Vous aimerez peut-être aussi

- Gas Aggregation Company of Nigeria Investor Forum PresentationDocument23 pagesGas Aggregation Company of Nigeria Investor Forum PresentationsegunoyesPas encore d'évaluation

- Domestic GasDocument2 pagesDomestic GasOdiri OginniPas encore d'évaluation

- 2014.05.22. Interventions Required For The Development of The Gas Sector in NigeriaDocument21 pages2014.05.22. Interventions Required For The Development of The Gas Sector in NigeriasiriuslotPas encore d'évaluation

- Nigerian Gas OverviewDocument15 pagesNigerian Gas OverviewKagiso KayaPas encore d'évaluation

- Terms & Conditions of Tariff A ComparisonDocument42 pagesTerms & Conditions of Tariff A ComparisonVineel KambalaPas encore d'évaluation

- Winners Power Gardens Refinery BPLANDocument18 pagesWinners Power Gardens Refinery BPLANOwunari Adaye-OrugbaniPas encore d'évaluation

- NNPCDocument21 pagesNNPCtsar_philip2010100% (1)

- 1354 Nigeria Country SuDocument48 pages1354 Nigeria Country Sudharmendra_kanthariaPas encore d'évaluation

- Bond Calculator TemplateDocument2 pagesBond Calculator Templatechintandesai20083112Pas encore d'évaluation

- Economic Evaluation and Sensitivity Analysis of Some Fuel Oil Upgrading ProcessesDocument11 pagesEconomic Evaluation and Sensitivity Analysis of Some Fuel Oil Upgrading ProcessesamitPas encore d'évaluation

- Petroleum Exploration & Production POLICY 2011: Government of Pakistan Ministry of Petroleum & Natural ResourcesDocument54 pagesPetroleum Exploration & Production POLICY 2011: Government of Pakistan Ministry of Petroleum & Natural ResourcesShaista IshaqPas encore d'évaluation

- General: GDP Is Expected To Grow in The Region of 8.75% To 9.25%. The MinisterDocument5 pagesGeneral: GDP Is Expected To Grow in The Region of 8.75% To 9.25%. The MinisterSuraj NaikPas encore d'évaluation

- SPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field EconomicsDocument19 pagesSPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field Economicsipali4christ_5308248Pas encore d'évaluation

- Transfer Pricing Rules DecodingDocument74 pagesTransfer Pricing Rules DecodingWaqas AtharPas encore d'évaluation

- RTI Handbook IndiaDocument31 pagesRTI Handbook Indiaashish08394Pas encore d'évaluation

- 1.0 Financial Modeling Intro v2Document28 pages1.0 Financial Modeling Intro v2Arif JamaliPas encore d'évaluation

- Nigeria The Dynamics of A Growing Gas Market - Presentation To The Africa Energy Forum 2008Document9 pagesNigeria The Dynamics of A Growing Gas Market - Presentation To The Africa Energy Forum 2008Adeoye AdefuluPas encore d'évaluation

- Presentation On PIB 2020Document27 pagesPresentation On PIB 2020Adegbola OluwaseunPas encore d'évaluation

- Large PipesDocument3 pagesLarge Pipesqais bakrPas encore d'évaluation

- Evolutionary Programming Based Economic Power Dispatch Solutions With Independent Power ProducersDocument6 pagesEvolutionary Programming Based Economic Power Dispatch Solutions With Independent Power Producersapi-3697505Pas encore d'évaluation

- Demand Dignity: Petrol, Pollution + Poverty in The Niger DeltaDocument24 pagesDemand Dignity: Petrol, Pollution + Poverty in The Niger Deltasouleymane2013Pas encore d'évaluation

- Production Sharing Agreement - Wikipedia, The Free EncyclopediaDocument3 pagesProduction Sharing Agreement - Wikipedia, The Free EncyclopediaandinumailPas encore d'évaluation

- FMA Cash Flow StatementsDocument19 pagesFMA Cash Flow Statementskanha PanigrahyPas encore d'évaluation

