Vous aimerez peut-être aussi

- Private Client Practice: An Expert Guide, 2nd editionD'EverandPrivate Client Practice: An Expert Guide, 2nd editionPas encore d'évaluation

- Directors DutiesDocument134 pagesDirectors DutiesMatthew Evan ThomasPas encore d'évaluation

- Company Law Modernisation and Corporate GovernanceDocument20 pagesCompany Law Modernisation and Corporate GovernanceMagda ShavadzePas encore d'évaluation

- The First Basic Plan For Immigration Policy, 2008-2012, Ministry of Justice, Republic of KoreaDocument129 pagesThe First Basic Plan For Immigration Policy, 2008-2012, Ministry of Justice, Republic of KoreakhulawPas encore d'évaluation

- T1 General PDFDocument4 pagesT1 General PDFbatmanbittuPas encore d'évaluation

- Corporate Governance: A practical guide for accountantsD'EverandCorporate Governance: A practical guide for accountantsÉvaluation : 5 sur 5 étoiles5/5 (1)

- Final Draft of The Role of IRP Under IBC CodeDocument24 pagesFinal Draft of The Role of IRP Under IBC CodeHemantPrajapatiPas encore d'évaluation

- Chapter - Money Creation & Framwork of Monetary Policy1Document6 pagesChapter - Money Creation & Framwork of Monetary Policy1Nahidul Islam IUPas encore d'évaluation

- Skills For Smart Industrial Specialization and Digital TransformationDocument342 pagesSkills For Smart Industrial Specialization and Digital TransformationAndrei ItemPas encore d'évaluation

- SWOT-ToWS Analysis of LenovoDocument2 pagesSWOT-ToWS Analysis of Lenovoada9ablao100% (4)

- Extremely Entertaining Short Stories PDFDocument27 pagesExtremely Entertaining Short Stories PDFvidovdan9852Pas encore d'évaluation

- Cross-Border Insolvency Problems - Is The UNCITRAL Model Law The Answer PDFDocument27 pagesCross-Border Insolvency Problems - Is The UNCITRAL Model Law The Answer PDFvidovdan9852Pas encore d'évaluation

- Chapter One ProjectDocument11 pagesChapter One ProjectDickson Tk Chuma Jr.Pas encore d'évaluation

- INTRODUCTIONDocument11 pagesINTRODUCTIONBhumika KhandelwalPas encore d'évaluation

- The UK's Company Law ReviewDocument6 pagesThe UK's Company Law ReviewSabeeb M RazeenPas encore d'évaluation

- Corporate Governance Reform and Corporate Failure in The UKDocument15 pagesCorporate Governance Reform and Corporate Failure in The UKGolam KibriaPas encore d'évaluation

- Control and Corporate Rescue - An Anglo-American Evaluation - Gerard McCormack (2007) (Pp. 517 y SS.)Document38 pagesControl and Corporate Rescue - An Anglo-American Evaluation - Gerard McCormack (2007) (Pp. 517 y SS.)Vicente Javier Tapia InfantePas encore d'évaluation

- Part 1Document108 pagesPart 1Thirnugnanasampandar ArulananthasivamPas encore d'évaluation

- Corporate Governance in The CaribbeanDocument46 pagesCorporate Governance in The CaribbeanJamal ShamsudeenPas encore d'évaluation

- Benefits of Ai in Corporate GovernanceDocument14 pagesBenefits of Ai in Corporate GovernanceAyushman SinghPas encore d'évaluation

- A Report On Business Law and EthicsDocument19 pagesA Report On Business Law and Ethicssharaf fahimPas encore d'évaluation

- Corporate Governance of Unilever and MicDocument22 pagesCorporate Governance of Unilever and MicAnushk ShuklaPas encore d'évaluation

- Bankruptcy and ReorganizationDocument13 pagesBankruptcy and ReorganizationAnkita ChauhanPas encore d'évaluation

