Académique Documents

Professionnel Documents

Culture Documents

WACC Report en

Transféré par

zlatan_juric0 évaluation0% ont trouvé ce document utile (0 vote)

44 vues86 pageswacc, proracun

Titre original

WACC Report En

Copyright

© © All Rights Reserved

Formats disponibles

PDF, TXT ou lisez en ligne sur Scribd

Partager ce document

Partager ou intégrer le document

Avez-vous trouvé ce document utile ?

Ce contenu est-il inapproprié ?

Signaler ce documentwacc, proracun

Droits d'auteur :

© All Rights Reserved

Formats disponibles

Téléchargez comme PDF, TXT ou lisez en ligne sur Scribd

0 évaluation0% ont trouvé ce document utile (0 vote)

44 vues86 pagesWACC Report en

Transféré par

zlatan_juricwacc, proracun

Droits d'auteur :

© All Rights Reserved

Formats disponibles

Téléchargez comme PDF, TXT ou lisez en ligne sur Scribd

Vous êtes sur la page 1sur 86

Frontier Economics Ltd, London.

The impact from regulatory regimes on

the WACC

A REPORT FOR RWE GASNET

September 2013

September 2013 | Frontier Economics i

Contents

The impact from regulatory regimes on

the WACC

Executive Summary 1

1 Background and scope of the study 7

1.1 Context....................................................................................... 7

1.2 Scope of the study ..................................................................... 7

1.3 Structure of the report ................................................................ 8

2 Regulation of energy network in Czech Republic 9

2.1 Regulation of energy networks 2010 to 2014 .......................... 9

2.2 EROs actions during 3

rd

regulatory period .............................. 10

2.3 EROs action and the regulatory climate .................................. 11

3 Relationship between regulation and risk 13

3.1 Channels for transmitting changes in risk to the WACC .......... 13

3.2 Role of regulation in the cost of financing ................................ 15

3.3 Regulation and risk the view from rating agencies ................ 19

3.4 Key findings Regulation and risk ........................................... 22

4 Regulation and risk selected European countries 23

4.1 UK ............................................................................................ 24

4.2 Germany .................................................................................. 33

4.3 France ...................................................................................... 40

4.4 Key findings Regulation and risk in UK, Germany and France

................................................................................................. 48

5 Regulation and risk Czech Republic 49

5.1 Stability and Predictability of the Regulatory Regime ............... 49

5.2 Cost and Investment Recovery and Revenue Risk ............. 55

5.3 WACC Cost recovery for cost of capital at risk ..................... 61

5.4 Key findings Regulation and Risk for CZ gas distribution

companies ................................................................................ 67

ii Frontier Economics | September 2013

Contents

6 Conclusion 69

7 References 73

September 2013 | Frontier Economics iii

Tables & Figures

The impact from regulatory regimes on

the WACC

Figure 1. Channels for transmission of risk changes to the WACC 14

Figure 2. Principal outputs under RIIO GD1 30

Figure 3. Investment indicators 44

Figure 4. Quality of service indicators 45

Table 1. Regulation and Risk and the impact on cost of capital 2

Table 2. Regulation and Risk and the impact on cost of capital 5

Table 3. Moody's methodology for rating regulated electricity and gas

networks 20

Table 4. Regulatory parameters RIIO-GD1 29

Table 5. WACC parameter UK 32

Table 6. Regulatory parameters Germany 36

Table 7. Cost of equity parameter Germany 38

Table 8. Regulatory parameters France 42

Table 9. WACC parameter France 46

Table 10. Regulation and Risk and the impact on cost of capital 48

Table 11. Stability and Predictability of Regulatory Regime from 3

rd

to

4

th

regulatory period 55

Table 12. Regulatory components CZ gas distribution companies 56

Table 13. Cost and Investment Recovery and Revenue Risk from

3

rd

to 4

th

regulatory period 59

Table 14. WACC 3

rd

to 4

th

regulatory period 62

Table 15. Frontiers assessment Rating factors from 3

rd

to 4

th

regulatory period 63

Table 16. Regulation and Risk and the impact on cost of capital 70

September 2013 | Frontier Economics 1

Executive Summary

September 2013 | Frontier Economics 1

Executive Summary

Executive Summary

ERO proposes substantial adjustments and changes for 4

th

regulatory

period

The Czech regulator ERO is responsible for the regulation of the electricity and

gas network companies. The current revenues are set according to the decision

on the 3

rd

regulatory period (2010-2014) from December 2009, which was the

result of a consultation process with all relevant stakeholders starting in 2008. In

March 2013 ERO made a first proposal for the regulatory framework of the 4

th

regulatory period including substantial adjustment compared to the previous one,

in particular the reversal of former partially acknowledged asset revaluation and a

shortening of the 3

rd

regulatory period. In August 2013 ERO issued a new

proposal including new regulatory instruments and a reduction in the WACC

compared to the March 2013 document.

RWE Gasnet asked Frontier to compare the regulatory and legal regime and their

main components for European peers with the CZ regime with regard to the risk

profile regulated entities face and to assess the alignment of the proposed WACC

by ERO with the potential increase in risk since the start of the 3

rd

regulatory

period.

Regulatory actions will influence the cost of capital by altering the risks

faced by equity and debt investors

The cost of capital represents the minimum rate of return companies must pay in

order to attract capital from investors. Changes in risk will affect equity investors

and debt investors via different channels. Risk will feed into the

cost of equity via the beta; and

cost of debt via the debt premium.

Regulatory actions and regulatory design will influence the cost of capital by

altering the risks faced by businesses. Credit rating indicators can reflect the

various aspects of the regulatory environment. Moodys covers the regulatory

environment by:

Stability and Predictability of the Regulatory Regime;

Cost and Investment Recovery; and

Revenue Risk.

Regulatory systems can be compared by analysing how they perform against

these indicators and how business risks influence the beta and debt premium.

2 Frontier Economics | September 2013

Executive Summary

Regulation and risk in selected European countries UK, Germany

and France

In order to assess the return/risk profile of the Czech Republic we compared the

regulatory framework with regard to the three Moodys factors covering the

regulatory environment for UK, Germany and France. UK sets the benchmark

(Aaa) for Stability and Predictability of Regulatory Regime. Germany (A) and France

(Aa) get a slight lower rating by Moodys. For Cost and Investment Recovery Moodys

rated the countries in the range of A to Baa, Revenue risk in the range of Aaa to A.

The corresponding beta and debt premium set by the regulatory authorities in

UK, Germany and France are:

asset beta in the range of 0.38 to 0.46;

equity beta in the range of 0.76 to 0.90; as well as

debt premium in the range of 0.60% to 0.90%.

Table 1. Regulation and Risk and the impact on cost of capital

UK

(2013-2021)

Germany

(2013-2017)

France

(2012-2015)

Stability and Predictability of Regulatory Regime Aaa A Aa

Cost and Investment Recovery A Baa A

Revenue Risk Aaa A Aa

Asset beta 0.38 0.39 0.46

Equity beta 0.90 0.79 0.76

Debt premium 0.90% na 0.60%

Source: UK Moodys; Germany and France and Frontier assessment based on Moodys ratings for

HSE Netz (Germany) and TIGF (France)

Deterioration of Stability and Predictability of CZ Regulatory Regime

between 3

rd

and 4

th

regulatory period

First, we compared the regulatory framework of the 3

rd

regulatory period for gas

distribution companies with the draft proposal from ERO for the 4

th

regulatory

period. Based on this comparison, we assess the potential impact on risk faced by

the companies. We also take EROs action during the 3

rd

regulatory period into

account. Second, we compared the new draft proposal from ERO for the 4

th

regulatory period and its corresponding return/risk profile with the relevant

profiles from UK, Germany and France.

