. Inflation 3. Exchange Rate 4. GDP GrowthDocument9 pagesMustard Garment Industry: 1. Remittance 2. Inflation 3. Exchange Rate 4. GDP GrowthTanjeemPas encore d'évaluation

- Economic Analysis of IndiaDocument120 pagesEconomic Analysis of Indiamonish147852Pas encore d'évaluation

- Madagascar 2013Document15 pagesMadagascar 2013HayZara MadagascarPas encore d'évaluation

- HS101 ProjectDocument5 pagesHS101 ProjectRevathi KotniPas encore d'évaluation

- Republic of the Congo Economic OverviewDocument15 pagesRepublic of the Congo Economic OverviewKunal BagadePas encore d'évaluation

- LNG Investment in Mozamibique (Final)Document15 pagesLNG Investment in Mozamibique (Final)Denis KipkoechPas encore d'évaluation

- Thailand's Economic Performance in Q4 and Outlook For 2012 - 0Document36 pagesThailand's Economic Performance in Q4 and Outlook For 2012 - 0thailand2dayPas encore d'évaluation

- Global Market Update - 04 09 2015 PDFDocument6 pagesGlobal Market Update - 04 09 2015 PDFRandora LkPas encore d'évaluation

- Weekly Update 04.09.2015 PDFDocument2 pagesWeekly Update 04.09.2015 PDFRandora LkPas encore d'évaluation

- Weekly Foreign Holding & Block Trade Update: Net Buying Net SellingDocument4 pagesWeekly Foreign Holding & Block Trade Update: Net Buying Net SellingRandora LkPas encore d'évaluation

- Wei 20150904 PDFDocument18 pagesWei 20150904 PDFRandora LkPas encore d'évaluation

- 03 September 2015 PDFDocument9 pages03 September 2015 PDFRandora LkPas encore d'évaluation

- Press 20150831ebDocument2 pagesPress 20150831ebRandora LkPas encore d'évaluation

- ICRA Lanka Assigns (SL) BBB-rating With Positive Outlook To Sanasa Development Bank PLCDocument3 pagesICRA Lanka Assigns (SL) BBB-rating With Positive Outlook To Sanasa Development Bank PLCRandora LkPas encore d'évaluation

- Daily 01 09 2015 PDFDocument4 pagesDaily 01 09 2015 PDFRandora LkPas encore d'évaluation

- Press 20150831ea PDFDocument1 pagePress 20150831ea PDFRandora LkPas encore d'évaluation

- Global Market Update - 04 09 2015 PDFDocument6 pagesGlobal Market Update - 04 09 2015 PDFRandora LkPas encore d'évaluation

- CCPI - Press Release - August2015 PDFDocument5 pagesCCPI - Press Release - August2015 PDFRandora LkPas encore d'évaluation

- Sri0Lanka000Re0ounting0and0auditing PDFDocument44 pagesSri0Lanka000Re0ounting0and0auditing PDFRandora LkPas encore d'évaluation

- Results Update Sector Summary - Jun 2015 PDFDocument2 pagesResults Update Sector Summary - Jun 2015 PDFRandora LkPas encore d'évaluation

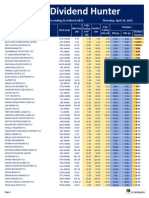

- Dividend Hunter - Apr 2015 PDFDocument7 pagesDividend Hunter - Apr 2015 PDFRandora LkPas encore d'évaluation

- Earnings & Market Returns Forecast - Jun 2015 PDFDocument4 pagesEarnings & Market Returns Forecast - Jun 2015 PDFRandora LkPas encore d'évaluation

- Earnings Update March Quarter 2015 05 06 2015 PDFDocument24 pagesEarnings Update March Quarter 2015 05 06 2015 PDFRandora LkPas encore d'évaluation

- BRS Monthly (March 2015 Edition) PDFDocument8 pagesBRS Monthly (March 2015 Edition) PDFRandora LkPas encore d'évaluation

- Results Update For All Companies - Jun 2015 PDFDocument9 pagesResults Update For All Companies - Jun 2015 PDFRandora LkPas encore d'évaluation

- Dividend Hunter - Mar 2015 PDFDocument7 pagesDividend Hunter - Mar 2015 PDFRandora LkPas encore d'évaluation

- Daily - 23 04 2015 PDFDocument4 pagesDaily - 23 04 2015 PDFRandora LkPas encore d'évaluation

- Dividend Hunter - Mar 2015 PDFDocument7 pagesDividend Hunter - Mar 2015 PDFRandora LkPas encore d'évaluation

- Microfinance Regulatory Model PDFDocument5 pagesMicrofinance Regulatory Model PDFRandora LkPas encore d'évaluation

- GIH Capital Monthly - Mar 2015 PDFDocument11 pagesGIH Capital Monthly - Mar 2015 PDFRandora LkPas encore d'évaluation

- CRL Corporate Update - 22 04 2015 - Upgrade To A Strong BUY PDFDocument12 pagesCRL Corporate Update - 22 04 2015 - Upgrade To A Strong BUY PDFRandora LkPas encore d'évaluation