- CIMA GBC 2015 Case StudyDocument25 pagesCIMA GBC 2015 Case StudyPasanPethiyagodePas encore d'évaluation

- Financing LNG Projects - Excellent Presentation Goldman SachDocument11 pagesFinancing LNG Projects - Excellent Presentation Goldman SachUJJWALPas encore d'évaluation

- Msla Business FeesDocument1 pageMsla Business FeesNBC MontanaPas encore d'évaluation

- Annuity and Toll Difference in NHAI BOT ProjectsDocument3 pagesAnnuity and Toll Difference in NHAI BOT Projectsjavedarzoo50% (2)

- Cost of ProductionDocument1 pageCost of ProductionPRATIK P. BHOIRPas encore d'évaluation

- Ior in NigeriaDocument6 pagesIor in NigeriaTayo AwololaPas encore d'évaluation

- Session 6 - Case Study On Haripur 360 MW Combined Cycle Power Plant by Nazrul IslamDocument27 pagesSession 6 - Case Study On Haripur 360 MW Combined Cycle Power Plant by Nazrul IslamFarukHossainPas encore d'évaluation

- Re-Engineering The Uk Construction Industry: The Process ProtocolDocument12 pagesRe-Engineering The Uk Construction Industry: The Process ProtocolGeeta RamsinghPas encore d'évaluation

- IB Final ShellDocument25 pagesIB Final ShellsnehakopadePas encore d'évaluation

- Asset ManagementDocument12 pagesAsset ManagementSantosh JhawarPas encore d'évaluation

- MNLP (I.e., MINLP) Model For Optimal Synthesis and Operation of Utility PlantsDocument35 pagesMNLP (I.e., MINLP) Model For Optimal Synthesis and Operation of Utility PlantsErhan OğuşPas encore d'évaluation

- Understanding The Big Data Problems and Their Solutions Using Hadoop and Map-ReduceDocument7 pagesUnderstanding The Big Data Problems and Their Solutions Using Hadoop and Map-ReduceInternational Journal of Application or Innovation in Engineering & ManagementPas encore d'évaluation

- OG MarketDocument276 pagesOG MarketoptisearchPas encore d'évaluation

- Nigerian Local Content Oil and GasDocument4 pagesNigerian Local Content Oil and GasBalogun Ruth Oluwatosin100% (1)

- Mine Valuation of A Typical Gold Deposit: Technical ParametersDocument8 pagesMine Valuation of A Typical Gold Deposit: Technical ParametersGwen Ibarra SuaybaguioPas encore d'évaluation

- Processing Model From Mining ProspectiveDocument5 pagesProcessing Model From Mining ProspectiveijsretPas encore d'évaluation

- The Role of Big DataDocument27 pagesThe Role of Big DataNina FilipovićPas encore d'évaluation

- Appendix 7 Financials: Income StatementDocument12 pagesAppendix 7 Financials: Income StatementHamza MalikPas encore d'évaluation

- Refinery Configuration (With Figures)Document9 pagesRefinery Configuration (With Figures)phantanthanhPas encore d'évaluation

- Aspen Basic EngineeringDocument5 pagesAspen Basic Engineeringnaren_013Pas encore d'évaluation

- Plexos Tutorials Session-1Document85 pagesPlexos Tutorials Session-1zrqtsinghuaPas encore d'évaluation

- Statoil PresentationDocument30 pagesStatoil PresentationsergeyalejandroPas encore d'évaluation

- ABC WeDig+Diagnostics 228003Document5 pagesABC WeDig+Diagnostics 228003Svetlana VladyshevskayaPas encore d'évaluation

- Petrobangla: Daily Gas & Condensate Production and Distribution Report I. Production III. LPG ProductionDocument3 pagesPetrobangla: Daily Gas & Condensate Production and Distribution Report I. Production III. LPG ProductionMohammadPas encore d'évaluation

- Abridged Dangote Cement and BCC Scheme of Merger-170910Document36 pagesAbridged Dangote Cement and BCC Scheme of Merger-170910ProsharePas encore d'évaluation