September 2013 | Frontier Economics 3

Executive Summary

With regard to Stability and Predictability of Regulatory Regime we conclude that

EROs actions may be classified as a

non consistent application of the regulatory framework for the 3

rd

regulatory period; or even a

significant change compared to the 3

rd

regulatory period.

We assess a significant downgrading of Stability and Predictability of Regulatory

Regime in the 4

th

regulatory period.

Cost and Investment Recovery and Revenue Risk also affected by

EROs proposal

There are various factors having a potential adverse direct impact on the Cost and

Investment Recovery and Revenue Risk. The main impact stems from the Network

utilisation factor, where the specification and application is still pending. We note

that the Network utilisation factor depending on its final specification may

induce even a sharp downgrade due to asset stranding and/or high exposure to

volume risk. In addition, the new mechanism for network losses may have an

adverse impact, as well, if ERO is reluctant on increasing network losses. As long

as this is still an unresolved issue we make the assumption that the new

parameter will slightly increase the risk of cost recovery and the revenue risk

resulting in a small downgrade compared to the 3

rd

regulatory period. Finally, the

efficiency assessment of operating expenditure which allows a retrospective

reduction of costs may jeopardize cost recovery, as well.

Cost Recovery for cost of capital at risk in 4

th

regulatory period

In order to assess if the current WACC proposal covers the risks borne by

investors in the Czech gas distribution sector it is necessary to compare the risks

faced by companies between the 3

rd

and 4

th

regulatory period. Applying the logic

of Moodys rating factors, we assess that the risk faced by gas distribution

companies increased between the 3

rd

and 4

th

regulatory period due to

increased uncertainty on the Stability and Predictability of Regulatory regime;

and

new proposed regulatory parameters which are yet unspecified and may

have an adverse effect on Cost and Investment Recovery and Revenue Risk

In addition, we assessed a potential adverse effect on selected Moodys key credit

metrics, Adjusted Interest Coverage Rate and Retained Cash Flow/Capex from the

reversal of asset revaluation.

Hence, in order to allow cost recovery for equity and debt investors the

increased risk should be reflected in the asset (equity) beta and debt

premium.

4 Frontier Economics | September 2013

Executive Summary

Adjustments of beta and debt premium in 4

th

regulatory period to allow

cost recovery

In order to allow cost recovery for the cost of capital the relevant parameters

through which this increased risk flows into the WACC beta and debt premium

should follow the principles outlined below.

Cost of equity The level of the asset (equity) beta from the 3

rd

regulatory

period should serve as the starting point for the 4

th

regulatory period. In

order to allow cost recovery a mark-up on this value covering the increased

risk between the 3

rd

and 4

th

regulatory period should be applied. This implies

an asset (equity) beta in the range of 0.45 to 0.50 (0.69 to 0.77) for the

4

th

regulatory period. Compared with the respective values for UK, Germany

and France and taking into account the higher rating in particular for the

important factor Stability and Predictability of Regulatory Regime in all

three countries this range seems to be a reasonable risk adjusted asset beta

and equity beta (Table 2) taking into account the lower notional gearing

(40%) proposed by ERO compared with UK (65%), Germany (60%) and

France (50%).

Cost of debt The risk faced by debt investors between the 3

rd

and 4

th

regulatory period did not decrease (in contrary the risk increased). This

implies that the implicit debt premium from the 3

rd

regulatory period should

serve as the starting point for the 4

th

regulatory period. However, we further

identified a systematic problem in the way ERO currently determines the

cost of debt. ERO sets the cost of debt based on a short-term interest rate

(1-5years) which is in contrast with the longer term financing and investment

horizon for networks and European regulators best practice (substantially

above 5 years). Hence, the overall level of the regulatory cost of debt

may be substantially below market cost of debt. Hence, the

adjustment of the debt premium should reflect the switch from a short-term

to a longer-term interest rate. This results in a substantial higher debt

premium in the range of 0.70% to 1.30%, which is more in line with the

respective values used in UK and France. In addition, ERO should consider

including cost of raising debt in the debt premium in the range of 0.10% to

0.20%.

September 2013 | Frontier Economics 5

Executive Summary

Table 2. Regulation and Risk and the impact on cost of capital

3

rd

reg- period

(2010-2014)

4

th

reg-period

(Aug 2013)

UK

(2013-21)

Germany

(2013-17)

France

(2012-15)

Stability and

Predictability of

Regulatory Regime

Aa A * Ba B* Aaa** A** Aa**

Cost and Investment

Recovery

A* Baa Ba* A** Baa** A**

Revenue Risk Aa* A Baa* Aaa** A** Aa**

adjICR and RCF/Capex Potential

downward

pressure*

- - -

Asset beta 0.40 0.35 0.38 0.39 0.46

Equity beta 0.62 0.54 0.9 0.79 0.76

Debt premium (implicit) 0.31% 0.23% 0.90% na 0.60%

Frontier adjustments 3

rd

reg- period

(2010-2014)

4

th

reg-period

(Aug 2013)

Asset beta

(risk adjusted)

0.45 0.50

Equity beta

(risk adjusted)

0.69 0.77

Debt premium

(longer term interest rate)

0.70% - 1.30% 0.70% - 1.30%

Cost of raising debt 0.10% - 0.20%

Source: Frontier based on Moodys methodology, Moodys

* Assessment by Frontier

** Assessment by Moodys

Regulatory principles guiding the specification of the 4

th

regulatory

period

Provided that ERO still insisted in changing the regulatory framework in the 4

th

regulatory period in particular with regard to the reversal of asset revaluation then

at least ERO should adopt a more refined logic that explicitly considers the

following principles:

Avoidance of retrospective interventions Regulators and regulated

companies play a repeated interaction game, coming together periodically to

agree new cost allowances and incentive mechanisms that will apply for the

6 Frontier Economics | September 2013

Executive Summary

next period. Regulators credibility is therefore key: this also includes that

retrospective interventions shall be avoided.

Specification of regulatory framework The current ERO proposal for

the 4

th

regulatory period introduces various new regulatory changes and

regulatory instruments, e.g. the Network utilisation factor. However, there is

a low degree of specification which hampers companies to assess the specific

impact on their costs and/or revenues. In order to increase predictability for

companies and also investors a detailed description which can be translated

into companies business plans should be provided by ERO as soon as

possible.

Transparent decision rules In order to maximise the regulatory

commitment and stability, ERO should base any new measure announced in

the decision for the 4

th

regulatory period on transparent decisions rules,

which are known to the regulated companies ex ante. This means that the

regulated companies must know in advance, which behaviour will induce

measures by ERO. For example, this refers to the announced audits on the

efficient utilisation of funds from the Network obsolescence factor.

September 2013 | Frontier Economics 7

Background and scope of the study

1 Background and scope of the study

1.1 Context

The Czech regulator ERO is responsible for the regulation of the electricity and

gas network companies. The current revenues are set according to the decision

on the 3

rd

regulatory period (2010-2014) from December 2009, which was the

result of a consultation process with all relevant stakeholders starting in 2008. In

March 2013 ERO made a first proposal for the regulatory framework of the 4

th

regulatory period including substantial adjustment compared to the previous one,

in particular the reversal of former partially acknowledged asset revaluation. In

August 2013 ERO issued a new proposal including new regulatory instruments

and a reduction in the WACC compared to the March 2013 document. ERO

stick to the reversal of the asset revaluation, however, it stated that the new

regulatory instruments proposed in August 2013 increase the incentives to invest

and decrease the risk compared to the March 2013 proposal.

