Vous aimerez peut-être aussi

- Renewable Energy Finance: Theory and PracticeD'EverandRenewable Energy Finance: Theory and PracticeÉvaluation : 4 sur 5 étoiles4/5 (1)

- IC38 Janamghutti v1 10052019 PDFDocument67 pagesIC38 Janamghutti v1 10052019 PDFMahesh S Gour75% (4)

- Federal Reserve Lien Ammended AgainDocument3 pagesFederal Reserve Lien Ammended AgainCharles Scott0% (1)

- Equity Markets in Transition PDFDocument612 pagesEquity Markets in Transition PDFkshitij kumar100% (1)

- Microfinance and Poverty: Evidence Using Panel Data From BangladeshDocument25 pagesMicrofinance and Poverty: Evidence Using Panel Data From BangladeshMvelako StoryPas encore d'évaluation

- Microfinance and Poverty Evidence Using Panel Data From BangladeshDocument25 pagesMicrofinance and Poverty Evidence Using Panel Data From BangladeshCharles PeterPas encore d'évaluation

- Energy in Common - GSBI 2010 - FactsheetDocument2 pagesEnergy in Common - GSBI 2010 - FactsheetseincstsPas encore d'évaluation

- Crowdfunding - The Road To Energy Decentralization and Energy-Poverty Eradication - TK FredericaDocument6 pagesCrowdfunding - The Road To Energy Decentralization and Energy-Poverty Eradication - TK FredericaTirza Kasamira FredericaPas encore d'évaluation

- Access To Energy Via Digital Finance: Overview of Models and Prospects For InnovationDocument29 pagesAccess To Energy Via Digital Finance: Overview of Models and Prospects For InnovationCGAP PublicationsPas encore d'évaluation

- Impact of Microcredit in Rural Areas of Morocco: Evidence From A Randomized EvaluationDocument33 pagesImpact of Microcredit in Rural Areas of Morocco: Evidence From A Randomized EvaluationSedekholie ChadiPas encore d'évaluation

- Solar Power Concept PaperDocument7 pagesSolar Power Concept Paperrasnowmah2012Pas encore d'évaluation

- "Microfinance in India An Indepth Study": Project Proposal TitledDocument7 pages"Microfinance in India An Indepth Study": Project Proposal TitledAnkush AgrawalPas encore d'évaluation

- Deconstructing The Concept FINAL Pre Print Accepted in WIREDocument26 pagesDeconstructing The Concept FINAL Pre Print Accepted in WIREHay Day RPas encore d'évaluation

- Renewable Energy Power Projects For Rural Electrification in India PDFDocument86 pagesRenewable Energy Power Projects For Rural Electrification in India PDFSD FGPas encore d'évaluation

- Kuliah BMT 31 535-542 - SalinDocument8 pagesKuliah BMT 31 535-542 - SalinDokterndeso ChannelPas encore d'évaluation

- Current Affairs 2010 WWW - UpscportalDocument141 pagesCurrent Affairs 2010 WWW - UpscportalMayoof MajidPas encore d'évaluation

- Public Sector Funding and Debt Management: A Case For GDP-Linked SukukDocument29 pagesPublic Sector Funding and Debt Management: A Case For GDP-Linked SukukFoutiyou OumarPas encore d'évaluation

- Does Microfinance Reduce Poverty in Bangladesh? New Evidence From Household Panel DataDocument22 pagesDoes Microfinance Reduce Poverty in Bangladesh? New Evidence From Household Panel Datamaria ianPas encore d'évaluation

- "Causes of Disagreement in Electricity Generation Among Stakeholders in Sub-Saharan Africa" by Mekobe AjebeDocument20 pages"Causes of Disagreement in Electricity Generation Among Stakeholders in Sub-Saharan Africa" by Mekobe AjebeThe International Research Center for Energy and Economic Development (ICEED)Pas encore d'évaluation

- Dissertation Topics On MicrofinanceDocument5 pagesDissertation Topics On MicrofinanceApaPapersForSaleFargo100% (1)

