Vous aimerez peut-être aussi

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- SFH Rental AnalysisDocument6 pagesSFH Rental AnalysisA jPas encore d'évaluation

- Basic Rental Analysis WorksheetDocument8 pagesBasic Rental Analysis WorksheetGleb petukhovPas encore d'évaluation

- ABC Company, Inc. Recapitalization AnalysisDocument10 pagesABC Company, Inc. Recapitalization AnalysisMarcPas encore d'évaluation

- AN INTRODUCTION TO DEBT POLICY AND VALUE Case Syndicate 1 Cliff, Uri, Ary, KevinDocument7 pagesAN INTRODUCTION TO DEBT POLICY AND VALUE Case Syndicate 1 Cliff, Uri, Ary, KevinAntonius CliffSetiawanPas encore d'évaluation

- Nike Inc - Cost of Capital - Syndicate 10Document16 pagesNike Inc - Cost of Capital - Syndicate 10Anthony KwoPas encore d'évaluation

- Business ValuationDocument2 pagesBusiness Valuationahmed HOSNYPas encore d'évaluation

- Case 26 An Introduction To Debt Policy ADocument5 pagesCase 26 An Introduction To Debt Policy Amy VinayPas encore d'évaluation

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsD'EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsPas encore d'évaluation

- The Discounted Free Cash Flow Model For A Complete BusinessDocument2 pagesThe Discounted Free Cash Flow Model For A Complete BusinessHẬU ĐỖ NGỌCPas encore d'évaluation

- FIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadDocument3 pagesFIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadgPas encore d'évaluation

- Relative Value Models (Feb04)Document18 pagesRelative Value Models (Feb04)api-3763138Pas encore d'évaluation

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorPas encore d'évaluation

- Appendix B. Capital Budgeting TemplateDocument7 pagesAppendix B. Capital Budgeting TemplateAbel AliPas encore d'évaluation

- vAJ1-DCF Spreadsheet FreeDocument6 pagesvAJ1-DCF Spreadsheet FreesumanPas encore d'évaluation

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineD'EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LinePas encore d'évaluation

- 5 Year Financial Plan ManufacturingDocument30 pages5 Year Financial Plan ManufacturingLiza GeorgePas encore d'évaluation

- DCF Valuation-BDocument11 pagesDCF Valuation-BElsaPas encore d'évaluation

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachD'EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachÉvaluation : 3 sur 5 étoiles3/5 (3)

- Stryker Corporation - Assignment 22 March 17Document4 pagesStryker Corporation - Assignment 22 March 17Venkatesh K67% (6)

- Term Structure JP Morgan Model (Feb04)Document7 pagesTerm Structure JP Morgan Model (Feb04)api-3763138Pas encore d'évaluation

- Task 1 AnswerDocument9 pagesTask 1 AnswerSiddhant Aggarwal0% (4)

- April 8/91: All GroupsDocument33 pagesApril 8/91: All Groupsreza mirzakhaniPas encore d'évaluation

- Degree Polynomial:: Generic Yield Interpolation ChartDocument9 pagesDegree Polynomial:: Generic Yield Interpolation Chartapi-3763138Pas encore d'évaluation

- Corporate Finance Solution Chapter 6Document9 pagesCorporate Finance Solution Chapter 6Kunal KumarPas encore d'évaluation

- CFI - FMVA Practice Exam Case Study ADocument18 pagesCFI - FMVA Practice Exam Case Study AWerfelli MaramPas encore d'évaluation

- Categories of Cargo and Types of ShipsDocument14 pagesCategories of Cargo and Types of ShipsVibhav Kumar100% (1)

- Equity Analysis of A Project: Capital Budgeting WorksheetDocument8 pagesEquity Analysis of A Project: Capital Budgeting WorksheetanuradhaPas encore d'évaluation

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2deepika0% (1)

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2Yash JasaparaPas encore d'évaluation

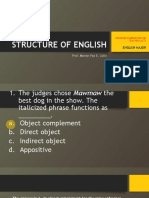

- LET-English-Structure of English-ExamDocument57 pagesLET-English-Structure of English-ExamMarian Paz E Callo80% (5)

- Bond Price With Excel FunctionsDocument6 pagesBond Price With Excel Functionsapi-3763138Pas encore d'évaluation

- MARTELINO Vs Alejandro DigestDocument1 pageMARTELINO Vs Alejandro Digestheirarchy100% (2)

- Fin 600 - Radio One-Team 3 - Final SlidesDocument20 pagesFin 600 - Radio One-Team 3 - Final SlidesCarlosPas encore d'évaluation

