Vous aimerez peut-être aussi

- XTO Energy Liquidity and Solvency AnalysisDocument6 pagesXTO Energy Liquidity and Solvency AnalysisCarneadesPas encore d'évaluation

- Components of RNOA - Profit Margin and Asset TurnoverDocument3 pagesComponents of RNOA - Profit Margin and Asset TurnoverCarneadesPas encore d'évaluation

- Basic V Diluted EPSDocument1 pageBasic V Diluted EPSCarneadesPas encore d'évaluation

- Introduction To Credit Risk Analysis: Debt To Equity RatioDocument3 pagesIntroduction To Credit Risk Analysis: Debt To Equity RatioCarneadesPas encore d'évaluation

- Vertical Analysis of Financial Statements - Pepsi V CokeDocument2 pagesVertical Analysis of Financial Statements - Pepsi V CokeCarneades33% (3)

- Net Operating Profit Margin (NOPM)Document1 pageNet Operating Profit Margin (NOPM)CarneadesPas encore d'évaluation

- America's Healthy Future Act of 2009Document223 pagesAmerica's Healthy Future Act of 2009KFFHealthNewsPas encore d'évaluation

- SP/Case Shiller Index Through June 2009Document1 pageSP/Case Shiller Index Through June 2009CarneadesPas encore d'évaluation

- OCF To CapexDocument1 pageOCF To CapexCarneadesPas encore d'évaluation

- Duke Energy Allowances To ReceivablesDocument1 pageDuke Energy Allowances To ReceivablesCarneadesPas encore d'évaluation

- Aetna Q2 09 Financial ResultsDocument14 pagesAetna Q2 09 Financial ResultsCarneadesPas encore d'évaluation

- Earnings Quality Analysis - Operating Cash Flow To Net IncomeDocument3 pagesEarnings Quality Analysis - Operating Cash Flow To Net IncomeCarneadesPas encore d'évaluation

- OCF To Current LiabilitiesDocument1 pageOCF To Current LiabilitiesCarneadesPas encore d'évaluation

- Housing Starts August 2009Document1 pageHousing Starts August 2009CarneadesPas encore d'évaluation

- Monthly CMBS Delinquency August 2009Document1 pageMonthly CMBS Delinquency August 2009CarneadesPas encore d'évaluation

- Democrats and Out of State Campaign ContributionsDocument3 pagesDemocrats and Out of State Campaign ContributionsCarneadesPas encore d'évaluation

- The SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsDocument124 pagesThe SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsCarneadesPas encore d'évaluation

- RealPoint CMBS Delinquency Report July 2009Document15 pagesRealPoint CMBS Delinquency Report July 2009Carneades100% (1)

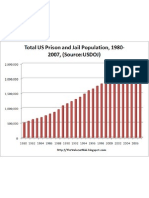

- Prison Population As % of US Population 1980-2007Document1 pagePrison Population As % of US Population 1980-2007CarneadesPas encore d'évaluation

- Social Security COLA History 1999-2009Document1 pageSocial Security COLA History 1999-2009CarneadesPas encore d'évaluation

- Semiconductor Data Through July 2009Document2 pagesSemiconductor Data Through July 2009CarneadesPas encore d'évaluation

- ENSYS Cap and Trade Briefing 8-20-09Document25 pagesENSYS Cap and Trade Briefing 8-20-09CarneadesPas encore d'évaluation

- July 2009 Housing Starts 2005-PresentDocument1 pageJuly 2009 Housing Starts 2005-PresentCarneadesPas encore d'évaluation

- TIC Data June 2009Document1 pageTIC Data June 2009CarneadesPas encore d'évaluation

- US Prison Population 1980-2007Document1 pageUS Prison Population 1980-2007CarneadesPas encore d'évaluation

- Medicare Modernization ActDocument416 pagesMedicare Modernization ActCarneadesPas encore d'évaluation

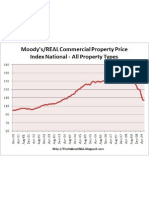

- Moodys CPPI August 2009Document1 pageMoodys CPPI August 2009CarneadesPas encore d'évaluation

- July 2009 Housing Starts 1959-PresentDocument1 pageJuly 2009 Housing Starts 1959-PresentCarneadesPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Gartner Magic Quadrant Report For SFA - Aug 2016Document31 pagesGartner Magic Quadrant Report For SFA - Aug 2016Francisco LSPas encore d'évaluation

