Vous aimerez peut-être aussi

- Who Killed GodDocument5 pagesWho Killed GodVikram PatwaPas encore d'évaluation

- Why Americans Pay More For Health CareDocument12 pagesWhy Americans Pay More For Health CareVikram PatwaPas encore d'évaluation

- Home Aryan Invasion Theory: Quotes Basics Science History Social Other SearchDocument68 pagesHome Aryan Invasion Theory: Quotes Basics Science History Social Other SearchShailesh GpPas encore d'évaluation

- A Healthier Future For IndiaDocument5 pagesA Healthier Future For IndiaVikram PatwaPas encore d'évaluation

- Insurance A SummaryDocument17 pagesInsurance A SummaryVikram PatwaPas encore d'évaluation

- TowardsCircularEconomy Report 2014Document64 pagesTowardsCircularEconomy Report 2014rfmoraes16Pas encore d'évaluation

- Cat ModellingDocument15 pagesCat ModellingVikram PatwaPas encore d'évaluation

- Auto InsuranceDocument22 pagesAuto InsuranceVikram PatwaPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Pre-Feasibility Study, Feasibility Study & Business PlanDocument16 pagesPre-Feasibility Study, Feasibility Study & Business PlanNyle Joy DalunazaPas encore d'évaluation

- House of Representatives: Republic of The Philippines Quezon City, Metro ManilaDocument13 pagesHouse of Representatives: Republic of The Philippines Quezon City, Metro ManilaGlomarie GonayonPas encore d'évaluation

- 86 698 1 PBDocument21 pages86 698 1 PBSemen PutihPas encore d'évaluation

- Marketing goals to drive growthDocument4 pagesMarketing goals to drive growthYashwanth YashasPas encore d'évaluation

- Summary Chapters 1-5 (Kotler)Document7 pagesSummary Chapters 1-5 (Kotler)Anthonette TanPas encore d'évaluation

- Integreted Case StudyDocument7 pagesIntegreted Case StudyShihab UddinPas encore d'évaluation

- BS 1449-1 Steel Plate, Sheet & Strip 1983 PDFDocument39 pagesBS 1449-1 Steel Plate, Sheet & Strip 1983 PDFSaad Ayub0% (1)

- Session - 046Document8 pagesSession - 046Abcdef GhPas encore d'évaluation

- Emtel LTD V The Information and Communication Technologies AuthorityDocument89 pagesEmtel LTD V The Information and Communication Technologies AuthorityDefimediagroup LdmgPas encore d'évaluation

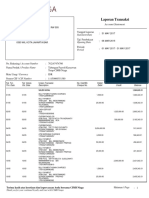

- Kepada / To Laporan Transaksi Account StatementDocument3 pagesKepada / To Laporan Transaksi Account StatementBulir SenjaPas encore d'évaluation

- Skill Seminar: Burn Baby Burn - Alexander Pinter: Lesson 1 - 18.05.2020 Business ModelDocument3 pagesSkill Seminar: Burn Baby Burn - Alexander Pinter: Lesson 1 - 18.05.2020 Business ModelHarald MeiserPas encore d'évaluation

- Borehole Drilling - Planning, Contracting & Management: A UNICEF ToolkitDocument17 pagesBorehole Drilling - Planning, Contracting & Management: A UNICEF Toolkithindreen mohammedPas encore d'évaluation

- South African Airways v. CIRDocument3 pagesSouth African Airways v. CIRHailin Quintos67% (3)

- APEC Thought Leadership Publication 2013Document98 pagesAPEC Thought Leadership Publication 2013Chris AtkinsPas encore d'évaluation

- Tradisi Buwuh Dalam Perspektif Akuntansi Piutangdan Hibahdi KecamatanLowokwaru Kota MalangDocument10 pagesTradisi Buwuh Dalam Perspektif Akuntansi Piutangdan Hibahdi KecamatanLowokwaru Kota MalangAdley RamliPas encore d'évaluation

- 2Document53 pages2maxz100% (1)

- Thermo Fisher ScientificDocument11 pagesThermo Fisher ScientificDhruvesh ModyPas encore d'évaluation

- Product Manager QuestionsDocument4 pagesProduct Manager Questionsartsan3Pas encore d'évaluation

- 2022 - 02 - 03 Revision in Rates of NSSDocument10 pages2022 - 02 - 03 Revision in Rates of NSSKhawaja Burhan0% (2)

- Lean Maintenance Management: 1-Course OverviewDocument9 pagesLean Maintenance Management: 1-Course OverviewtetoPas encore d'évaluation

- RealEstateFinancialModelingCourse EXPERIMENTDocument12 pagesRealEstateFinancialModelingCourse EXPERIMENTVijay Singh100% (1)

- VERITAS Storage Foundation 5.0 For Linux - FundamentalsDocument400 pagesVERITAS Storage Foundation 5.0 For Linux - FundamentalsMaria Ghazalia CameroonPas encore d'évaluation

- Quality Assurance in SurveysDocument32 pagesQuality Assurance in SurveysDurga Prasad PahariPas encore d'évaluation

- Maths McqsDocument10 pagesMaths McqsafeeraPas encore d'évaluation

- Continuing Education CalendarDocument76 pagesContinuing Education CalendarBPas encore d'évaluation

- List of Investment Banks-UKDocument5 pagesList of Investment Banks-UKnnaemekenPas encore d'évaluation

- Narrative-Promotionalvideo - Englishmonth - HighschoolDocument2 pagesNarrative-Promotionalvideo - Englishmonth - HighschoolJaydel Dela RosaPas encore d'évaluation

- MMVA ZG537 Lean Manufacturing: Rajiv Gupta BITS Pilani Live Lecture 2Document32 pagesMMVA ZG537 Lean Manufacturing: Rajiv Gupta BITS Pilani Live Lecture 2arkraviPas encore d'évaluation

- Nature of Accounting Mind MapDocument12 pagesNature of Accounting Mind MapJared 03Pas encore d'évaluation

- ChaseDream Business School Guide INSEAD - ZH-CN - enDocument9 pagesChaseDream Business School Guide INSEAD - ZH-CN - enRafael LimaPas encore d'évaluation