1.2 Scope of the study

RWE Gasnet is concerned on the potential impact from the proposed

adjustments on risk and the alignment of the risk with the proposed WACC by

ERO. In addition, RWE Gasnet is concerned on the long-term stability of the

proposed regulatory framework.

RWE Gasnet has asked Frontier to

Benchmark of the WACC parameters for European peers compared to the

CZ figures.

Compare the regulatory and legal regime and their main components for

European peers compared with the CZ regime with regard to the risk profile

regulated entities face in the CZ republic compared to European peers. This

includes e.g.

predictability of the behavior of the regulator;

possibility of legal actions against regulators decisions; as well as

regulatory components and their impact on various risks, e.g. volume

risk, cost risk.

Assess the WACC proposed by ERO in relation to the potential increase in

risk since the start of the 3

rd

regulatory period.

8 Frontier Economics | September 2013

Background and scope of the study

RWE Gasnet provided Frontier with the respective EROs draft proposals for

the 4

th

regulatory period from March 2013 (ERO 2013a) and August 2013 (ERO

2013b).

1.3 Structure of the report

The report is structured as follows:

Section 2 describes the regulatory system for CZ gas distribution companies

and the proposed changes for the 4

th

regulatory period.

Section 3 describes the relationship between regulation and risk and how a

change in the risk may feed into the cost of equity and the cost of debt.

Section 4 describes the relationship between the regulatory framework and

the WACC for three selected European countries, UK, Germany and

France.

Section 5 analysis behaviour of ERO since the start of the consultation

process for the 3

rd

regulatory period and the proposed changes for the 4

th

regulatory period with regard to the implication on the risks faced by the gas

distribution companies. The section analysis to what extent the proposed

WACC in ERO (2013b) aligns with the underlying risk exposure of the

companies.

Section 6 concludes the results.

September 2013 | Frontier Economics 9

Regulation of energy network in Czech Republic

2 Regulation of energy network in Czech

Republic

This section describes the Czech regulatory regime until the 3

rd

regulatory period

(2010-2014) and the proposed regulatory framework for the 4

th

regulatory period

(2015-2019) by the Czech regulator, ERO, with regard to asset revaluation.

2.1 Regulation of energy networks 2010 to 2014

The energy networks are regulated using a revenue cap. The regulatory period is

5 years. The Czech revenue cap is a combination of incentive regulation and

cost-plus regulation, where the first applies to operating costs and the latter to

capital costs.

In 2006 there was an one-off revaluation of the assets based on current costs

during the process of unbundling, which resulted in roughly a doubling of the

asset value compared to historic costs (step-up) which had to be reflected in

the accounting books of the company. Already in the 2

nd

regulatory period ERO

started a process of gradual acknowledgement of revaluated depreciation which

was accomplished in the 3

rd

regulatory period.

1

Allowing depreciations based on

revaluated assets at current cost in 2006 was a means of providing cash to the

companies in order to finance necessary investments.

The decision by ERO to acknowledge revaluated depreciation as allowed one was

taken after an intense assessment by the ERO and discussion between ERO and

the regulated companies on their long-term investment plans. For this a period of

15 years was evaluated. The submitted investment plan in 2009 forecasted for the

years 2010 2013 (already) lower investment than depreciation with growing

investments exceeding depreciation after 2014. Other aspect of the ERO strategy

of providing cash to the companies in the regulatory period was slower

depreciation of RAB via deduction of only a share of the allowed depreciation.

This share was determined by a ratio of RAB to the revaluated asset value. ERO

(2009: 16) stated in 2009 that if companies do not reinvest revaluated

depreciation in asset upgrades in a way to preserve their level and the quality of

supply, the Office will introduce a mechanism into regulation, which will ensure

that allowed depreciation is used solely for investment purposes under the

respective licence.

1

Energy Regulatory Office, Final Report of the Energy Regulatory Office on the regulatory methodology for the

third regulatory period, including the key parameters of the regulatory formula and pricing in the electricity and gas

industries, December 2009.

10 Frontier Economics | September 2013

Regulation of energy network in Czech Republic

The initial value of the regulatory asset base for the 3

rd

regulatory period (2010-

2014) has been based on the RAB 2009 which was acknowledged in the previous

regulatory period (based more or less on historical costs), which was then

adjusted by an initial revaluation coefficient. This revaluation coefficient was

calculated by dividing the previous RAB 2009 value with the revaluated asset

value in 2009 (comprising the one-off current cost revaluation in 2006 plus new

investments at historical costs between 2007 and 2009). Only, if the asset value at

historic costs is less than 50% of the revalued assets there is a step up of the

assets at historical costs to reach 50% of the revalued assets. In other cases the

initial RAB is set at the residual asset value 2009.

EROs hybrid approach in relation to asset revaluation differs from approaches

used by other European regulators. In countries where revaluation was applied

either based on historic or replacement costs , e.g. Norway, Netherlands,

Finland, Sweden, the revaluated assets were used to calculate depreciation and

also the allowed RAB (and not only to calculate depreciation as in the CZ

republic).

However, EROs objective for asset revaluation seemed to be similar: supporting

a long-term sustainable asset value and signalling investors the long-term stability

of the regulatory system with regard to the regulated asset base.

2.2 EROs actions during 3

rd

regulatory period

We understand that during the 3

rd

regulatory period a new head of ERO was

appointed by the Czech government with effect from August 1

st

, 2011. ERO

fundamentally changed its position in relation to asset revaluation. In 2012 ERO

made the legal assessment that the regulatory decision for the 3

rd

regulatory

period contradicts the Czech energy law, which according to the new

interpretation of ERO grants depreciation only for realized investments and not

on revaluated assets.

2

ERO started actions during the 3

rd

regulatory period to comply with its legal

assessment with the goal to reverse the impact from asset revaluation. This

introduced a substantial discontinuity with the regulatory framework set out in

the 3

rd

regulatory period:

2

Article 19a Energy act: (1) Pi regulaci cen penosu elektiny, pepravy plynu, distribuce

elektiny a distribuce plynu postupuje Energetick regulan ad tak, aby stanoven ceny

pokrvaly eln vynaloen nklady na zajitn spolehlivho, bezpenho a efektivnho vkonu

licencovan innosti, dle odpisy a pimen zisk zajiujc nvratnost realizovanch investic

do zazen sloucch k vkonu licencovan innosti [].

September 2013 | Frontier Economics 11

Regulation of energy network in Czech Republic

ERO proposed a change in the regulatory formula for the 3

rd

regulatory

period at the end of year 2012. The change was planned to come into force

in 2014, hence, during the 3

rd

regulatory period. ERO proposed the so called

Investment Debt Factor (IDF) which shall be applied for the period 2010-

2025 and would decrease allowed revenues on 2014 by accumulated

differences of investments and depreciation since 1.1.2010. ERO did not

implement this factor, because the Governments Legislative Council

dismissed this new parameter as retroactive and therefore incompatible with

the legislative order.

Instead ERO proposed in March 2013 to shorten the 3

rd

regulatory period

by one year and start with the 4

th

regulatory period as of 1.1.2014 (instead of

1.1.2015). In addition ERO proposed to reverse the revaluation of the assets

(step up) and to base the depreciation on the lower historic book values.

In August 2013 ERO when ERO dismissed its previous March intention to

shorten the 3

rd

regulatory period, they published a new proposal for the 4

th

regulatory period, which included some differences compared to the

regulatory formula for the 3

rd

regulatory period and the ERO proposal from

March 2013. It still includes the reversal of the step up from 2006.