- The Performance of Microfinance Institutions in Cameroon: Does Financial Regulation Really Matter?Document13 pagesThe Performance of Microfinance Institutions in Cameroon: Does Financial Regulation Really Matter?Ayoniseh CarolPas encore d'évaluation

- WEF Future of Electricity 2016Document36 pagesWEF Future of Electricity 2016leemhyunseokPas encore d'évaluation

- Clean Energy Services For All: Financing Universal ElectrificationDocument14 pagesClean Energy Services For All: Financing Universal ElectrificationDetlef LoyPas encore d'évaluation

- Scaling Up Access To Electricity: The Case of BangladeshDocument12 pagesScaling Up Access To Electricity: The Case of BangladeshDetlef LoyPas encore d'évaluation

- Edited 2Document23 pagesEdited 2Mahesh majji100% (1)

- Technology and Development: A Growing Number of Initiatives Are Promoting Bottom-Up Ways To Deliver Energy To The World's PoorDocument9 pagesTechnology and Development: A Growing Number of Initiatives Are Promoting Bottom-Up Ways To Deliver Energy To The World's PoorJeremiah SmithPas encore d'évaluation

- Telling Our Story: Climate ChangeDocument24 pagesTelling Our Story: Climate ChangeInternational Finance Corporation (IFC)Pas encore d'évaluation

- Enea Ensuring Steady Cash Flows in Off Grid Solar Microgrid ProjectsundefinedDocument49 pagesEnea Ensuring Steady Cash Flows in Off Grid Solar Microgrid Projectsundefinedhanae lakhdarPas encore d'évaluation

- Case Study by ONERGYDocument5 pagesCase Study by ONERGYakhileshguptamnrePas encore d'évaluation

- Impact of Islamic Microfinance On Borrower S Income in Pakistan-A Case Study of AkhuwatDocument10 pagesImpact of Islamic Microfinance On Borrower S Income in Pakistan-A Case Study of AkhuwatmairaPas encore d'évaluation

- Business Models For Solar-Powered Irrigation in EthiopiaDocument8 pagesBusiness Models For Solar-Powered Irrigation in EthiopiaBasazinew A BasazinewPas encore d'évaluation

- Micro Finance: Microfinance Is The Provision ofDocument7 pagesMicro Finance: Microfinance Is The Provision ofSushant ShettyPas encore d'évaluation

- Thesis On Microfinance in IndiaDocument5 pagesThesis On Microfinance in IndiaOnlinePaperWritersUK100% (2)

- Msci Research PaperDocument7 pagesMsci Research Paperfvf442bf100% (1)

- Effect of Micro-Finance On PovertyDocument18 pagesEffect of Micro-Finance On PovertyKarim KhaledPas encore d'évaluation

- Sustainability 11Document13 pagesSustainability 11colegiulPas encore d'évaluation

- World Bank Solar Home Systems Projects: Experiences and Lessons Learned 1993-2000Document8 pagesWorld Bank Solar Home Systems Projects: Experiences and Lessons Learned 1993-2000Pranay ShrivastavaPas encore d'évaluation

- Microfinance-Thesis Dilin LimDocument37 pagesMicrofinance-Thesis Dilin Lim9415351296Pas encore d'évaluation

- Renewable 0 Energy 0 ReportDocument94 pagesRenewable 0 Energy 0 ReportTara Sinha100% (1)

- AslamDocument32 pagesAslamAminurPas encore d'évaluation

- Green Finance in Bangladesh - Policies, Institutions, and Challenges - Adbi-Wp892Document28 pagesGreen Finance in Bangladesh - Policies, Institutions, and Challenges - Adbi-Wp892shakib nazmusPas encore d'évaluation

- Cover StoryDocument8 pagesCover StoryBhavesh SwamiPas encore d'évaluation

- Financing Renewable Energy in India: A Review of Mechanisms in Wind and Solar ApplicationsDocument16 pagesFinancing Renewable Energy in India: A Review of Mechanisms in Wind and Solar ApplicationsPrudhvinadh KopparapuPas encore d'évaluation