- Learning Module - Joints, Taps and SplicesDocument9 pagesLearning Module - Joints, Taps and SplicesCarlo Cartagenas100% (1)

- Excel Spreadsheet For Mergers and Acquisitions ValuationDocument6 pagesExcel Spreadsheet For Mergers and Acquisitions Valuationisomiddinov100% (2)

- Catalogo Escavadeira EC27CDocument433 pagesCatalogo Escavadeira EC27CNilton Junior Kern50% (2)

- Cash Flow ModelDocument1 pageCash Flow ModelVinay KumarPas encore d'évaluation

- FcffevaDocument6 pagesFcffevaShobhit GoyalPas encore d'évaluation

- Inputs For Valuation Current InputsDocument6 pagesInputs For Valuation Current InputsÃarthï ArülrãjPas encore d'évaluation

- High GrowthDocument30 pagesHigh GrowthAbhinav PandeyPas encore d'évaluation

- Inputs For Valuation Current Inputs (As A Naïve Estimate, You Can Use BV of Debt + BV of Equity)Document11 pagesInputs For Valuation Current Inputs (As A Naïve Estimate, You Can Use BV of Debt + BV of Equity)Long Bùi VănPas encore d'évaluation

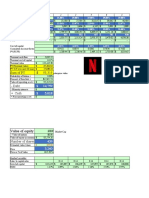

- Sum of PV $ 95,315: Netflix Base Year 1 2 3 4 5Document6 pagesSum of PV $ 95,315: Netflix Base Year 1 2 3 4 5Laura Fonseca SarmientoPas encore d'évaluation

- Amazon ValuationDocument22 pagesAmazon ValuationDr Sakshi SharmaPas encore d'évaluation

- 3 Statement Model STRAT 5XXXDocument6 pages3 Statement Model STRAT 5XXXdawson.ber2zPas encore d'évaluation

- I. Income StatementDocument27 pagesI. Income StatementNidhi KaushikPas encore d'évaluation

- Facebook IPO caseHBRDocument29 pagesFacebook IPO caseHBRCrazy Imaginations100% (1)

- Assignment Dataset 1Document19 pagesAssignment Dataset 1Chip choiPas encore d'évaluation

- Cash Flow - Lecture 2Document11 pagesCash Flow - Lecture 2abbasaltarouti1000Pas encore d'évaluation

- Apple TTMDocument25 pagesApple TTMQuofi SeliPas encore d'évaluation

- 2008-2-00474-TI LampiranDocument3 pages2008-2-00474-TI LampiranMuhamad AzwarPas encore d'évaluation

- Capbudgeting For Smart DiapersDocument8 pagesCapbudgeting For Smart Diapersمحمد عليPas encore d'évaluation

- Year 1 Year 2 Panel A - Projected Free Cash FlowDocument7 pagesYear 1 Year 2 Panel A - Projected Free Cash FlowLede Ann Calipus YapPas encore d'évaluation

- FCFF 3 STDocument3 pagesFCFF 3 STKartikeya AryaPas encore d'évaluation

- Varma Capitals - Modeling TestDocument6 pagesVarma Capitals - Modeling TestSuper FreakPas encore d'évaluation

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2dikshapatil6789Pas encore d'évaluation

- Financial PlanDocument5 pagesFinancial PlanVivian CorpuzPas encore d'évaluation

- Input Page: Market Inputs For Your Company From The Balance SheetDocument20 pagesInput Page: Market Inputs For Your Company From The Balance SheetLevy APas encore d'évaluation

- Capital Budgeting Template-Jumawid, Joyce S.Document8 pagesCapital Budgeting Template-Jumawid, Joyce S.Aian Kit Jasper SanchezPas encore d'évaluation

- Common Size Income StatementDocument7 pagesCommon Size Income StatementUSD 654Pas encore d'évaluation

- EuroTunnDCFDocument11 pagesEuroTunnDCFNgọc Hiền Nguyễn PhanPas encore d'évaluation

- DCF Financial Model Blank BDocument24 pagesDCF Financial Model Blank BBHAVVYA WADHERAPas encore d'évaluation

- AmazonDocument16 pagesAmazonEsteban Camilo Ortiz ZambranoPas encore d'évaluation

- CH 11 - CF Estimation Mini Case Sols Word 1514edDocument13 pagesCH 11 - CF Estimation Mini Case Sols Word 1514edHari CahyoPas encore d'évaluation

- Inputs For Valuation Current Inputs (As A Naïve Estimate, You Can Use BV of Debt + BV of Equity)Document6 pagesInputs For Valuation Current Inputs (As A Naïve Estimate, You Can Use BV of Debt + BV of Equity)minhthuc203Pas encore d'évaluation