However, it further includes

reduction of the WACC compared to March 2013;

introduction of the Network obsolescence factor, which is yet to be

specified;

introduction of a network utilisation factor, which is yet to be specified;

introduction of the so called investment fund which retrospective

claws back revenues from the companies.

2.3 EROs action and the regulatory climate

We understand that ERO is aware that the CZ gas and electricity network

companies are facing substantial investments in the future. Hence, it is still well

accepted by ERO that the companies need additional financial resources and a

reliable investment climate to implement their ambitious long-term investment

plans. A stable regulatory environment is the key prerequisite that companies can

and will raise capital at reasonable costs.

However, EROs actions during the 3

rd

regulatory period and the draft proposal

for the 4

th

regulatory period issued on August 2013 may have affected the

stability of the investment and regulatory climate for CZ energy network

companies by increasing the uncertainty on regulatory actions, on the future

12 Frontier Economics | September 2013

Regulation of energy network in Czech Republic

regulatory framework and the cost of capitals investors demand for providing

equity and debt for investments into energy networks.

September 2013 | Frontier Economics 13

Relationship between regulation and risk

3 Relationship between regulation and risk

In this section we explore the links between regulation, risk and return. It

describes the mechanisms through which regulation affects the risk faced by debt

and equity investors and considers the importance of regulation relative to other

risk factors for investors in utilities.

3.1 Channels for transmitting changes in risk to the

WACC

The cost of capital represents the minimum rate of return firms must pay in

order to attract capital from investors. As such, it is recognised widely as the rate

of profit that firms operating in a competitive market could be expected to earn.

The rate of return earned by firms in competitive markets could, in any given

year, deviate from the cost of capital. However, on average, firms in such markets

could be expected to cover their cost of capital.

The cost of capital needs to cover the risks (and opportunity costs) borne by

investors in the business. A return that just covers the cost of capital is therefore

commensurate with a normal economic return. Regulatory allowances of the

cost of capital aim to ensure that the firm can cover its expected financing needs

in order to undertake efficient investments and asset maintenance that sustain the

provision of services.

The cost of capital is typically measured by the Weighted Average Cost of Capital

(WACC). WACC has two basic components:

the cost of equity capital; and

the cost of debt capital.

The cost of equity is the expected rate of return required by investors in equity

that compensates them for the risk they bear, and the opportunities they forgo by

committing funds to the firm. The cost of debt measures the expected cost of

borrowing to the business. The WACC calculation weights these two

components according to the proportion of debt and equity capital within the

businesss financing structure, i.e. its gearing.

Changes in risk can affect equity investors and debt investors via different

channels. In order to understand the full implications of a regulatory change on

the cost of capital, it is necessary to understand the impact on the cost of equity

and the cost of debt separately.

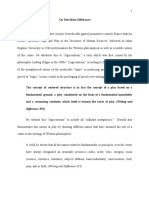

Figure 1 illustrates how a regulatory change could flow through to WACC by

altering a risk parameter within the cost of equity (beta) and/or a risk parameter

within the cost of debt (the debt premium).

14 Frontier Economics | September 2013

Relationship between regulation and risk

Figure 1. Channels for transmission of risk changes to the WACC

Source: Frontier Economics

The cost of equity to be used in the WACC formula is usually estimated using the

Capital Asset Pricing Model (CAPM). The CAPM formula to be applied for this

purpose is:

ost of euity iskfree rate eta uity risk remium

The risk-free rate represents the return on a completely riskless asset and is

generally proxied by the yield on government securities. The equity risk premium

measures the premium (over and above the risk-free rate) that investors might

expect to earn by investing in a fully diversified portfolio of all risky assets in the

economy (i.e. the market).

eta measures the resonsiveness of the comanys euity returns to

changes in overall market returns. It therefore captures the riskiness of the

equity invested in the given company. A change in regulatory circumstances that

alters the risk that equity investors expect to bear will feed through to the cost of

equity by causing the beta to change.

The cost of debt may be represented as follows:

ost of debt iskfree rate ebt remium

The debt premium reflects, among other things, the credit risk of a

comany. Any regulatory change that alters the riskiness of a comanys

debt will do so by altering the debt premium. A companys credit risk

depends, in part, on its capital structure (i.e. gearing level). In general, the higher

Change in risk resulting from a regulatory change

Cost of equity

Change in

beta?

Change in

cost of equity

Yes

Change in Weighted Average Cost of Capital

Change in debt

premium?

Cost of debt / leverage

Yes

Change in

cost of debt or

gearing

September 2013 | Frontier Economics 15

Relationship between regulation and risk

the level of gearing, the greater is the credit risk and, therefore, the higher is the

cost of debt.

In practice, a companys debt is observable directly, for example by examining

the yields on bonds issued by the firm. However, a companys cost of equity

cannot be observed in the same way. It needs to be estimated using asset pricing

models such as the CAPM.

3

The foundation of all asset pricing models is the risk-return trade-off, which says

that, all else being equal, the greater the risk borne by investors, the higher the

returns they expect in exchange for supplying capital.

3.2 Role of regulation in the cost of financing

This section considers how regulatory action, and regulatory design, can

influence the cost of capital by altering the risks faced by businesses. In this

regard, there are three distinctions to be made:

Firstly, the system of regulation may, itself, impose a certain risk profile on

companies. Relevant regulatory parameters may be length of regulatory

period, way how costs are determined (backward/forward looking), the

degree of incentives and/or uncertainty of cost recovery in the regulatory

system.

Secondly, regulatory actions, that either increase or lower uncertainty about

how the system of regulation will work in future, can alter the risks faced by

companies. This would include regulatory reform processes in relation to

future price control reviews.

Thirdly, the legal framework has an impact on the risk profile of companies

as it may limit the degree of freedom of regulators behaviours. This includes

how detailed rights and obligations of regulated companies are fixed in

primary and secondary energy legislation. Essential part of this is the appeal

process against regulatory actions which gives the regulated companies the

possibility to challenge regulatory decisions.

3.2.1 The system of regulation can influence risk and the cost of capital

A companys risk profile can be influenced by the nature of the regulatory system

it faces.

4

To help illustrate this concept we discuss the theoretical effect of two

3

Other asset pricing models considered by UK regulators include the Fama-French three-factor

model, and the Dividend Growth Model.

4

See, for example, Parker, D. (2003), Performance, risk and strategy in privatised, regulated

industries: The UKs experience, International Journal of Public Sector Management 16(1), 75 100;

Wright, S., Mason, R., Miles, D. (2003), A study into certain aspects of the cost of capital for

16 Frontier Economics | September 2013

Relationship between regulation and risk

alternative pure systems of regulation rate-of-return and price-cap on

firms cost of capital.

Rate-of-return regulation and price-cap regulation could be viewed as two

extremes of a spectrum of possible regulatory systems. Under pure price-cap

regulation, prices are set for a number of years, based on a forecast of efficient

costs. If a company manages to reduce costs below these forecast levels, it may

keep the profits from doing so for the remainder of the control period.

Therefore, price-cap regulation provides firms with incentives to improve

efficiency.

The efficiency incentives provided by a price-cap system exposes regulated firms

to cost outturns deviating from forecasts. In order to be compensated for this

risk, theoretically investors will demand a higher rate of return, which will be

reflected in a higher cost of capital. We note that empirical evidence may be in

contrast to this theoretical argument. For example, Frontier (2008/2011)

5

compared asset betas for energy network companies grouped in countries with

cost-plus and incentive-based regulation and could not find differences based on

statistical tests. There may be various reasons for this. In principle cost-plus and

incentive regimes applied are not pure systems, e.g. the incentive regimes include

also cost-pass through mechanism. In addition, even if cost-plus regulation is

applied, the companies will be exposed to regulatory scrutiny when setting

reasonable costs.

