Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Natural Law Legal PositivismDocument5 pagesNatural Law Legal PositivismlotuscasPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- ELECTION LAW Case Doctrines PDFDocument24 pagesELECTION LAW Case Doctrines PDFRio SanchezPas encore d'évaluation

- Othello Character Analysis and General NotesDocument8 pagesOthello Character Analysis and General Notesjoshuabonello50% (2)

- Iso 16750 4 2010 en PDFDocument8 pagesIso 16750 4 2010 en PDFvignesh100% (1)

- Training Design SKMTDocument4 pagesTraining Design SKMTKelvin Jay Cabreros Lapada67% (9)

- CRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesDocument110 pagesCRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesrockaholicnepsPas encore d'évaluation

- Caballes V CADocument2 pagesCaballes V CATintin CoPas encore d'évaluation

- City of Columbus Reaches Settlement Agreement With Plaintiffs in Alsaada v. ColumbusDocument2 pagesCity of Columbus Reaches Settlement Agreement With Plaintiffs in Alsaada v. ColumbusABC6/FOX28Pas encore d'évaluation

- Safety Data Sheet: Zetpol 1020Document8 pagesSafety Data Sheet: Zetpol 1020henrychtPas encore d'évaluation

- Botoys FormDocument3 pagesBotoys FormJurey Page Mondejar100% (1)

- Guidelines For The Writing of An M.Phil/Ph.D. ThesisDocument2 pagesGuidelines For The Writing of An M.Phil/Ph.D. ThesisMuneer MemonPas encore d'évaluation

- Tutang Sinampay:: Jerzon Senador Probably Wants To Be Famous and Show The World How Naughty He Is by Hanging HisDocument2 pagesTutang Sinampay:: Jerzon Senador Probably Wants To Be Famous and Show The World How Naughty He Is by Hanging HisClaire Anne BernardoPas encore d'évaluation

- Petitioners: La Bugal-B'Laan Tribal Association Inc, Rep. Chariman F'Long Miguel Lumayong Etc Respondent: Secretary Victor O. Ramos, DENR EtcDocument2 pagesPetitioners: La Bugal-B'Laan Tribal Association Inc, Rep. Chariman F'Long Miguel Lumayong Etc Respondent: Secretary Victor O. Ramos, DENR EtcApple Gee Libo-onPas encore d'évaluation

- A&M Plastics v. OPSol - ComplaintDocument35 pagesA&M Plastics v. OPSol - ComplaintSarah BursteinPas encore d'évaluation

- A Chronology of Key Events of US HistoryDocument5 pagesA Chronology of Key Events of US Historyanon_930849151Pas encore d'évaluation

- Itlp Question BankDocument4 pagesItlp Question BankHimanshu SethiPas encore d'évaluation

- CSRF 1 (CPF) FormDocument4 pagesCSRF 1 (CPF) FormJack Lee100% (1)

- TOR Custom Clearance in Ethiopia SCIDocument12 pagesTOR Custom Clearance in Ethiopia SCIDaniel GemechuPas encore d'évaluation

- COC 2021 - ROY - Finance OfficerDocument2 pagesCOC 2021 - ROY - Finance OfficerJillian V. RoyPas encore d'évaluation

- CEILLI Trial Ques EnglishDocument15 pagesCEILLI Trial Ques EnglishUSCPas encore d'évaluation

- The Following Information Is Available For Bott Company Additional Information ForDocument1 pageThe Following Information Is Available For Bott Company Additional Information ForTaimur TechnologistPas encore d'évaluation

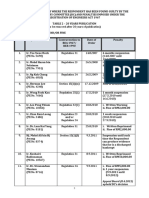

- LIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDocument1 pageLIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDarrenPas encore d'évaluation

- United States Bankruptcy Court Southern District of New YorkDocument21 pagesUnited States Bankruptcy Court Southern District of New YorkChapter 11 DocketsPas encore d'évaluation

- NC LiabilitiesDocument12 pagesNC LiabilitiesErin LumogdangPas encore d'évaluation

- Case StudyDocument6 pagesCase StudyGreen Tree0% (1)

- Bulletin No 18 August 16 2019 - PassDocument770 pagesBulletin No 18 August 16 2019 - PassNithyashree T100% (1)

- Test 3 - Part 5Document4 pagesTest 3 - Part 5hiếu võ100% (1)

- AKD Daily Mar 20 202sDocument3 pagesAKD Daily Mar 20 202sShujaat AhmadPas encore d'évaluation

- Riverscape Fact SheetDocument5 pagesRiverscape Fact SheetSharmaine FalcisPas encore d'évaluation

- CAGAYAN STATE UNIVERSITY TECHNOLOGY LIVELIHOOD EDUCATION CLUB CONSTITUTIONDocument7 pagesCAGAYAN STATE UNIVERSITY TECHNOLOGY LIVELIHOOD EDUCATION CLUB CONSTITUTIONjohnlloyd delarosaPas encore d'évaluation