- Literature Review On Power Sector ReformsDocument7 pagesLiterature Review On Power Sector Reformsgrgdazukg100% (1)

- Microfinance: in Partial Fulfillment of The Requirements For The Degree ofDocument11 pagesMicrofinance: in Partial Fulfillment of The Requirements For The Degree ofpromilagoyalPas encore d'évaluation

- Literature Review MicrofinanceDocument5 pagesLiterature Review Microfinancedajemevefaz2100% (1)

- Business Plan: Kudakwashe Solomon Mavuru Paul Henri Hie Nathan KuchenaDocument24 pagesBusiness Plan: Kudakwashe Solomon Mavuru Paul Henri Hie Nathan Kuchenakudakwashe4mavuruPas encore d'évaluation

- Chapter-01: Introduction: (John D. Finnerty, 1996)Document55 pagesChapter-01: Introduction: (John D. Finnerty, 1996)aziz ghediraPas encore d'évaluation

- Public Sector Funding and Debt Management: A Case For GDP-Linked SukukDocument28 pagesPublic Sector Funding and Debt Management: A Case For GDP-Linked SukukSon Go HanPas encore d'évaluation

- Bangladesh Microfinance Full CaseDocument19 pagesBangladesh Microfinance Full CaseMushfiq Farazi AbhikPas encore d'évaluation

- Fostering Livelihoods with Decentralised Renewable Energy: An Ecosystems ApproachD'EverandFostering Livelihoods with Decentralised Renewable Energy: An Ecosystems ApproachPas encore d'évaluation

- Renewable Energy: Thematic BriefsDocument3 pagesRenewable Energy: Thematic BriefsFelixPas encore d'évaluation

- Journal - Impact of Microcredit Inrural Areas of Morocco. Evidence From A Randomized EvaluationDocument31 pagesJournal - Impact of Microcredit Inrural Areas of Morocco. Evidence From A Randomized EvaluationAgustina EkaPas encore d'évaluation

- OECD WWF Asia Sustainable Finance Initiative Case StudyDocument27 pagesOECD WWF Asia Sustainable Finance Initiative Case Studypradipto.bhaskoroPas encore d'évaluation

- Malaysia ExperienceDocument5 pagesMalaysia ExperienceMohd Raffi SamsudinPas encore d'évaluation

- Literature Review On Microfinance Institutions in UgandaDocument9 pagesLiterature Review On Microfinance Institutions in UgandakbcymacndPas encore d'évaluation

- Financing Clean Energy in Developing Asia—Volume 2D'EverandFinancing Clean Energy in Developing Asia—Volume 2Pas encore d'évaluation

- Distributed Generation Technologies: An Approach Towards Future EnergyDocument7 pagesDistributed Generation Technologies: An Approach Towards Future EnergyPavan KhetrapalPas encore d'évaluation

- Determinants of Financial Performance of Microfinance Institutions in Kenya: A Case of Microfinance Institutions in Nakuru TownDocument16 pagesDeterminants of Financial Performance of Microfinance Institutions in Kenya: A Case of Microfinance Institutions in Nakuru TownTJPRC PublicationsPas encore d'évaluation

- Renewable energy finance: Sovereign guaranteesD'EverandRenewable energy finance: Sovereign guaranteesPas encore d'évaluation

- A Guide for Developing Zero Energy Communities: The Zec GuideD'EverandA Guide for Developing Zero Energy Communities: The Zec GuidePas encore d'évaluation

- Renewable energy finance: Institutional capitalD'EverandRenewable energy finance: Institutional capitalÉvaluation : 5 sur 5 étoiles5/5 (1)

- Improving Skills for the Electricity Sector in IndonesiaD'EverandImproving Skills for the Electricity Sector in IndonesiaPas encore d'évaluation