- Corporate Insolvency Resolution Procedure Under Indian Insolvency and Bankruptcy Code, 2016: A Comparative PerspectiveDocument8 pagesCorporate Insolvency Resolution Procedure Under Indian Insolvency and Bankruptcy Code, 2016: A Comparative PerspectiveDeva SharmaPas encore d'évaluation

- SubmissionDocument8 pagesSubmissionAnonymous F9E2kpF5LePas encore d'évaluation

- Article - Prerna Tomar - CompressedDocument16 pagesArticle - Prerna Tomar - CompressedprernaPas encore d'évaluation

- Corporate Reorganization and Strategic Behaviour - An Economic AnaDocument38 pagesCorporate Reorganization and Strategic Behaviour - An Economic AnaAmanuel BirhanPas encore d'évaluation

- Insolvency and Bankruptcy Code 2016Document2 pagesInsolvency and Bankruptcy Code 2016Sweta AgrawalPas encore d'évaluation

- The Growth in Corporate Governance CodesDocument15 pagesThe Growth in Corporate Governance CodesSudip BaruaPas encore d'évaluation

- U-4 Insolvency and Bankruptcy Code 2016Document26 pagesU-4 Insolvency and Bankruptcy Code 2016HIMANI PALAKSHAPas encore d'évaluation

- Corporate LawDocument35 pagesCorporate Lawnicrome buringPas encore d'évaluation

- Reforming Capital Maintenance Law: The Companies (Amendment) Act 2005Document43 pagesReforming Capital Maintenance Law: The Companies (Amendment) Act 2005yohannis asfachewPas encore d'évaluation

- Acra Legal DigestDocument15 pagesAcra Legal DigestAudrey ArdanentyaPas encore d'évaluation

- Shasi, Urvashi and Kumar, Tushar - Changing Paradigm of Insolvency Jurisprudence Without CommentsDocument9 pagesShasi, Urvashi and Kumar, Tushar - Changing Paradigm of Insolvency Jurisprudence Without CommentsTushar KumarPas encore d'évaluation

- Law of Business Associations GPR 304 Director DutiesDocument15 pagesLaw of Business Associations GPR 304 Director Dutiesnkita MaryPas encore d'évaluation

- File146909 KDocument62 pagesFile146909 KMask ManPas encore d'évaluation

- Reverse PiercingDocument18 pagesReverse PiercingDhirenPas encore d'évaluation

- Understanding Insolvency: October 2008Document49 pagesUnderstanding Insolvency: October 2008Shakti SinghPas encore d'évaluation

- Financial Distress, Reorganization, and Organizational EfficiencyDocument26 pagesFinancial Distress, Reorganization, and Organizational EfficiencyFadil YmPas encore d'évaluation

- Caa 18Document14 pagesCaa 18Salman AsimPas encore d'évaluation

- Merger and Acquisition Project ReportDocument59 pagesMerger and Acquisition Project ReportSatish ChavanPas encore d'évaluation

- Tentative ChapterisationDocument13 pagesTentative ChapterisationNikhil kumarPas encore d'évaluation

- Global Restructuring Insolvency Guide 12 2016new Logo ItalyDocument28 pagesGlobal Restructuring Insolvency Guide 12 2016new Logo ItalyaltieroloPas encore d'évaluation

- 001 Grant Thornton Corporate Governance Review 2011Document60 pages001 Grant Thornton Corporate Governance Review 2011Ali LoughreyPas encore d'évaluation

- Dissertation Covid-19Document41 pagesDissertation Covid-19BAFE 20-05 Rimsha ZaffarPas encore d'évaluation

- Article 4Document31 pagesArticle 4Abdul OGPas encore d'évaluation

- UK Approach To Corporate Governance Oct 20101Document16 pagesUK Approach To Corporate Governance Oct 20101Alice PhamPas encore d'évaluation

- Dwnload Full Auditing Assurance A Business Risk Approach 3rd Edition Jubb Solutions Manual PDFDocument35 pagesDwnload Full Auditing Assurance A Business Risk Approach 3rd Edition Jubb Solutions Manual PDFbendvvduncan100% (16)