- Lecture-3 Crude Oil PropertiesDocument61 pagesLecture-3 Crude Oil PropertiesMrHemFun100% (1)

- Hybrid Fuel Cell Gas Turbine SystemsDocument32 pagesHybrid Fuel Cell Gas Turbine Systemsİsmail Cem OktayPas encore d'évaluation

- Oag SuppDocument28 pagesOag SuppMeghhsPas encore d'évaluation

- A Study On Capital Budgeting at Bharathi Cement LTDDocument4 pagesA Study On Capital Budgeting at Bharathi Cement LTDEditor IJTSRDPas encore d'évaluation

- Refining IndustryDocument73 pagesRefining IndustryMukesh Kumar MeenaPas encore d'évaluation

- Chapter-1-2, EMC DSA NotesDocument8 pagesChapter-1-2, EMC DSA NotesakragnarockPas encore d'évaluation

- ACF5950-Assignment-2801656-kaidi ZhangDocument13 pagesACF5950-Assignment-2801656-kaidi ZhangkietPas encore d'évaluation

- AbtngDocument5 pagesAbtngSushant PaiPas encore d'évaluation

- Reforming Process - Catalyst Advancement: A Presentation OnDocument23 pagesReforming Process - Catalyst Advancement: A Presentation OnSiddharth Sharma100% (1)

- Rao 2018Document81 pagesRao 2018Sultan AlmaghrabiPas encore d'évaluation

- Strategy 4 Gas FlaringDocument13 pagesStrategy 4 Gas Flaringwhale007Pas encore d'évaluation

- CERC's Analysis Solar PV CostDocument3 pagesCERC's Analysis Solar PV Costs_kohli2000Pas encore d'évaluation

- 2 - 4.2 Wileman - Africa RegionDocument10 pages2 - 4.2 Wileman - Africa Regions_kohli2000Pas encore d'évaluation

- Best Practices For Supercritical PlantsDocument490 pagesBest Practices For Supercritical PlantsktsnlPas encore d'évaluation

- Bahrain Waste To Energy PDFDocument6 pagesBahrain Waste To Energy PDFs_kohli2000Pas encore d'évaluation

- Goals SettingDocument11 pagesGoals Settings_kohli2000100% (1)

- Robinhood Case StudyDocument2 pagesRobinhood Case StudyUdaya ChoudaryPas encore d'évaluation

- Power Sector Development in MyanmarDocument27 pagesPower Sector Development in Myanmars_kohli20000% (1)

- Upcoming GTPP / CCPP Opportunities For LIG & LII: Ason15 June 2009Document1 pageUpcoming GTPP / CCPP Opportunities For LIG & LII: Ason15 June 2009s_kohli2000Pas encore d'évaluation

- Asia Pacific Partnership India Peer Review ParticipantsListDocument9 pagesAsia Pacific Partnership India Peer Review ParticipantsLists_kohli2000Pas encore d'évaluation

- Power Projects Seeking Gas AllocationDocument3 pagesPower Projects Seeking Gas Allocations_kohli2000Pas encore d'évaluation

- Top Plant: Amman East Power Plant, Al Manakher, Jordan: Owner/operator: AES Jordan PSCDocument3 pagesTop Plant: Amman East Power Plant, Al Manakher, Jordan: Owner/operator: AES Jordan PSCs_kohli2000Pas encore d'évaluation

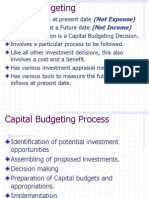

- Cash Outflow Cash Inflow: (Not Expense) (Not Income)Document15 pagesCash Outflow Cash Inflow: (Not Expense) (Not Income)s_kohli2000Pas encore d'évaluation

- SEC Projects 2010 - 2018Document1 pageSEC Projects 2010 - 2018s_kohli2000100% (1)

- Japanese Companies in IndiaDocument18 pagesJapanese Companies in Indias_kohli2000Pas encore d'évaluation

- Industrial X-Ray & Allied Radiographers (I) Pvt. LTDDocument1 pageIndustrial X-Ray & Allied Radiographers (I) Pvt. LTDABHIJEETPas encore d'évaluation

