Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Mkuchajr ProposalDocument9 pagesMkuchajr ProposalinnocentmkuchajrPas encore d'évaluation

- Kepco Ilijan CORPORATION, Petitioner, v. Commissioner of Internal REVENUE, RespondentDocument12 pagesKepco Ilijan CORPORATION, Petitioner, v. Commissioner of Internal REVENUE, RespondentnomercykillingPas encore d'évaluation

- Chapter 13Document61 pagesChapter 13ginish12Pas encore d'évaluation

- Forms BrgyDocument13 pagesForms BrgyErlinda LagunaPas encore d'évaluation

- How The Myth of The 'Robber Barons' Began-And Why It Persists - Foundation For EDocument11 pagesHow The Myth of The 'Robber Barons' Began-And Why It Persists - Foundation For ENinnin 64100% (1)

- Public Finance and Taxation Final12345Document134 pagesPublic Finance and Taxation Final12345ThomasGetye76% (29)

- E01 Word Smith Grant Writing BPlanDocument31 pagesE01 Word Smith Grant Writing BPlanBenPas encore d'évaluation

- Calculate New Salary Tax by Ather SaleemDocument2 pagesCalculate New Salary Tax by Ather SaleemMalikKamranAsifPas encore d'évaluation

- Intermediate Course Study Material: TaxationDocument34 pagesIntermediate Course Study Material: TaxationMd IbrarPas encore d'évaluation

- Ia3 Prelim Exam - Set ADocument11 pagesIa3 Prelim Exam - Set AClara MacallingPas encore d'évaluation

- Cost and Benefit Analysis BookDocument361 pagesCost and Benefit Analysis Book9315875729100% (7)

- 2643 Final Sample MCQDocument17 pages2643 Final Sample MCQDhivyaa ThayalanPas encore d'évaluation

- Passing The Plate - Smith and EmersonDocument283 pagesPassing The Plate - Smith and EmersonIsmael Mendez ReyesPas encore d'évaluation

- GSTDocument59 pagesGSTkeval Chavan88% (8)

- Nit75 PMC BhopalDocument64 pagesNit75 PMC BhopalFaisal KhanPas encore d'évaluation

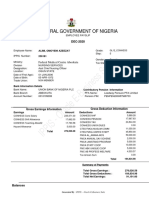

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- Sison Vs AnchetaDocument8 pagesSison Vs AnchetaJoshua Erik MadriaPas encore d'évaluation

- Form PDF 853296050300723-2023-24Document9 pagesForm PDF 853296050300723-2023-24muskanvivekfunhousePas encore d'évaluation

- Mcqs On Basic Concept of Income Tax, Residential Status & Exempt IncomeDocument6 pagesMcqs On Basic Concept of Income Tax, Residential Status & Exempt IncomePradeep SethyPas encore d'évaluation

- FM8 Lec 1 Principles That Form FinanceDocument3 pagesFM8 Lec 1 Principles That Form FinanceDarryl RazalanPas encore d'évaluation

- MIECO 5001 Financial Report PDFDocument130 pagesMIECO 5001 Financial Report PDFkoneiseongPas encore d'évaluation

- Sources of Data (2) Purposes of Financial Analysis (For Making Decisions) How To Analyze Financial DataDocument5 pagesSources of Data (2) Purposes of Financial Analysis (For Making Decisions) How To Analyze Financial DataĐinh AnhPas encore d'évaluation

- Tax Saving Investment Strategies Among Salaried Individuals in Aurangabad CityDocument6 pagesTax Saving Investment Strategies Among Salaried Individuals in Aurangabad CityRajani AthanimathPas encore d'évaluation

- Begun and Held in Metro Manila, On Monday, The Twenty-Sixth Day of July, Nineteen Hundred and Ninety-ThreeDocument6 pagesBegun and Held in Metro Manila, On Monday, The Twenty-Sixth Day of July, Nineteen Hundred and Ninety-ThreeJILL ANGELESPas encore d'évaluation

- Cost Records and Cost Audit Under Companies Act, 2013Document6 pagesCost Records and Cost Audit Under Companies Act, 2013Purushotham MysorePas encore d'évaluation

- Tax Law Case DigestsDocument131 pagesTax Law Case DigestsThea Jane MerinPas encore d'évaluation

- Vishvanath Enterprise Bill dt08032022Document1 pageVishvanath Enterprise Bill dt08032022rahulPas encore d'évaluation

- 99 BillDocument2 pages99 BillLive lifePas encore d'évaluation

- Savani - A Choice Mind-Set Increases The Acceptance and Maintenance of Wealth InequalityDocument10 pagesSavani - A Choice Mind-Set Increases The Acceptance and Maintenance of Wealth Inequalityselena pPas encore d'évaluation