Vous aimerez peut-être aussi

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

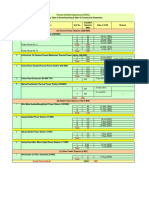

- 100 KWP Solar Power Plant Technical Proposal PDFDocument24 pages100 KWP Solar Power Plant Technical Proposal PDFRabindra SinghPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hydrogen Fuel Engine-Ppt AbstractDocument7 pagesHydrogen Fuel Engine-Ppt AbstractVijay RaghavanPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Comparison Between Traditional and Modern Fuel VehiclesDocument16 pagesComparison Between Traditional and Modern Fuel VehiclesNaina AgrawalPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Heating and Cooling With Geothermal EnergyDocument34 pagesHeating and Cooling With Geothermal EnergyJuan Carlos Sanchez FloresPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- 01 - Introduction To PV Systems - NEWDocument35 pages01 - Introduction To PV Systems - NEWnoudjuhPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Akshay UrjaDocument56 pagesAkshay UrjasilverbirddudePas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Solar Fans PDFDocument3 pagesSolar Fans PDFMohammed ShakilPas encore d'évaluation

- Sources of EnergyDocument2 pagesSources of EnergyglechohPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Solar Photovoltaic System DesignDocument9 pagesSolar Photovoltaic System DesignJay RanvirPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Solar Energy and ApplicationsDocument20 pagesSolar Energy and ApplicationsSanath ReddyPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Total 200: Present Installed Capacity of CSPGCLDocument1 pageTotal 200: Present Installed Capacity of CSPGCLajjuPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Renewable Energy Sources in FiguresDocument88 pagesRenewable Energy Sources in FiguresJayson LauPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Review of Related LiteratureDocument4 pagesReview of Related LiteratureMaria Blessie Navarrete100% (1)

- Proposed PV System Electricity Generation and Electricity RateDocument3 pagesProposed PV System Electricity Generation and Electricity RateSangeet BhandariPas encore d'évaluation

- Wind Energy and Wind Turbine PDFDocument13 pagesWind Energy and Wind Turbine PDFE Cos LopezPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- ModelQuestions EEE305Document2 pagesModelQuestions EEE305John TauloPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Exergetic Analysis of A New Design Photovoltaic and Thermal (PV/T) SystemDocument5 pagesExergetic Analysis of A New Design Photovoltaic and Thermal (PV/T) SystemBranislavPetrovicPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Non Conventional Energy ResourcesDocument27 pagesOn Non Conventional Energy ResourcesPhani Kiran83% (6)

- No. 1/2006 - Vol. 25Document68 pagesNo. 1/2006 - Vol. 25vdmoorthy123Pas encore d'évaluation

- Environmental Controls I/IG Environmental Controls I/IGDocument28 pagesEnvironmental Controls I/IG Environmental Controls I/IGRUSHALI SRIVASTAVAPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- USGeothermal Education&Training Guide Oct2010Document15 pagesUSGeothermal Education&Training Guide Oct2010Ardhymanto Am.TanjungPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- U.S. Solar Market Insight: Executive SummaryDocument22 pagesU.S. Solar Market Insight: Executive SummaryScott WhitePas encore d'évaluation

- Questions You Might Be Afraid To Ask About Off Grid Solar SystemDocument2 pagesQuestions You Might Be Afraid To Ask About Off Grid Solar Systema0ftrou651Pas encore d'évaluation

- Lehigh Solar Business LetterDocument2 pagesLehigh Solar Business Letterapi-329298798Pas encore d'évaluation

- Mrhkli: Beam Pro Training and ExaminationDocument68 pagesMrhkli: Beam Pro Training and ExaminationSimon LawPas encore d'évaluation

- New Microsoft Word DocumentDocument4 pagesNew Microsoft Word DocumentAshwini KumarPas encore d'évaluation

- Monocrystalline - 50Wp - 200Wp: 50W - 200W 17.20V - 30.10V 27.5A - 7.85A 21.10V - 36.10V 2.95A - 8.34ADocument2 pagesMonocrystalline - 50Wp - 200Wp: 50W - 200W 17.20V - 30.10V 27.5A - 7.85A 21.10V - 36.10V 2.95A - 8.34AsuryarisPas encore d'évaluation

- TNB HANDBOOK A4 - FinalDocument104 pagesTNB HANDBOOK A4 - FinalSharin Bin Ab GhaniPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- SOC 3101: Society, Technology and Engineering Ethics: Lecture On Renewable EnergyDocument10 pagesSOC 3101: Society, Technology and Engineering Ethics: Lecture On Renewable EnergyMd. Sahriar SabbirPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)