- Bankruptcy Is A Determination of Insolvency Made by A Court of Law With Resulting Legal Orders Intended To Resolve The InsolvencyDocument9 pagesBankruptcy Is A Determination of Insolvency Made by A Court of Law With Resulting Legal Orders Intended To Resolve The InsolvencyHarsha VardhanPas encore d'évaluation

- Corporate Governance1Document17 pagesCorporate Governance1Deshan1989Pas encore d'évaluation

- Are Laws Needed For Public ManagemenDocument25 pagesAre Laws Needed For Public ManagemenYard AssociatesPas encore d'évaluation

- Comparative Corporate InsolvencyDocument30 pagesComparative Corporate InsolvencyChuyi WeiPas encore d'évaluation

- The Cadbury Report 1992: Shared Vision and Beyond: Related PapersDocument43 pagesThe Cadbury Report 1992: Shared Vision and Beyond: Related Paperstinashe chavundukatPas encore d'évaluation

- Corporate Restructuring by Dr. Fancy TooDocument26 pagesCorporate Restructuring by Dr. Fancy TooDavid MunyuaPas encore d'évaluation

- Chap 012Document20 pagesChap 012Hemali MehtaPas encore d'évaluation

- Selective Strategy RestructuringDocument30 pagesSelective Strategy RestructuringMikha DetalimPas encore d'évaluation

- CH 13 - Current LiabilitiesDocument85 pagesCH 13 - Current LiabilitiesViviane Tavares60% (5)

- SOXDocument15 pagesSOXRafael BazaniPas encore d'évaluation

- 2011 Giovanni Fasano Corporate Governance h17Document151 pages2011 Giovanni Fasano Corporate Governance h17MoatasemMadianPas encore d'évaluation

- ComparativeDocument19 pagesComparativetemivaughnPas encore d'évaluation

- Research Paper 4Document16 pagesResearch Paper 4Akshayveer Singh SehrawatPas encore d'évaluation

- Comparitive Analysis of Insolvency and Bankruptcy Laws in India, US and Germany.Document7 pagesComparitive Analysis of Insolvency and Bankruptcy Laws in India, US and Germany.Prasanna KumarPas encore d'évaluation

- MSME IBC2 FootDocument26 pagesMSME IBC2 FootPriyadarshan NairPas encore d'évaluation

- Enterprise Act 2002 Guidance MergerDocument13 pagesEnterprise Act 2002 Guidance MergerdakappakvPas encore d'évaluation

- Corporate GovernanceDocument2 pagesCorporate GovernanceMehedi Hasan ShaikotPas encore d'évaluation

- Pre-Packaged Insolvency Framework - A Boon or Bane For IndiaDocument8 pagesPre-Packaged Insolvency Framework - A Boon or Bane For IndiaBhai Ki Vines (Shivansh Gupta)Pas encore d'évaluation

- AC301 Off Balance Sheet FinancingDocument25 pagesAC301 Off Balance Sheet Financinghui7411Pas encore d'évaluation

- Declassified UK Paper On Srebrenica - PREM-19-5487 - 1Document110 pagesDeclassified UK Paper On Srebrenica - PREM-19-5487 - 1vidovdan9852Pas encore d'évaluation

- Benign Congenital HypotoniaDocument4 pagesBenign Congenital Hypotoniavidovdan9852Pas encore d'évaluation

- Floppy Infant SyndromeDocument5 pagesFloppy Infant Syndromevidovdan9852Pas encore d'évaluation

- JFK50 ShortlinksDocument7 pagesJFK50 Shortlinksvidovdan9852Pas encore d'évaluation

- Russia vs. Ukraine Eurobond - Final Judgment - Judgement 29.03.2017Document107 pagesRussia vs. Ukraine Eurobond - Final Judgment - Judgement 29.03.2017vidovdan9852100% (1)

