Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- 0547 s06 TN 3Document20 pages0547 s06 TN 3mstudy123456Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- 0486 w09 QP 4Document36 pages0486 w09 QP 4mstudy123456Pas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- 0654 w04 Ms 6Document6 pages0654 w04 Ms 6mstudy123456Pas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Literature (English) : International General Certificate of Secondary EducationDocument1 pageLiterature (English) : International General Certificate of Secondary Educationmstudy123456Pas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Frequently Asked Questions: A/AS Level Sociology (9699)Document1 pageFrequently Asked Questions: A/AS Level Sociology (9699)mstudy123456Pas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- 9694 s11 QP 21Document8 pages9694 s11 QP 21mstudy123456Pas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- 9694 w10 QP 23Document8 pages9694 w10 QP 23mstudy123456Pas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- English Language: PAPER 1 Passages For CommentDocument8 pagesEnglish Language: PAPER 1 Passages For Commentmstudy123456Pas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- 9693 s12 QP 2Document12 pages9693 s12 QP 2mstudy123456Pas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- University of Cambridge International Examinations General Certificate of Education Advanced LevelDocument2 pagesUniversity of Cambridge International Examinations General Certificate of Education Advanced Levelmstudy123456Pas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- 8780 w12 QP 1Document16 pages8780 w12 QP 1mstudy123456Pas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- 8693 English Language: MARK SCHEME For The October/November 2009 Question Paper For The Guidance of TeachersDocument4 pages8693 English Language: MARK SCHEME For The October/November 2009 Question Paper For The Guidance of Teachersmstudy123456Pas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- 9719 SPANISH 8685 Spanish Language: MARK SCHEME For The May/June 2009 Question Paper For The Guidance of TeachersDocument3 pages9719 SPANISH 8685 Spanish Language: MARK SCHEME For The May/June 2009 Question Paper For The Guidance of Teachersmstudy123456Pas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- 8679 w04 ErDocument4 pages8679 w04 Ermstudy123456Pas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- First Language Spanish: Paper 8665/22 Reading and WritingDocument6 pagesFirst Language Spanish: Paper 8665/22 Reading and Writingmstudy123456Pas encore d'évaluation

- Dpa20033 Chapter 1Document31 pagesDpa20033 Chapter 1King Fernandez100% (1)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Accounting IG Section 1.1 The Fundamentals of Accounting Section 1.2 The Accounting EquationDocument7 pagesAccounting IG Section 1.1 The Fundamentals of Accounting Section 1.2 The Accounting EquationJuné MaraisPas encore d'évaluation

- Bba SyllabusDocument19 pagesBba SyllabusamitpriyashankarPas encore d'évaluation

- Balance of Payments AccountingDocument20 pagesBalance of Payments AccountingWilly AndersonPas encore d'évaluation

- Report of Collections and Deposit orDocument2 pagesReport of Collections and Deposit orLILIBETH BACUDPas encore d'évaluation

- Accounting MaterialDocument161 pagesAccounting MaterialMithun Nair MPas encore d'évaluation

- Clerk 2019 Main PaperDocument29 pagesClerk 2019 Main PaperSaifi KhanPas encore d'évaluation

- Accounting 100 First ChapterDocument9 pagesAccounting 100 First ChapterMarjon VillanuevaPas encore d'évaluation

- Tally Erp 9.0 Material Sample Reports in Tally - Erp 9Document150 pagesTally Erp 9.0 Material Sample Reports in Tally - Erp 9Raghavendra yadav KMPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Accounting Fundamentals: Oubs023114, Oubs002111, Oubs003111, Oubs022111 Oubs009111, Oubs010113, Oubs008111, Oubs0021113Document113 pagesAccounting Fundamentals: Oubs023114, Oubs002111, Oubs003111, Oubs022111 Oubs009111, Oubs010113, Oubs008111, Oubs0021113Valérie CamanguePas encore d'évaluation

- Accountancy (Code No.055) : Class-XI (2020-21)Document8 pagesAccountancy (Code No.055) : Class-XI (2020-21)ALAQMARRAJPas encore d'évaluation

- Investment Advisory Business Plan TemplateDocument22 pagesInvestment Advisory Business Plan TemplatesolomonPas encore d'évaluation

- Solution Manual For Microeconomics 15th Canadian Edition Campbell R Mcconnell Stanley L Brue Sean Masaki Flynn Tom BarbieroDocument34 pagesSolution Manual For Microeconomics 15th Canadian Edition Campbell R Mcconnell Stanley L Brue Sean Masaki Flynn Tom Barbierowisardspoliate.ybjnr100% (47)

- JKSSB Finance SyllabusDocument4 pagesJKSSB Finance Syllabusangel arushiPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- HA3032 AuditingDocument9 pagesHA3032 AuditingAayam SubediPas encore d'évaluation

- Feedback: Not Answered Marked Out of 1.00Document30 pagesFeedback: Not Answered Marked Out of 1.00Mark John Paul CablingPas encore d'évaluation

- 663 Chemical TechnologyDocument28 pages663 Chemical TechnologyAnonymous okVyZFmqqXPas encore d'évaluation

- Fundamentals of AccountingDocument73 pagesFundamentals of AccountingCarmina Dongcayan100% (2)

- Auditing Book Gobind Kumar JhaDocument145 pagesAuditing Book Gobind Kumar Jhabinay chaudharyPas encore d'évaluation

- MMPC004 Book PDFDocument422 pagesMMPC004 Book PDFShivam ShivamPas encore d'évaluation

- Study Note 3, Page 148-196Document49 pagesStudy Note 3, Page 148-196samstarmoonPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Guidelines For The Administration of School FinancesDocument27 pagesGuidelines For The Administration of School FinancesLeilani RomaniaPas encore d'évaluation

- REVIEWER AACA (Midterm)Document15 pagesREVIEWER AACA (Midterm)cynthia karylle natividadPas encore d'évaluation

- Reviewer For Bookkeeping NCIIIDocument18 pagesReviewer For Bookkeeping NCIIIAngelica Faye95% (20)

- FA - FFA Syllabus and Study Guide 2020-21 FINAL PDFDocument17 pagesFA - FFA Syllabus and Study Guide 2020-21 FINAL PDFShah SujitPas encore d'évaluation

- Suspense Accounts and Error Correction Are Popular Topics For Examiners Because They Test Understanding of Bookkeeping Principles So WellDocument12 pagesSuspense Accounts and Error Correction Are Popular Topics For Examiners Because They Test Understanding of Bookkeeping Principles So WellocalmaviliPas encore d'évaluation

- (Revised) Officer of Bank Financial Institution AffidavitDocument1 page(Revised) Officer of Bank Financial Institution Affidavitin1or100% (8)

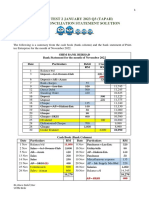

- Acc117 Test 2 Jan2023 - Tapah BRS SSDocument2 pagesAcc117 Test 2 Jan2023 - Tapah BRS SSNajmuddin Azuddin100% (1)

- SOL Financial Accounting Unit I-V PDFDocument242 pagesSOL Financial Accounting Unit I-V PDFshiv - aayPas encore d'évaluation

- ABM FABM1 AIRs LM Q4-M9 AdustingEntriesOfServiceBusDocument19 pagesABM FABM1 AIRs LM Q4-M9 AdustingEntriesOfServiceBusKarl Vincent DulayPas encore d'évaluation

- Getting to Yes: How to Negotiate Agreement Without Giving InD'EverandGetting to Yes: How to Negotiate Agreement Without Giving InÉvaluation : 4 sur 5 étoiles4/5 (652)