- IS Excel Participant (Risit Savani) - Simplified v2Document9 pagesIS Excel Participant (Risit Savani) - Simplified v2risitsavaniPas encore d'évaluation

- The Discounted Free Cash Flow Model For A Complete BusinessDocument2 pagesThe Discounted Free Cash Flow Model For A Complete BusinessBacarrat BPas encore d'évaluation

- Multifamily Apartment ProformaDocument4 pagesMultifamily Apartment Proformaartsan3Pas encore d'évaluation

- W10 Excel Model Cash Flow, Net Cost, and Capital BudgetingDocument5 pagesW10 Excel Model Cash Flow, Net Cost, and Capital BudgetingJuan0% (1)

- Remodelers' Cost of Doing Business Study, 2020 EditionD'EverandRemodelers' Cost of Doing Business Study, 2020 EditionPas encore d'évaluation

- Cody - Smith - Chap 4Document36 pagesCody - Smith - Chap 4api-3763138100% (1)

- SchwartzMoon (2000) Rational Pricing Internet CpyDocument14 pagesSchwartzMoon (2000) Rational Pricing Internet Cpyapi-3763138Pas encore d'évaluation

- Estimating Growth Rates (Teaching Model)Document4 pagesEstimating Growth Rates (Teaching Model)api-3763138Pas encore d'évaluation

- Optimal Portfolio Assignment Solution StrudwickDocument10 pagesOptimal Portfolio Assignment Solution Strudwickapi-3763138Pas encore d'évaluation

- Optimal Portfolio Assignment FINA 515 2005 Ray Guo (P)Document76 pagesOptimal Portfolio Assignment FINA 515 2005 Ray Guo (P)api-3763138Pas encore d'évaluation

- Stiglitz Weiss 1981 Implementation by Kurt HessDocument20 pagesStiglitz Weiss 1981 Implementation by Kurt Hessapi-3763138Pas encore d'évaluation

- Cody - Smith - Chap 5Document24 pagesCody - Smith - Chap 5api-3763138Pas encore d'évaluation

- Endowment - Warrant - Valuer (McVerry) DDocument244 pagesEndowment - Warrant - Valuer (McVerry) Dapi-3763138Pas encore d'évaluation

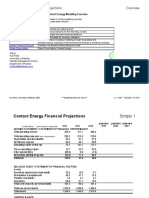

- Contact - Main 2006Document89 pagesContact - Main 2006api-3763138Pas encore d'évaluation

- Δr=α b−r Δt+σε Δt: Simulation of short-term interest ratesDocument19 pagesΔr=α b−r Δt+σε Δt: Simulation of short-term interest ratesapi-3763138Pas encore d'évaluation

- Refresh Worksheet ListDocument14 pagesRefresh Worksheet Listapi-3763138Pas encore d'évaluation

- BbandsDocument12 pagesBbandsapi-3763138Pas encore d'évaluation

- Stock Price Random ProcessesDocument63 pagesStock Price Random Processesapi-3763138Pas encore d'évaluation

- Spline Basis Function Approximating Discount Function Fitting Bond UniverseDocument5 pagesSpline Basis Function Approximating Discount Function Fitting Bond Universeapi-3763138Pas encore d'évaluation

- Longstaff Schwartz (95) Risky Debt (P)Document18 pagesLongstaff Schwartz (95) Risky Debt (P)api-3763138Pas encore d'évaluation

- Bond Pricing - Dynamic ChartDocument4 pagesBond Pricing - Dynamic Chartapi-3763138Pas encore d'évaluation

- Converts PrimerDocument6 pagesConverts Primerjunjun07_01Pas encore d'évaluation

- RV YTM Model PDFDocument47 pagesRV YTM Model PDFAllen LiPas encore d'évaluation

- Bond Pricing - by Yield To MaturityDocument3 pagesBond Pricing - by Yield To Maturityapi-3763138Pas encore d'évaluation

- Bond Duration - Price Sensitivity Using DurationDocument3 pagesBond Duration - Price Sensitivity Using Durationapi-3763138Pas encore d'évaluation

- Bond Pricing - Dynamic ChartDocument4 pagesBond Pricing - Dynamic Chartapi-3763138Pas encore d'évaluation

- Bond Pricing - System of Five Bond VariablesDocument2 pagesBond Pricing - System of Five Bond Variablesapi-3763138Pas encore d'évaluation

- Bond Pricing - BasicsDocument2 pagesBond Pricing - Basicsapi-3763138Pas encore d'évaluation

- Bond Duration - Dynamic ChartDocument3 pagesBond Duration - Dynamic Chartapi-3763138Pas encore d'évaluation