- 275 Export DeclarationDocument3 pages275 Export Declarationvidovdan9852Pas encore d'évaluation

- Declassified UK Files On Srebrenica - PREM-19-5487 - 2Document100 pagesDeclassified UK Files On Srebrenica - PREM-19-5487 - 2vidovdan9852Pas encore d'évaluation

- Article IV Montenego 2017Document92 pagesArticle IV Montenego 2017vidovdan9852Pas encore d'évaluation

- Global Dollar Credit and Carry Trades - A Firm-Level AnalysisDocument53 pagesGlobal Dollar Credit and Carry Trades - A Firm-Level Analysisvidovdan9852Pas encore d'évaluation

- Floppy Infant SyndromeDocument5 pagesFloppy Infant Syndromevidovdan9852Pas encore d'évaluation

- List of 616 English Irregular VerbsDocument21 pagesList of 616 English Irregular Verbsمحمد طه المقطري67% (3)

- A Unified Model of Early Word Learning - Integrating Statistical and Social CuesDocument8 pagesA Unified Model of Early Word Learning - Integrating Statistical and Social Cuesvidovdan9852Pas encore d'évaluation

- How Children Learn WordsDocument6 pagesHow Children Learn Wordsvidovdan9852Pas encore d'évaluation

- A Determination of The Risk of Ruin PDFDocument36 pagesA Determination of The Risk of Ruin PDFvidovdan9852Pas encore d'évaluation

- Example Mutual Non Disclosure AgreementDocument2 pagesExample Mutual Non Disclosure Agreementvidovdan9852Pas encore d'évaluation

- A Convenient Untruth - Fact and Fantasy in The Doctrine of Odious DebtsDocument45 pagesA Convenient Untruth - Fact and Fantasy in The Doctrine of Odious Debtsvidovdan9852Pas encore d'évaluation

- Chapter 11 at TwilightDocument30 pagesChapter 11 at Twilightvidovdan9852Pas encore d'évaluation

- Artigo Previsão de Falência Com Lógica Fuzzy Bancos TurcosDocument13 pagesArtigo Previsão de Falência Com Lógica Fuzzy Bancos TurcosAndrew Drummond-MurrayPas encore d'évaluation

- Balancing The Public Interest - Applying The Public Interest Test To Exemption in The UK Freedom of Information Act 2000Document62 pagesBalancing The Public Interest - Applying The Public Interest Test To Exemption in The UK Freedom of Information Act 2000vidovdan9852Pas encore d'évaluation

- Hanlon Illegitimate DebtDocument16 pagesHanlon Illegitimate DebtVinícius RitterPas encore d'évaluation

- From Privilege To Right - Limited LiabilityDocument22 pagesFrom Privilege To Right - Limited Liabilitymarcelo4lauarPas encore d'évaluation

- A Reply To Alan Schwartz's 'A Contract Theory Approach To Business Bankruptcy' PDFDocument26 pagesA Reply To Alan Schwartz's 'A Contract Theory Approach To Business Bankruptcy' PDFvidovdan9852Pas encore d'évaluation

- After The Housing Crisis - Second Liens and Contractual InefficienciesDocument21 pagesAfter The Housing Crisis - Second Liens and Contractual Inefficienciesvidovdan9852Pas encore d'évaluation

- Too Many To Fail - The Effect of Regulatory Forbearance On Market DisciplineDocument38 pagesToo Many To Fail - The Effect of Regulatory Forbearance On Market Disciplinevidovdan9852Pas encore d'évaluation

- A Convenient Untruth - Fact and Fantasy in The Doctrine of Odious DebtsDocument45 pagesA Convenient Untruth - Fact and Fantasy in The Doctrine of Odious Debtsvidovdan9852Pas encore d'évaluation

- Leases and InsolvencyDocument32 pagesLeases and Insolvencyvidovdan9852Pas encore d'évaluation

- Assessing The Probability of BankruptcyDocument47 pagesAssessing The Probability of Bankruptcyvidovdan9852Pas encore d'évaluation