3.2.2 Regulatory action can alter the risk faced by companies

Apart from the broader regulatory system itself, the actual behaviour of the

regulator within a given system can influence the risks borne by the regulated

firm and investors. There are a number of reasons why regulatory risk can be

correlated with market risk. In periods of unfavourable economic conditions,

regulators might be less inclined to raise allowed rates of return for regulated

firms in order to avoid increasing the burden on consumers.

6

This would cause

regulatory actions to be correlated with general macroeconomic conditions. This

regulated utilities in the U.K., a Smith & Co. Ltd. report to the OFT and U.K. economic regulators.;

Guthrie, G. (2006), Regulating infrastructure: the impact of risk and investment, Journal of Economic

Literature XLIV, 925972.

5

Frontier Economics, Ermittlung des Zuschlages zur Abdeckung netzbetriebsspezifischer Wagnisse im Bereich

Strom und Gas, Report for Bundesnetzagentur, 2008; Frontier Economics, Wissenschaftliches Gutachten

zur Ermittlung des Zuschlages zur Abdeckung netzbetriebsspezifischer unternehmerischer Wagnisse im Bereich Gas,

Report for Bundesnetzagentur, 2011.

6

In fact, an asymmetry may arise because pressure from consumer groups and industrial customers

may make it difficult for regulators to raise prices in bad times, and the regulator could justify

disallowances of price increase.

September 2013 | Frontier Economics 17

Relationship between regulation and risk

in turn would mean that the effect of regulatory decisions will be difficult to

diversify, so such changes will affect the cost of capital.

7

In relation to the impact of regulatory actions on company risk, it is useful to

distinguish between two categories for regulatory action.

First, predictable regulatory changes can increase the correlation of the

regulated firm with market risk. This is not necessarily a source of harm for

society. For example, regulatory action that introduces competition into a

sector may increase the risks faced by firms regulated within that sector, but

the change may nevertheless raise overall welfare to society.

Second, regulatory action can create uncertainty about how the system will

work in future. This is potentially more harmful to society. Unpredictable

regulatory conduct can create uncertainty for firms and, ultimately, for

investors. Depending on the source and nature of the uncertainty, this could

raise the firms cost of capital.

Several empirical studies find significant effects of regulation on the regulated

firms cost of capital. Trout (1996)

8

, Archer (1981)

9

and Dubin and Navarro

(1982)

10

compared utilities in different US states, to investigate the effect of

variations in state-level regulations on the cost of capital. All these studies find

that regulatory climate has a significant effect on the cost of capital.

Uncertainty over the future expected behaviour of the regulator can also affect

the cost of capital for the regulated firm. A number of studies have examined the

effect of regulatory uncertainty. Buckland and Fraser (2001) studied the impact of

the 1992 UK general election on the betas of 12 regional electricity companies,

which were privatised in 1990. The Conservative victory at those elections was

one of the more unexpected results during the 20

th

century and in the month

leading up to the election on 10 April, speculation of a Labour victory was

intense. Buckland and Fraser found statistically-significant evidence of the betas

of the Regional Electricity Companies (RECs) rising significantly during this

period, peaking on the day of the election, in anticipation of stricter regulation to

come. This would have had the effect of raising the RECs costs of capital, all

else being equal.

7

Burkhard, p., 2010. Regulatory risk and the cost of capital. Determinants and implications for rate

regulation. Springer Berlin- Heidelberg 2010. Pp. 37.

8

Trout, R., R., 1979. The regulatory factor and electric utility common stock investment values.

Public Utilities Fortnightly, November 22 1979, pp.28-31.

9

Archer, S., H., 1981. The regulatory effects on cost of capital in electric utilities. Public Utilities

Fortnightly, February 26 1989, pp. 36-9.

10

Dubin, J., A., and Navarro, P., 1982. Regulatory climate and the cost of capital. In: regulatory

reform and public utilities, ed. By Michael A. Crew, Boston/Dordrecht/London 1982, 141-66.

18 Frontier Economics | September 2013

Relationship between regulation and risk

3.2.3 Legal certainty, appeal process, regulated companies and regulatory

action

The possibility for regulated companies to legally appeal a regulatory decision,

with which they disagree, may influence the behaviour of regulators in two ways:

Ex ante limitation The threat of a potential legal appeal may force the

regulator to put more emphasis on reasoning its decisions. For example, this

may result in a transparent consultation/decision process, where regulated

companies and/or other stakeholders have the possibility to comment the

regulators proposals.

Ex post limitation In principle the regulatory process is a balancing of

various and sometime conflicting interests. In some cases the regulatory

action may overemphasize one interest or is supposed not compliant with

the law. Hence, the legal appeal institution has the task to decide on the

legitimacy of the regulatory action and will approve or disapprove it ex post.

We note that the degree of the ex ante and ex post limitation depends on various

factors in relation to the legal appeal process:

Rules defining the regulatory framework detailed rules for setting the

regulatory components will more easily allow assessing the compliance

of regulatory decisions with the law.

11

Clear structure of legal appeal institutions allows all stakeholders to know

the respective legal enforcement institution. In addition the legal

character of the regulatory decision should comply with the principle

legal appeal process, e.g. in some countries a regulatory contract may

not fit into legal appeal process; and

Track record of legal appeal institutions the legal appeal institution should

have a track record (credibility) to decide in time and with a balanced

view for all stakeholders. This is important as companies will only use

the costly legal appeal process if they can expect a positive decision

in their case. In particular, the credibility of the legal appeal institution

has an important impact on the ex ante limitation of regulatory actions.

Only if the regulator expects an overruling of her decision, she will take

into account the expected opinion of the legal appeal institution.

11

However, we note that detailed rules may have an adverse effect on risk, as well. This is the case if a

change in the economic environment of regulated companies, e.g. increase in investment need due

to connection of renewables, requires flexible regulatory actions.

September 2013 | Frontier Economics 19

Relationship between regulation and risk

3.3 Regulation and risk the view from rating

agencies

The regulation/risk exposure of regulated companies to the capital market can be

reflected by the rating methodologies published by credit rating agencies. The

level of risk embedded in companies regulatory framework plays a crucial role in

these methodologies and differentiates the regulated sector from most other

corporate sectors.

In the following we illustrate Moodys rating methodology for regulated electric

and gas networks

12

, which hinges on four rating factors with different weights on

the final result:

Regulatory environment and asset ownership model, which reflect

the companys expected ability to recover cost in a consistent manner

over time;

Operational characteristics and asset risk, which reflects the

companys capacity to carry out its investment plan;

Stability of business model and financial structure, which capture

the exposure of lenders from the company engaging in new or

unregulated activities; and

Key credit metrics, which account for the financial parameters that

best reflects the likelihood of default.

The four rating factors are further categorised into sub-factors illustrated in

Table 3 again with different weights on the final result.

12

Moodys Investors Service, Rating Methodology Regulated Electric and Gas Networks, 2009. However,

we note that Standard&Poors and Fitch are using similar financial indicators.