- Cash Receipts Record (Crrec) : InstructionsDocument1 pageCash Receipts Record (Crrec) : InstructionsdinvPas encore d'évaluation

- BSP M-2020-016 PDFDocument9 pagesBSP M-2020-016 PDFRaine Buenaventura-EleazarPas encore d'évaluation

- Prop Firm Drawdown Limitations - Forex Prop ReviewsDocument9 pagesProp Firm Drawdown Limitations - Forex Prop ReviewsMye RakPas encore d'évaluation

- My Cash: Balance TotalDocument9 pagesMy Cash: Balance TotalDahlan MuksinPas encore d'évaluation

- Varengold Bank FX Trading-Challenge - Prize 1,000,000 USDDocument1 pageVarengold Bank FX Trading-Challenge - Prize 1,000,000 USDKostas KazakosPas encore d'évaluation

- UntitledDocument2 pagesUntitledarmando González100% (2)

- Cfas Millan 2020 Answer KeyDocument193 pagesCfas Millan 2020 Answer KeyPEBIDA, DAVERLY N.Pas encore d'évaluation

- APT ExerciseDocument3 pagesAPT Exercise노긔0% (1)

- Pioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesDocument4 pagesPioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesPrajwal PaiPas encore d'évaluation

- W1 Partnership AccountingDocument11 pagesW1 Partnership AccountingChristine Joy MondaPas encore d'évaluation

- Accounting Intern Cover Letter ExamplesDocument7 pagesAccounting Intern Cover Letter Examplesiyldyzadf100% (2)

- IJIBM Vol9No4 Nov2017Document310 pagesIJIBM Vol9No4 Nov2017فوزان علیPas encore d'évaluation

- A B C D: 02 Objective / Objektif 2Document5 pagesA B C D: 02 Objective / Objektif 2foryourhonour wongPas encore d'évaluation

- Your 2024 Social Security Cost of Living IncreaseDocument4 pagesYour 2024 Social Security Cost of Living IncreasenazoyaqPas encore d'évaluation

- Underwriting: Types of Underwriting (1) FirmunderwritingDocument8 pagesUnderwriting: Types of Underwriting (1) FirmunderwritingThakker NimeshPas encore d'évaluation

- 4.3.2.5 Elaborate - Determining AdjustmentsDocument4 pages4.3.2.5 Elaborate - Determining AdjustmentsMa Fe Tabasa0% (1)

- Sawsan Hassan Al SaffarDocument3 pagesSawsan Hassan Al SaffarwaminoPas encore d'évaluation

- REAL ESTATE MORTGAGE-CalubayanDocument5 pagesREAL ESTATE MORTGAGE-CalubayanChristopher JuniarPas encore d'évaluation

- Far - First Preboard QuestionnaireDocument14 pagesFar - First Preboard QuestionnairewithyouidkPas encore d'évaluation

- Unit II Methods of Valuing Material IssuesDocument21 pagesUnit II Methods of Valuing Material IssuesLeemaRosaline Simon0% (1)

- ForexManagement Paresh Shah WileyIndiaDocument4 pagesForexManagement Paresh Shah WileyIndiaArnoldPas encore d'évaluation

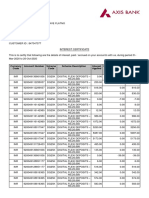

- Interest CertificateDocument2 pagesInterest CertificatesumitPas encore d'évaluation

- Financial Planning and ForecastingDocument20 pagesFinancial Planning and ForecastingSyedMaazPas encore d'évaluation

- Eng. Book PDFDocument93 pagesEng. Book PDFSelvaraj VillyPas encore d'évaluation

- Ayush Gaur First Internship Project ReportDocument43 pagesAyush Gaur First Internship Project Report777 FamPas encore d'évaluation

- Smart Cities As Business HubsDocument11 pagesSmart Cities As Business HubsSabyasachi Naik (Zico)Pas encore d'évaluation

- Credit Report ExplanationDocument3 pagesCredit Report ExplanationthalhaPas encore d'évaluation