- (ISDA, Altman) Analyzing and Explaining Default Recovery RatesDocument97 pages(ISDA, Altman) Analyzing and Explaining Default Recovery Rates00aaPas encore d'évaluation

- L03 ECO220 PrintDocument15 pagesL03 ECO220 PrintAli SioPas encore d'évaluation

- Air Asia CompleteDocument18 pagesAir Asia CompleteAmy CharmainePas encore d'évaluation

- Seminar Topic: Fill All ContentDocument7 pagesSeminar Topic: Fill All ContentRanjith GowdaPas encore d'évaluation

- Rise of Hitler Inquiry Sources-3CDocument15 pagesRise of Hitler Inquiry Sources-3CClaudia ChangPas encore d'évaluation

- Project Feasibility Report: BBA 5th SemesterDocument15 pagesProject Feasibility Report: BBA 5th SemesterChandan RaiPas encore d'évaluation

- Social Integration Approaches and Issues, UNRISD Publication (1994)Document16 pagesSocial Integration Approaches and Issues, UNRISD Publication (1994)United Nations Research Institute for Social DevelopmentPas encore d'évaluation

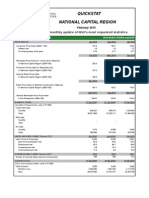

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocument3 pagesQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiPas encore d'évaluation

- VAT Registration CertificateDocument1 pageVAT Registration Certificatelucas.saleixo88Pas encore d'évaluation

- Pay Slip For The Month of April 2018Document1 pagePay Slip For The Month of April 2018srini reddyPas encore d'évaluation

- Account Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRajwinder SandhuPas encore d'évaluation

- ESSAY01 - Advantages and Disadvantages of GlobalizationDocument5 pagesESSAY01 - Advantages and Disadvantages of GlobalizationJelo ArtozaPas encore d'évaluation

- Complete Data About Swiss Grid PDFDocument7 pagesComplete Data About Swiss Grid PDFManpreet SinghPas encore d'évaluation

- Strategic Plan DRAFTVolunteerDocument85 pagesStrategic Plan DRAFTVolunteerLourdes SusaetaPas encore d'évaluation

- Sabc Directory2014-2015Document48 pagesSabc Directory2014-2015api-307927988Pas encore d'évaluation

- Tugas Problem Set 5 Ekonomi ManajerialDocument3 pagesTugas Problem Set 5 Ekonomi ManajerialRuth AdrianaPas encore d'évaluation

- Amma Mobile InsuranceDocument1 pageAmma Mobile InsuranceANANTH JPas encore d'évaluation

- DTH IndustryDocument37 pagesDTH IndustrySudip Vyas100% (1)

- OD126193179886369000Document6 pagesOD126193179886369000Refill positivityPas encore d'évaluation

- Raki RakiDocument63 pagesRaki RakiRAJA SHEKHARPas encore d'évaluation

- Methods To Initiate Ventures: Leoncio, Ma. Aira Grabrielle R. Mamigo, Princess Nicole B. G12-AB126Document21 pagesMethods To Initiate Ventures: Leoncio, Ma. Aira Grabrielle R. Mamigo, Princess Nicole B. G12-AB126Precious MamigoPas encore d'évaluation

- AbstractDocument12 pagesAbstractanmolPas encore d'évaluation

- Daftar Industrial EstatesDocument2 pagesDaftar Industrial EstatesKepo DehPas encore d'évaluation

- Plan Contable EmpresarialDocument432 pagesPlan Contable EmpresarialJhamil Nirek PascasioPas encore d'évaluation

- Spot THE Error: Detai L Ed Expl Anati OnDocument131 pagesSpot THE Error: Detai L Ed Expl Anati OnopprakasPas encore d'évaluation

- Malabon AIP 2014+amendments PDFDocument81 pagesMalabon AIP 2014+amendments PDFCorics HerbuelaPas encore d'évaluation