20 Frontier Economics | September 2013

Relationship between regulation and risk

Table 3. Moody's methodology for rating regulated electricity and gas networks

Broad Rating Factors Broad Rating

Factor

Weighting

Rating Sub-Factor Sub-

Factor

Weighting

1. Regulatory environment

and asset ownership model

40% Stability and Predictability of

Regulatory Regime

15%

Asset Ownership Model 10%

Cost and Investment Recovery 10%

Revenue Risk 5%

2. Efficiency and execution

risk

10% Cost Efficiency 6%

Scale and Complexity of Capital

Programme

4%

3. Stability of business model

and financial structure

10% Ability and Willingness to Pursue

Opportunistic Corporate Activity

3.33%

Ability and Willingness to Increase

Leverage

3.33%

Targeted Proportion of Operating

Profit Outside Core Regulated

Activities

3.33%

4. Key credit metrics 40% Adjusted ICR (or FFO Interest Cover) 15%

Net Debt/RAV 15%

FFO/Net Debt 5%

RCF/Capex 5%

Source: Moody's

In the following we focus on the sub-factors which correspond to our discussion

on the role of regulation in the cost of financing in Section 3.2.

Stability and Predictability of Regulatory Regime (15%) Reflects the

characteristics of the regulatory environment in which a network operates.

This includes the transparency of the regulatory framework, the regulators

track record for predictability and stability in terms of decisions making and

its independence from politics. In addition this sub-factor takes into account

the overall robustness of institutions and the rule of law in relevant

jurisdiction. Hence, this sub-factor corresponds with the discussion on

regulatory action and risk (Section 3.2.2) and the possibility of the legal

appeal process (Section 3.2.3).

September 2013 | Frontier Economics 21

Relationship between regulation and risk

Cost and Investment Recovery (10%) Focuses on the supportiveness of

the regulatory system on cost recovery with regard to operating and capital

expenditures. For example this includes the degree of incentives on costs,

the degree and timing of the cost-pass through mechanism, etc. In other

words, it measures the risk allocation between the company and its

customers. Hence, this sub-factor corresponds with the discussion on the

system of regulation (Section 3.2.1).

Revenue Risk (5%) Refers to the mechanism of revenue generation by

the company, in more detail on the volumes transported by a network as a

driver of potential volatility and uncertainty of future revenues. The

regulatory framework can mitigate this risk e.g. by introducing tariffs based

on capacities (which tend to be more stable) instead of volume or a revenue

cap. Hence, this sub-factor corresponds with the discussion on the system

of regulation (Section 3.2.1).

As the three sub-factors discussed above make up 35% of the overall assessment

the effect on the credit rating by an up-/downgrade will be substantial. In

addition, it is straightforward that the factor Cost and Investment Recovery and

Revenue Risk will affect other rating factors, e.g. Key credit metrics by influencing the

cash flow profile of the regulated companies.

22 Frontier Economics | September 2013

Relationship between regulation and risk

3.4 Key findings Regulation and risk

Changes in risk will affect equity investors and debt investors via

different channels. Risk will feed into the

cost of equity via the beta; and

cost of debt via the debt premium.

Regulatory actions and regulatory design will influence the cost of capital by

altering the risks faced by businesses.

We identified three sources of potential regulatory influence and

categorised them to three Moodys key credit rating indicators reflecting

the regulatory environment:

Stability and Predictability of Regulatory Regime;

Cost and Investment Recovery; and

Revenue Risk.

Regulatory systems can be compared by analysing how they perform

against these indicators and how this may influence business risks

influence the beta and debt premium.

September 2013 | Frontier Economics 23

Regulation and risk selected European

countries

4 Regulation and risk selected European

countries

In the following we describe and analyse selected European countries with regard

to the

Stability and Predictability of Regulatory Regime;

Cost and Investment Recovery; and

Revenue Risk.

In addition we illustrate the allowed cost of capital (WACC) for these countries.

The European countries we selected are:

UK Introduced a new regulatory framework, RIIO

13

, for the electricity and

gas networks. The first application of RIIO for the UK gas distribution

companies came into force on 1 April 2013. The main changes from RIIO

on the companies are the extension of the regulatory period from 5 to 8

years (RIIO-G1 for gas distribution companies is from 1 April 2013 to 31

March 2021) and the strong focus on providing outputs. Hence, UK

provides as an example of a recent regulatory decision applying a new

regulatory framework.

Germany Started the 2

nd

regulatory period for gas distribution companies

with 1 January 2013. As the main principles of the regulatory framework are

set out in law the 2

nd

regulatory period is mainly an extension of the revenue

cap framework from the 1

st

regulatory period. However, with regard to the

cost of capital the regulator decided to deviate from the more mechanistic

approach used in the 1

st

regulatory period to a more flexible one in favour of

the regulated companies. Hence, Germany provides as an example of a

recent regulatory decision, as well.

France Started the 4

th

regulatory period for gas distribution companies

with 1 July 2012. The regulation in France is characterised by a combination

of incentive regulation for operating expenditures and cost-plus regulation

for investments. In addition the regulation includes incentive-based

mechanism for certain output objectives, e.g. promotion of gas use and

quality of service. Hence, France provides as an example of a regulatory

framework compared to UK and Germany with a lower degree of

incentives.

13

RIIO stand for Revenues = Incentives + Innovation + Outputs.

24 Frontier Economics | September 2013

Regulation and risk selected European

countries

We make the following disclaimer in relation to the below stated Moodys

assessment for gas distribution companies in Germany and France:

France The assessment of Moodys rating is taken out from the rating of

the French gas TSO, TIGF

14

. Although TIGF being a gas TSO we assume a

similar assessment with regard to gas distribution networks, as the same

regulatory principles are applied.

Germany The assessment of Moodys rating is taken from the rating of

HSE Netz AG

15

, which owns and operates gas and electricity distribution

networks. Although HSE Netz AG operates gas and distribution networks

we assume a similar assessment with regard to gas distribution networks

only, as the same regulatory principles are applied for gas and electricity

networks.

4.1 UK

16

4.1.1 Stability and Predictability of Regulatory Regime

Regulation in UK for electricity and gas networks has a track-record of more

than 20 years. The process of price control for a regulatory period is transparent

and lasts between 18 months to 2 years. During this period the regulator, Ofgem,

obtains information from the companies and consults on the methodology that

will be used to set the price control. Ofgem publishes a draft determination,

which is also open to consultation, and then presents the company with a final

determination of the tariff control for the next regulatory period.

When reaching the determination, Ofgem must ensure that it is consistent with

her legal duties. Specifically, the regulator has a primary duty to protect the

interests of consumers and a number of secondary duties including the need to

secure that licence holders are able to finance the activities which are the subject

of obligations imposed

17

.

Once presented with the final determination, a company has a pre-specified

period of time to decide whether to accept Ofgems decision. If the decision is

accepted, the companys licence is modified to reflect the new tariff. If the

14

Moodys, Credit Opinion: TIGF SA, August 2013.

15

Moodys, Credit Opinion: HSE Netz AG, August 2013.

16

We note that this section refers to gas (and electricity) networks regulated by Ofgem. These are the

networks in England, Wales and Scotland. The networks in Northern Ireland are not included as

they are regulated by the Northern Ireland energy regulator (UR).

17

Utilities Act 2000.

September 2013 | Frontier Economics 25

Regulation and risk selected European

countries

decision is not accepted within the specified time period, Ofgem refers the case

to the Competition Commission (the appeals body in UK).

The conditions under which a company can reject the regulators decision and

thereby seek an appeal are laid out in legislation. Formally, the company will

reject the proposed tariff if it is unable to finance the proper carrying out of its

function. That is, the company can reject the decision if it believes that the

revenues allowed by the regulator are not sufficient to cover the costs of

delivering required outputs.

If a company rejects Ofgems proposal the case is referred to the Competition

Commission (CC). The duties of the CC are laid out in the legislation relevant to

the particular sector (The Utilities Act 2000 in the case of energy). In addition,

the companies have the possibility to make a legal appeal to the High Court.