- Reliance Petcoke Maitra-RelianceDocument20 pagesReliance Petcoke Maitra-Reliancestavros7Pas encore d'évaluation

- Vaca Muerta Shale OilDocument20 pagesVaca Muerta Shale OilYamamoto_KZPas encore d'évaluation

- Global Oil ComapnyDocument18 pagesGlobal Oil ComapnySantosh KumarPas encore d'évaluation

- Chapter 7 Production UTMDocument56 pagesChapter 7 Production UTMNurzanM.JefryPas encore d'évaluation

- NelpDocument27 pagesNelpkhandelwalnakulPas encore d'évaluation

- MON Calculation For Compounds: Motor Octane Factor As Per IS 14861:2000Document2 pagesMON Calculation For Compounds: Motor Octane Factor As Per IS 14861:2000kvsr0205Pas encore d'évaluation

- Assignment NameDocument5 pagesAssignment NameVenkatRamanaPas encore d'évaluation

- Agora Energiewende - Flexibility in Thermal Power Plants: P P Ramp RateDocument2 pagesAgora Energiewende - Flexibility in Thermal Power Plants: P P Ramp Ratezisis81Pas encore d'évaluation

- Offshore Magazine MayDocument94 pagesOffshore Magazine MaynokarajuPas encore d'évaluation

- 2021 ShareholdingStructure ENDocument35 pages2021 ShareholdingStructure ENPanu PhumtabtimPas encore d'évaluation

- Coal and Petroleum - Notes - 220908 - 185218Document14 pagesCoal and Petroleum - Notes - 220908 - 185218VENKATESH PRABHUPas encore d'évaluation

- GIIGNL 2022 Annual Report 1652020175Document76 pagesGIIGNL 2022 Annual Report 1652020175Roberto RuizPas encore d'évaluation

- UntitledDocument62 pagesUntitledbleuz00mPas encore d'évaluation

- Iran Investment Companies NSDocument24 pagesIran Investment Companies NSvasucristalPas encore d'évaluation

- Gulf of Mexico Oil Spill Explosion RuptureDocument203 pagesGulf of Mexico Oil Spill Explosion RuptureVincent J. CataldiPas encore d'évaluation

- Oil History in EuropeDocument24 pagesOil History in EuropeBudi SantosoPas encore d'évaluation

- Petroleum Industry Report 2017 18 PDFDocument96 pagesPetroleum Industry Report 2017 18 PDFAamir SamiPas encore d'évaluation

- Revised Bitumen Price Wef 01.11.2022Document3 pagesRevised Bitumen Price Wef 01.11.2022Manas Kumar Swain100% (1)

- Industrial Fleet Master Samudera ShippingDocument5 pagesIndustrial Fleet Master Samudera ShippingherlambangPas encore d'évaluation

- Essential Commodity Act, 1955Document25 pagesEssential Commodity Act, 1955sneh7335Pas encore d'évaluation

- Tender 6.11.2023Document211 pagesTender 6.11.2023Chandar RajuPas encore d'évaluation

- Anugerah Bumi IndoDocument1 pageAnugerah Bumi IndoassyfhaaarobbiPas encore d'évaluation

- Tabela LubrimotorsDocument1 pageTabela LubrimotorsjaburecaPas encore d'évaluation

- Gas Authority of India LimitedDocument5 pagesGas Authority of India Limitedsanjay shelarPas encore d'évaluation

- Höegh LNG - Provider of Floating LNG ServicesDocument14 pagesHöegh LNG - Provider of Floating LNG ServicesHyeong-Ho KimPas encore d'évaluation

- PetroBangla Annual Report 2017 PDFDocument74 pagesPetroBangla Annual Report 2017 PDFAl Jawad100% (1)

- Petro Africa June-Issue2011Document72 pagesPetro Africa June-Issue2011karehman100% (1)

- Geology of The NetherlandsDocument7 pagesGeology of The Netherlandssslob_Pas encore d'évaluation

- GULFDocument33 pagesGULFJORDAN FREEPas encore d'évaluation