Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

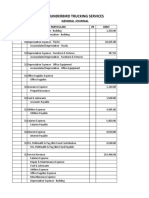

- Fixed Asset Accounting, Steven Bragg (2011)Document348 pagesFixed Asset Accounting, Steven Bragg (2011)Chaitaly R.100% (3)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Practice Set OwnDocument51 pagesPractice Set OwnAngela Dane Javier100% (1)

- McVitie's Digestive BiscuitsDocument28 pagesMcVitie's Digestive BiscuitsAnkit Goyal14% (7)

- Exploring Economics 6th Edition Sexton Test BankDocument77 pagesExploring Economics 6th Edition Sexton Test Bankcharlesdrakejth100% (31)

- Blackbook M&aDocument74 pagesBlackbook M&aSiddhartha100% (1)

- Assignment For Topic 01-01: Productivity and CostDocument3 pagesAssignment For Topic 01-01: Productivity and Costsyed aliPas encore d'évaluation

- MM Tables in Sap MMDocument59 pagesMM Tables in Sap MMIshan Patel100% (1)

- Operation ProjectDocument15 pagesOperation ProjectJaveria UmarPas encore d'évaluation

- To What Extent Does Demographic Growth Represent More of An Opportunity That A Threat To UK BusinessDocument3 pagesTo What Extent Does Demographic Growth Represent More of An Opportunity That A Threat To UK BusinessYazdan JafriPas encore d'évaluation

- Valuation of Merger ProposalDocument21 pagesValuation of Merger ProposalKARISHMAATA2100% (2)

- Ch14 - Parkin - Econ - Lecture PresentationDocument34 pagesCh14 - Parkin - Econ - Lecture PresentationSu Sint Sint HtwayPas encore d'évaluation

- References QuantiDocument2 pagesReferences Quantikarel Grace ColotPas encore d'évaluation

- Prof. Dr. Islam El Nakib: Submitted ToDocument2 pagesProf. Dr. Islam El Nakib: Submitted ToAhmed abd.elbasetPas encore d'évaluation

- PENgarap-FS RedjDocument43 pagesPENgarap-FS RedjAndrea AtonducanPas encore d'évaluation

- WEEK6 - Conducting A Feasibility StudyDocument31 pagesWEEK6 - Conducting A Feasibility StudyHannah Shiela MendozaPas encore d'évaluation

- ICT3642 - Assignment 4 - 2022Document8 pagesICT3642 - Assignment 4 - 2022Sibusiso NgwenyaPas encore d'évaluation

- Chapter 3 Understanding BuyersDocument34 pagesChapter 3 Understanding BuyersSally GarasPas encore d'évaluation

- Vanishing Games Corporation VGC Operates A Massively Multiplayer Online GameDocument1 pageVanishing Games Corporation VGC Operates A Massively Multiplayer Online GameTaimour HassanPas encore d'évaluation

- Consumer and Producer Surplus: Efficiency and Deadweight LossDocument11 pagesConsumer and Producer Surplus: Efficiency and Deadweight LossManideep DoddaPas encore d'évaluation

- Syllabus MBA JISU Final PDFDocument51 pagesSyllabus MBA JISU Final PDFNaredla Suman KumarPas encore d'évaluation

- Share Companies - Nature and FormationDocument34 pagesShare Companies - Nature and FormationKedir MuhammadPas encore d'évaluation

- Week 2-Basic Cost ManagementDocument21 pagesWeek 2-Basic Cost ManagementRichard Oliver CortezPas encore d'évaluation

- 50Document3 pages50sv03Pas encore d'évaluation

- Chapter 13 Postponement BenettonDocument7 pagesChapter 13 Postponement BenettonAbhishek PadhyePas encore d'évaluation

- Operation and Prodn MGMTDocument150 pagesOperation and Prodn MGMTSurafel KebeeePas encore d'évaluation

- Cost ST - 1 2018 (Solu)Document6 pagesCost ST - 1 2018 (Solu)chitkarashellyPas encore d'évaluation

- Activity Based Costing Questions and NotesDocument11 pagesActivity Based Costing Questions and Notesviettuan9167% (3)

- Micro - Economies and Diseconomies of ScaleDocument9 pagesMicro - Economies and Diseconomies of ScaleTanvi ShahPas encore d'évaluation

- Sales Force act-WPS OfficeDocument22 pagesSales Force act-WPS Officebhagyashree devadasPas encore d'évaluation

- SOW Form 5 POA Term 2 2020 2021Document9 pagesSOW Form 5 POA Term 2 2020 2021Peta-Gay Brown-JohnsonPas encore d'évaluation