However, since the beginning of regulation no company has rejected Ofgems

proposal. The CC is also responsible for the decisions from the Northern Ireland

energy regulator (UR). There was a recent case where a company rejected the

decision from UR, in which CC analysed the impact from regulatory actions on

risk and the cost of capital (see box below).

In November 2008 Ofgem started its review of the then regulatory approach

(RPI-X@20). The main task was to incentivise networks to support sustainability

objectives and sector decarbonisation, while maintaining high quality of service

and low costs. RPI-X@20 included an extensive consultation and interaction

process with all stakeholders. The goal of this process was increase the

transparency on the objectives of all relevant stakeholders and to include them in

the new approach. In addition, the consultation was meant to specify the new

regulatory measures proposed. The process resulted in the new regulatory

approach RIIO Revenue set with Incentives for delivering Innovation and

Outputs in October 2010. Its key innovation is the central focus on outputs,

not inputs. The principle is simple. Customers care primarily about the end result

and so this is what network operators should be incentivised to provide. In 2013

RIIO was first applied to the gas distribution companies (RIIO-GD1), electricity

and gas transmission companies (RIIO-T1).

26 Frontier Economics | September 2013

Regulation and risk selected European

countries

Competition Commission Phoenix Natural Gas

In February 2012 Phoenix Natural Gas Limited (PNGL) rejected the price

control proposed by the Northern Ireland energy regulator (UR). UR

subsequently referred the price control to the CC investigate whether the price

control conditions operated against the public interest. The dispute was focussed

on URs proposal to write off approximately 25% of PNGLs regulated asset

base (RAB).

PNGL argued that this proposal was unexpected, unjustified, and contrary to the

principles of incentive regulation, since it retrospectively altered the previously

agreed value of PNGLs asset base. UR argued that it was acting in line with

regulatory practice, and protecting the interests of customers, by removing

unspent allowances from the asset base after 5 years.

The CC

18

found that URs proposal had not been adequately signalled and that

the rationale for it was not sufficiently well communicated or understood.

Changes to the regulatory framework that were enacted in this way would lead to a

perception of regulatory uncertainty, as investors may assume that URs future actions could be

unpredictable.Investors may anticipate that in addition to normal commercial risks there

could be greater uncertainty in the future about the regulatory environment, and thus increased

risks that returns on investment will not be realized in the way or to the extent that is expected.

This is likely adversely to affect investment decisions in the future.

The CC identified the ways in which customers could be harmed by retrospective

interventions in the long-run. It highlighted three possible mechanisms by which

the willingness to invest and the cost of finance could be adversely affected by URs

proposals:

The credit ratings agencies may view the regulatory regime as less favourable and, as

a result, may demand higher credit metrics for a given credit rating, which may lead to a

downgrade of a companys debt. This may have the effect of decreasing the amount of debt

that a company can have in its capital structure and/or increasing the cost of the

companys debt, both of which could lead to an increase in the overall WACC.

Equity investors may consider that the regulatory regime is less attractive,

and as a result may increase the return that they require for investing in a given project.

This may have the effect of increasing the required rate of return.

Finally, a perception of regulatory uncertainty may deter investment if companies

are unable to form judgements or are very uncertain of what the regulatory environment will be

and if, how or when they will receive a return on investments.

18

Competition Commission, Phoenix Natural Gas Limited price determination, November 2012.

September 2013 | Frontier Economics 27

Regulation and risk selected European

countries

Therefore, the CC considered that regulatory uncertainty would affect both the

cost of debt and the cost of equity. It stated that any effects on the cost of equity could

be long-lived because the investment community may be expected to take into account URs

track record over a relatively long time period when investing in infrastructure assets with a

similarly long life. [para 8.94]

The CC did not quantify the scale of the impact of regulatory uncertainty on the

cost of capital. Nevertheless it concluded that it is our judgement that these effects

could be significant. As an illustrative example, applying a 50 basis point uplift to the cost of

capital to NIEs and PNGLs combined RABs of approximately 1.8 billion would equal

9 million a year. This does not take into account any effects on other regulated investments

and on future greenfield investments. [para 8.99]

Moodys assessment Stability and Predictability of Regulatory

Regime with Aaa rating

With regards to Stability and Predictability of Regulatory Regime Moodys uses the UK

regulatory framework as the benchmark and applies an Aaa rating.

In particular Moodys placed special attention to the Ofgem project RPI-X@20

started in 2008, which evaluated Ofgems past regulatory approach for future

application. This process finally resulted in the new RIIO regime.

In October 2010 Moodys raised its concern about Ofgems announcement that

the new regulatory model RIIO is the biggest change to the regulatory

framework for 20 years. Moodys was concerned that the regulators track

record for stability and predictability could be quickly undone.

Moodys welcomes this review and recognises that the challenges facing network companies

are clearly evolving against the backdrop of the changing way in which energy is likely to

be delivered in the future. The current regulatory framework for energy companies was

developed when they were purely infrastructure companies with a somewhat fixed role in

the industry. This is no longer the case and network companies will clearly need to evolve

to meet new technological challenges. However, the UK regulatory framework and, in

particular the RPI-X concept, has been adopted all over the world and is held in high

regard for its predictability, support and good track record. Moodys scores the UK

regulatory framework for the energy sector as one of the most transparent in the world.

Therefore, any material change to the regime could potentially weaken that view until a

good track record of performance has been re-established. We also note that a changing

regulatory framework and new processes may represent a significant management

challenge for companies, particularly in the first few years.

19

19

Moodys (2010: 3).

28 Frontier Economics | September 2013

Regulation and risk selected European

countries

However, after the first application of RIIO to the UK gas distribution

companies (RIIO-GD1), electricity and gas transmission companies (RIIO-T1)

Moodys notes that

RIIO is more a rebranding of the previous RPI-X regime and represents a natural

evolution in regulation that has continued since the utilities were first privatised.

20

Due to the evolutionary development from RPI-X to RIIO Moodys assessed

that the transition to RIIO for the gas distribution companies has no impact on

the Aaa rating.

20

Moodys (2013: 1).

September 2013 | Frontier Economics 29

Regulation and risk selected European

countries

4.1.2 Regulatory system Cost and Investment Recovery and Revenue

Risk

Table 4. Regulatory parameters RIIO-GD1

Regulatory component Description

Type of regulation Revenue cap regulation

Length of price control 8 years (mid-period review)

Opex Split in to

Controllable costs (subject to efficiency analysis) ;and

Non-controllable costs.

RAB RAB is based on

Asset value of end year of previous period (rolled forward);

Annual net additions to RAB (fixed percentage of Totex)

Cost of capital WACC approach

Real WACC

Depreciation Sum-of-year digits (front loading)

Depreciation based on asset live of 45 years (sum-of-digits)

Investment Business plans serve as basis for RAB growth rate of 1%/a

Efficiency analysis Totex benchmarking based on four models (average efficiency):

Historical Totex;

Forecast Totex;

Historical disaggregated activity level expenditure; and

Forecast disaggregated activity level expenditure.

DSOs have to close 75% of their assessed gap between the cost forecast

and the upper quartile (75%-quartile).

Treatment of network

losses

DSOs are expected to improve gas transport losses over RIIO-GD1 through

rolling incentive mechanism

Companies receive forecast allowance for shrinkage based on actual

volumes and forecasted prices

Ex post alignment between forecast and outturn prices, therefore no

commodity price risk for operators

Incentives Incentive rates in cost allowances

IQI (Information Quality Incentive) provides ex-ante incentives to

submit accurate cost forecasts. Companies receive bonus if

submitted business plan is closely aligned to Ofgems forecast.