- Cost Study On SHEET-FED PRESS OPERATIONSDocument525 pagesCost Study On SHEET-FED PRESS OPERATIONSalexbilchuk100% (1)

- Faunus Homebrew PDFDocument3 pagesFaunus Homebrew PDFPaul FernandezPas encore d'évaluation

- Kapil Choudhary: Personal ProfileDocument2 pagesKapil Choudhary: Personal ProfileAishwarya GoelPas encore d'évaluation

- 1CKCDocument44 pages1CKCsema2210100% (1)

- One Dollar and Eighty-Seven CentsDocument3 pagesOne Dollar and Eighty-Seven CentsAmna RanaPas encore d'évaluation

- Atlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaDocument86 pagesAtlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaEdilson Silva100% (1)

- Technology Theatres, Plays and PerformanceDocument48 pagesTechnology Theatres, Plays and PerformanceHannah Williams WaltonPas encore d'évaluation

- IEEE Romania SectionDocument14 pagesIEEE Romania SectionLucian TomaPas encore d'évaluation

- Senarai Akta A MalaysiaDocument8 pagesSenarai Akta A MalaysiawswmadihiPas encore d'évaluation

- Very Important General Knowledge MCQs With DetailsDocument13 pagesVery Important General Knowledge MCQs With DetailsNiaz AsgharPas encore d'évaluation

- Dot Net TricksDocument101 pagesDot Net TrickssathishmnmPas encore d'évaluation

- Standard Operating Procedures in Drafting July1Document21 pagesStandard Operating Procedures in Drafting July1Edel VilladolidPas encore d'évaluation

- Danamma Vs AmarDocument13 pagesDanamma Vs AmarParthiban SekarPas encore d'évaluation

- Tata Steel Europe LTDDocument22 pagesTata Steel Europe LTDEntertainment OverloadedPas encore d'évaluation

- Microsoft Lumia 950 XL - Unlocked (Black)Document8 pagesMicrosoft Lumia 950 XL - Unlocked (Black)Dawood AhmedPas encore d'évaluation

- Gann Trding PDFDocument9 pagesGann Trding PDFMayur KasarPas encore d'évaluation

- 2463-Article Text-6731-1-10-20220712Document18 pages2463-Article Text-6731-1-10-20220712Okto LedohPas encore d'évaluation

- 1927 To 1939 New PDFDocument8 pages1927 To 1939 New PDFahmed razaPas encore d'évaluation

- Samsung Galaxy Beam GT I8530 User ManualDocument172 pagesSamsung Galaxy Beam GT I8530 User ManualFirdaus AhmadPas encore d'évaluation

- The Lucid Dream Exchange Magazine Issue 36Document36 pagesThe Lucid Dream Exchange Magazine Issue 36api-384230967% (3)

- What Got You Here Won't Get You ThereDocument4 pagesWhat Got You Here Won't Get You ThereAbdi50% (6)

- Physical and Chemical Changes WorksheetDocument2 pagesPhysical and Chemical Changes Worksheetisabe;llaPas encore d'évaluation

- Erinnerungsmotive in Wagner's Der Ring Des NibelungenDocument14 pagesErinnerungsmotive in Wagner's Der Ring Des NibelungenLaur MatysPas encore d'évaluation

- Programme Guide - PGDMCH PDFDocument58 pagesProgramme Guide - PGDMCH PDFNJMU 2006Pas encore d'évaluation

- IdentifyDocument40 pagesIdentifyLeonard Kenshin LianzaPas encore d'évaluation

- ExtractedRA - CIVILENG - MANILA - Nov2017 RevDocument62 pagesExtractedRA - CIVILENG - MANILA - Nov2017 Revkelvin jake castroPas encore d'évaluation

- The BoxDocument6 pagesThe BoxDemian GaylordPas encore d'évaluation

- 01 B744 B1 ATA 23 Part2Document170 pages01 B744 B1 ATA 23 Part2NadirPas encore d'évaluation

- Take The MMPI Test Online For Free: Hypnosis Articles and InformationDocument14 pagesTake The MMPI Test Online For Free: Hypnosis Articles and InformationUMINAH0% (1)