- Janashakthi Insurance Company PLC - (JINS) - Q4 FY 14 - SELL PDFDocument9 pagesJanashakthi Insurance Company PLC - (JINS) - Q4 FY 14 - SELL PDFRandora LkPas encore d'évaluation

- N D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Document5 pagesN D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Randora LkPas encore d'évaluation

- Chevron Lubricants Lanka PLC (LLUB) - Q4 FY 14 - SELL PDFDocument9 pagesChevron Lubricants Lanka PLC (LLUB) - Q4 FY 14 - SELL PDFRandora LkPas encore d'évaluation

- The Morality of Capitalism Sri LankiaDocument32 pagesThe Morality of Capitalism Sri LankiaRandora LkPas encore d'évaluation

- Weekly Foreign Holding & Block Trade Update - 02 04 2015 PDFDocument4 pagesWeekly Foreign Holding & Block Trade Update - 02 04 2015 PDFRandora LkPas encore d'évaluation

- Daily Stock Watch 08.04.2015 PDFDocument9 pagesDaily Stock Watch 08.04.2015 PDFRandora LkPas encore d'évaluation

- New Haven Budget 2020-21Document485 pagesNew Haven Budget 2020-21Helen Bennett100% (1)

- Ethiopia Report - Jan 2020Document71 pagesEthiopia Report - Jan 2020Shime HI RayaPas encore d'évaluation

- Master's Thesis - Factors Affecting Theatrical Success of Films: An Empirical ReviewDocument45 pagesMaster's Thesis - Factors Affecting Theatrical Success of Films: An Empirical Reviewsiddharth_uPas encore d'évaluation

- Pork BarrelDocument2 pagesPork BarrelJunjun16 JayzonPas encore d'évaluation

- Edney Company Employs A Standard Cost System For Product CostingDocument2 pagesEdney Company Employs A Standard Cost System For Product CostingAmit PandeyPas encore d'évaluation

- Evaluation GridDocument6 pagesEvaluation GridDaniel BWINO AMANYAPas encore d'évaluation

- Finance Process FlowDocument13 pagesFinance Process FlowHasan NasirPas encore d'évaluation

- CH 1 Gov - AccountingDocument16 pagesCH 1 Gov - AccountingMohamed DiabPas encore d'évaluation

- Boulder City Tentative Capital Improvement Plan Presentation and Executive SummaryDocument46 pagesBoulder City Tentative Capital Improvement Plan Presentation and Executive SummaryBoulder City ReviewPas encore d'évaluation

- Accounting for Government Budgetary AccountsDocument33 pagesAccounting for Government Budgetary AccountsRia BagoPas encore d'évaluation

- Abstract: Budget Process and Performance of Local Governments in IndonesiaDocument1 pageAbstract: Budget Process and Performance of Local Governments in IndonesiaHarryanto EndhyPas encore d'évaluation

- Master Budget Example MC Watters AIP8-13Document2 pagesMaster Budget Example MC Watters AIP8-13Muhammed muhabaPas encore d'évaluation

- Zero Based Budgeting OverviewDocument4 pagesZero Based Budgeting OverviewSazidur RahmanPas encore d'évaluation

- Colloquim Jan 29 Abstract Corrected Jan 6Document87 pagesColloquim Jan 29 Abstract Corrected Jan 6bryan001935Pas encore d'évaluation

- Cost accounting and financial managementDocument22 pagesCost accounting and financial managementEsha Bhardwaj100% (1)

- Capacity Assessment Checklist (CACHE) For CSO/NGODocument1 pageCapacity Assessment Checklist (CACHE) For CSO/NGOTaskin Reza KhalidPas encore d'évaluation

- The Importance and Use of Budgets Within An OrganizationDocument6 pagesThe Importance and Use of Budgets Within An OrganizationAndrei MunteanuPas encore d'évaluation

- PESS and PCER Report PDFDocument29 pagesPESS and PCER Report PDFEm Calvento MacaraegPas encore d'évaluation

- City of Oneida Department SalariesDocument1 pageCity of Oneida Department SalariesOneida Daily DispatchPas encore d'évaluation

- Third Outline Perspective Plan (Opp3) Chapter 3 - Macro Economic PerspectiveDocument24 pagesThird Outline Perspective Plan (Opp3) Chapter 3 - Macro Economic PerspectiveChristy BrownPas encore d'évaluation

- Review Materials Chapters 8, 10, 3 & 4 Term 3 Y18-19 PDFDocument19 pagesReview Materials Chapters 8, 10, 3 & 4 Term 3 Y18-19 PDFKrizelle Anne TaguinodPas encore d'évaluation

- Consumer Theory Practice ProblemsDocument22 pagesConsumer Theory Practice Problemsben114Pas encore d'évaluation

- DLG Chapter 4 (Combined)Document14 pagesDLG Chapter 4 (Combined)Puth RathanaPas encore d'évaluation