Innovation stimulus packages

Source: Frontier

30 Frontier Economics | September 2013

Regulation and risk selected European

countries

The key element of the new RIIO framework is represented by an output

oriented, instead of in input-oriented, definition of cost-allowances. Under RIIO,

companies are required to submit business plans setting out future investment

plans and define how the set of outputs will be achieved. Those plans serve as

key input in setting the price control elements. Figure 2 shows the principal

outputs under RIIO GD1 which can be allocated to different output categories.

Figure 2. Principal outputs under RIIO GD1

Source: Frontier

The biggest expenditure item under RIIO GD1 is represented by replacement

expenditure

21

(repex) which is an obligation derived from UKs Health&Safety

Executive that requires gas distribution companies to replace iron mains located

within 30 meters of buildings within 30 years (30/30 program).

In order to overcome the inherent principal-agent problem that lies within

business plans as source of information being submitted by regulated companies,

Ofgem introduced mechanisms (Information quality incentive, IQI) that aim at

incentivising the operators to submit accurate plans and reveal their true costs:

Incentive rates for outperformance IQI allows companies to retain part

of cost outperformance during a regulation period. The incentive rate has

been set between 65% and 70%, allowing companies to retain two thirds of

the achieved cost outperformance.

21

Ofgem changed the capitalisation principles for repex and introduced a stepped transition for repex

capitalisation, from 50% capitalisation in 2013-14 to 100% in 2020-21.

Principal outputs in RIIO GD1 (extract)

Percentage of biomethane capacity

connected

15-20% reduction of gas transport

losses

Reduction of carbon footprint

satisfactory survey, complaints metrics,

stakeholder engagement

Connection of 80,000 energy poor

households

Increase public awareness for carbon

monoxide

Maintain connection standards

New connection standards for gas

entry costumers

Reduce safety risks by 40-60%

Compliance with statutory

requirements

Expected number of interruptions

Asset load / Capacity utilisation

Maintaining operation performance

Environ-

ment

Customer

service

Social

obligation

Customer

connection

Safety Reliability

September 2013 | Frontier Economics 31

Regulation and risk selected European

countries

Reward for accuracy in business plans Cost rewards are granted

(penalties charged) of maximal 2.5% of total expenditure for companies that

provide costs forecasts equivalent to Ofgems assessment of efficient costs.

As to provide further incentive to innovate, RIIO GD1 includes an innovation

stimulus package to fund innovation.

Further, the submitted business plans are subject to a comparative efficiency

analysis based on four cost measures of total expenditure, two based on historical

costs and two based on forward looking cost assessment. The average over all

four measures serves as base line cost allowance. Companies will have to close

75% of the assessed gap between their forecast and the efficient costs

22

.

Moodys assessment Cost and Investment Recovery with A rating

and Revenue Risk with Aaa rating

With regards to Cost and Investment Recovery Moodys still applies an A rating on the

gas distribution companies after the first application of RIIO. The main reasons

are:

the extension of the price control period from five to eight years is a key

change of RIIO as there is the potential for companies having to wait

longer for prices to be reset if specific costs increase. However,

Moodys notes that this risk is largely mitigated by the number of

uncertainty mechanisms (such as true-ups and the move to a cost of

debt index) included;

the nature of the allowed expenditure is very much in line with the

existing price control and represents business as usual for the

companies;

the companies will face a similar risk due to cost performance under

RIIO-GD1; as well as

Moodys is of the opinion that the presence of new incentives in

relation to outputs is more than offset by the new uncertainty

mechanisms with regards to costs, hence, making the overall credit risk

balance broadly neutral for RIIO-GD1.

With regards to Revenue Risk Moodys applies an Aaa rating. This is due to the

structure of the tariffs as fixed capacity charges make up a big proportion of the

overall revenue in gas and that the companies are not exposed to volume

risks.

22

Efficient costs are defined as the upper quartile (75%) of efficiency scores.

32 Frontier Economics | September 2013

Regulation and risk selected European

countries

Moodys rating for Cost and Investment Recovery and Revenue Risk under RIIO

indicates a low risk exposure for gas distribution companies with regard to these

factors which will feed into the overall credit rating assessment.

4.1.3 WACC

Table 5. WACC parameter UK

Parameter Parameter value

Risk-free rate (real) 2.0%

Asset-Beta 0.38

Equity-Beta 0.9

Market risk premium 5.25%

Cost of equity (real, post-tax) 6.7%

Gearing 65.0%

Tax 21.0%

Debt premium 0.9%

Cost of debt (iBoxx 10-year simple trailing

average index) (real, pre-tax)

2.9%

Inflation rate 3.1%

WACC (real, vanilla) 4.2%

Source: Frontier

Ofgem used the Capital Asset Pricing Model (CAPM) including a relative risk

analysis to determine the cost of equity for RIIO-GD1. Compared to the

previous price control regime (gas distribution price review - GDPCR1), Ofgem

decided to lower the equity beta from 1 to 0.9 based on the argument that gas

distribution network operators face lower risks than in GDPCR1. The equity

beta of 0.9 translates into an asset beta of 0.38. Further, Ofgem reduced the real

risk-free rate from 2.5% to 2% and increased the market risk premium from

4.75% by 0.5% pp to 5.25%.

Under the RIIO model Ofgem decided to base the cost of debt on a long-term

trailing average of forward interest rates, and the revenues allowed under the

price control will be adjusted each year for changes in this trailing average.

Ofgem notes that the allowed return on debt in price controls before RIIO has

closely tracked the long-term cost of debt average rather than current rates. This

is a strong indication that long-term averages remain an appropriate basis for

calculating the cost of debt going forward irrespective of current (or indeed

September 2013 | Frontier Economics 33

Regulation and risk selected European

countries

forecast) market rates.

23

Hence, this approach should allow cost recovery for cost

of debt in the long run.

For RIIO-GD1 Ofgem decided to use a trailing 10-year average of two iBoxx

indices for the cost of debt. The respective iBoxx indices are the

iBoxx Non-Financials A 10+

24

This index includes bonds with a an

average remaining time to maturity (weighted by outstanding amount) of

21.6 years for A rated companies.

iBoxx Non-Financials BBB 10+

25

This index includes bond with a an

average remaining time to maturity (weighted by outstanding amount) of

17.2 years for BBB rated companies.

The unweighted average of both indices is then deflated by using a break-even

inflation figure. The break-even inflation figure is derived from the yield from

British Government Securities 10 year real and nominal zero coupons.

26

Ofgem

does not explicitly display the debt premium. However, using the risk-free rate

and the cost of debt implies a debt premium of 0.9 % at the beginning of RIIO-

G1.

4.2 Germany

4.2.1 Stability and Predictability of Regulatory Regime

The regulatory framework for incentive regulation for gas and electricity

networks is set out in the Incentive regulation decree (Anreizregulierungsverordnung

2012, ARegV). In addition the Gas network tariffs decree

(Gasnetzentgeltverordnung, GasNEV) defines how the costs are determined

to set the network tariffs for gas transmission system operators (TSO) and

distribution system operator (DSO) companies. These decrees include e.g.

regulatory formula;

size of productivity factors; or

calculation of allowed depreciation, asset values and cost of equity

and limit the actions from the regulator, Bundesnetzagentur (BNetzA).

23

See Ofgem, RIIO Handbook, 2010.

24

Series reference: DE000A0JY837.

25

Series reference: DE000A0JZAH1.

26

10 year nominal zero coupon, series reference IUDMNZC; 10 year real zero coupon, series

reference IUDMRZC.