- 353 Version 7thDocument1 page353 Version 7thDuc NguyenPas encore d'évaluation

- Mahindra First Choice Wheels LTD: 4-Wheeler Inspection ReportDocument5 pagesMahindra First Choice Wheels LTD: 4-Wheeler Inspection ReportRavi LovePas encore d'évaluation

- Black Hole Safety Brochure Trifold FinalDocument2 pagesBlack Hole Safety Brochure Trifold Finalvixy1830Pas encore d'évaluation

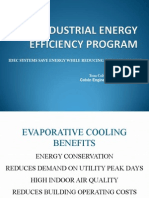

- Evaporative CoolingDocument68 pagesEvaporative Coolingshivas34regal100% (1)

- MPPSC ACF Test Paper 8 (26 - 06 - 2022)Document6 pagesMPPSC ACF Test Paper 8 (26 - 06 - 2022)Hari Harul VullangiPas encore d'évaluation

- Listening Tests 81112Document13 pagesListening Tests 81112luprof tpPas encore d'évaluation

- Project On Mahindra BoleroDocument35 pagesProject On Mahindra BoleroViPul75% (8)

- You're reading a free preview. Pages 4 to 68 are not shown in this preview. Leer la versión completa You're Reading a Free Preview Page 4 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 5 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 6 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 7 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 8 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 9 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 10 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 11 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 12 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 13 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 14 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 15 is notDocument9 pagesYou're reading a free preview. Pages 4 to 68 are not shown in this preview. Leer la versión completa You're Reading a Free Preview Page 4 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 5 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 6 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 7 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 8 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 9 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 10 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 11 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 12 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 13 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 14 is not shown in this preview. DESCARGA You're Reading a Free Preview Page 15 is notFernando ToretoPas encore d'évaluation

- PUPiApplyVoucher2017 0006 3024Document2 pagesPUPiApplyVoucher2017 0006 3024MätthëwPïńëdäPas encore d'évaluation

- Approved College List: Select University Select College Type Select MediumDocument3 pagesApproved College List: Select University Select College Type Select MediumDinesh GadkariPas encore d'évaluation

- NOV23 Nomura Class 6Document54 pagesNOV23 Nomura Class 6JAYA BHARATHA REDDYPas encore d'évaluation

- Chapter 3 Depreciation - Sum of The Years Digit MethodPart 4Document8 pagesChapter 3 Depreciation - Sum of The Years Digit MethodPart 4Tor GinePas encore d'évaluation

- Edtpa Lesson 3Document3 pagesEdtpa Lesson 3api-299319227Pas encore d'évaluation

- Lesson 23 Career PathwaysDocument34 pagesLesson 23 Career PathwaysAlfredo ModestoPas encore d'évaluation

- Model 900 Automated Viscometer: Drilling Fluids EquipmentDocument2 pagesModel 900 Automated Viscometer: Drilling Fluids EquipmentJazminPas encore d'évaluation

- Skilled Worker Overseas FAQs - Manitoba Immigration and Economic OpportunitiesDocument2 pagesSkilled Worker Overseas FAQs - Manitoba Immigration and Economic OpportunitieswesamPas encore d'évaluation

- 6 - European Cluster Partnership For Excellence - European Cluster Collaboration PlatformDocument5 pages6 - European Cluster Partnership For Excellence - European Cluster Collaboration PlatformDaniela DurducPas encore d'évaluation

- ACTIX Basic (Sample CDMA)Document73 pagesACTIX Basic (Sample CDMA)radhiwibowoPas encore d'évaluation

- Load Schedule: DescriptionDocument1 pageLoad Schedule: Descriptionkurt james alorroPas encore d'évaluation

- Lugam Annex Elementary School Second Quarter Second Periodical Test in EPP 6 H.EDocument4 pagesLugam Annex Elementary School Second Quarter Second Periodical Test in EPP 6 H.Ejess amielPas encore d'évaluation

- Coc 1 ExamDocument7 pagesCoc 1 ExamJelo BioPas encore d'évaluation

- Technology 6 B Matrixed Approach ToDocument12 pagesTechnology 6 B Matrixed Approach ToNevin SunnyPas encore d'évaluation

- Aashirwaad Notes For CA IPCC Auditing & Assurance by Neeraj AroraDocument291 pagesAashirwaad Notes For CA IPCC Auditing & Assurance by Neeraj AroraMohammed NasserPas encore d'évaluation

- 6 RVFS - SWBL Ojt Evaluation FormDocument3 pages6 RVFS - SWBL Ojt Evaluation FormRoy SumugatPas encore d'évaluation