Vous aimerez peut-être aussi

- Islamic Banking And Finance for Beginners!D'EverandIslamic Banking And Finance for Beginners!Évaluation : 2 sur 5 étoiles2/5 (1)

- Manual On Financial Management of BarangayDocument37 pagesManual On Financial Management of BarangayPeriod Ampersand Asterisk80% (20)

- MBFI NotesDocument27 pagesMBFI NotesSrikanth Prasanna BhaskarPas encore d'évaluation

- Training ReportDocument71 pagesTraining ReportHardeep MalikPas encore d'évaluation

- Chapter:-1 Introduction of BankDocument54 pagesChapter:-1 Introduction of BankOmkar ChavanPas encore d'évaluation

- An Overview of BanksDocument11 pagesAn Overview of BanksgishaPas encore d'évaluation

- Unit IDocument11 pagesUnit IShahid AfreedPas encore d'évaluation

- Banks Finanl PresentationDocument31 pagesBanks Finanl PresentationADNANE OULKHAJPas encore d'évaluation

- Banking LawDocument22 pagesBanking LawRASHIKA TRIVEDIPas encore d'évaluation

- History of Bank: Prepired by Bdifatah SaidDocument5 pagesHistory of Bank: Prepired by Bdifatah SaidAbdifatah SaidPas encore d'évaluation

- What Is The Difference Between Commercial Banking and Merchant BankingDocument8 pagesWhat Is The Difference Between Commercial Banking and Merchant BankingScarlett Lewis100% (2)

- Indian BankingDocument7 pagesIndian BankingMONIKA RUBINPas encore d'évaluation

- Introduction To BankingDocument35 pagesIntroduction To Bankingকাশী নাথPas encore d'évaluation

- FINANCE - CreditDocument9 pagesFINANCE - CreditHoney GubalanePas encore d'évaluation

- Banking and InsuranceDocument115 pagesBanking and InsuranceLeonardPas encore d'évaluation

- The Banking System in Bangladesh: History of BankDocument7 pagesThe Banking System in Bangladesh: History of Bankmirmoinul100% (1)

- Money & Banking PresentationDocument54 pagesMoney & Banking PresentationmehmooddharalaPas encore d'évaluation

- History of Philippine BankingDocument11 pagesHistory of Philippine BankingMark Ceddrick MiolePas encore d'évaluation

- Chapter - 01 Introduction of BankDocument37 pagesChapter - 01 Introduction of BankJeeva JeevaPas encore d'évaluation

- History: Personal FinanceDocument9 pagesHistory: Personal FinanceAyush JainPas encore d'évaluation

- Anitha HDFCDocument84 pagesAnitha HDFCchaluvadiinPas encore d'évaluation

- Unit I Banking and Insurance Law Study NotesDocument12 pagesUnit I Banking and Insurance Law Study NotesSekar M KPRCAS-CommercePas encore d'évaluation

- Growth of Banking Sector in India IntroductionDocument12 pagesGrowth of Banking Sector in India IntroductionShaktee Varma0% (1)

- Philippine Banking SystemDocument9 pagesPhilippine Banking SystemJungkookie Bae100% (3)

- The Banking System in Bangladesh: Definition of BankDocument10 pagesThe Banking System in Bangladesh: Definition of BankmirmoinulPas encore d'évaluation

- An Overview of Banking Industry - Unit I: Lecture Notes SeriesDocument28 pagesAn Overview of Banking Industry - Unit I: Lecture Notes SeriesGame ProfilePas encore d'évaluation

- A Study On Risk Analysis On Personal Loans at Vijaya BankDocument90 pagesA Study On Risk Analysis On Personal Loans at Vijaya BankChethan.sPas encore d'évaluation

- Chapter 01 Power PointDocument37 pagesChapter 01 Power PointmuluPas encore d'évaluation

- 00000114-Banking Law Inculding Negotiable Instrument ActDocument47 pages00000114-Banking Law Inculding Negotiable Instrument Actakshay yadavPas encore d'évaluation

- Merchant BankingDocument10 pagesMerchant BankingSunita KanojiyaPas encore d'évaluation

- History of BankDocument10 pagesHistory of BankSadaf KhanPas encore d'évaluation

- Merchant Banking Vs Commercial BankingDocument73 pagesMerchant Banking Vs Commercial BankingUditSawantPas encore d'évaluation

- Lecture No.1 (Intro To Money & Banking)Document17 pagesLecture No.1 (Intro To Money & Banking)Usama MubasherPas encore d'évaluation

- BANKING AND INSURANCE (1) .Docx NewDocument59 pagesBANKING AND INSURANCE (1) .Docx Newsuganya100% (1)

- Fundamental of BankingDocument10 pagesFundamental of BankingAnonymous y3E7iaPas encore d'évaluation

- Merchant BankingDocument27 pagesMerchant Bankingapi-3865133100% (13)

- Importance of The Bank System To The EconomyDocument12 pagesImportance of The Bank System To The EconomyEmil SalmanliPas encore d'évaluation

- Nikhil Nilee - Project-1Document83 pagesNikhil Nilee - Project-1Vaibhav MohitePas encore d'évaluation

- Philippine Banking SystemDocument20 pagesPhilippine Banking SystempatriciaPas encore d'évaluation

- Introduction To BankingDocument17 pagesIntroduction To BankingmashalPas encore d'évaluation

- Lecture # 15: Role of Commercial BanksDocument46 pagesLecture # 15: Role of Commercial BanksMudassar NawazPas encore d'évaluation

- Merchant Banking NotesDocument24 pagesMerchant Banking NotesSharada KadurPas encore d'évaluation

- 1.1 Concept of BankingDocument12 pages1.1 Concept of BankingsidharthPas encore d'évaluation

- LPB Unit - IDocument17 pagesLPB Unit - ITony StarkPas encore d'évaluation

- Indian Banking SystemDocument42 pagesIndian Banking Systemdraun vashishtaPas encore d'évaluation

- What Is A Bank ? Introduction: - CrowtherDocument29 pagesWhat Is A Bank ? Introduction: - CrowtherHarbrinder GurmPas encore d'évaluation

- Essentials of Banking and FinanceDocument32 pagesEssentials of Banking and FinanceAsadvirkPas encore d'évaluation

- Final Copy 1Document15 pagesFinal Copy 1gagana sPas encore d'évaluation

- Internship - Report 9097676765677Document80 pagesInternship - Report 9097676765677Abhijeet MohantyPas encore d'évaluation

- Internship Report Done at INDIAN BANK BRDocument80 pagesInternship Report Done at INDIAN BANK BRAbhijeet MohantyPas encore d'évaluation

- BankingDocument15 pagesBankingJyoti BhardwajPas encore d'évaluation

- Review of LiteratureDocument65 pagesReview of LiteratureRUTUJA PATILPas encore d'évaluation

- Review of LiteratureDocument64 pagesReview of LiteratureRUTUJA PATILPas encore d'évaluation

- Evolution of BankingDocument66 pagesEvolution of BankingMani KrishPas encore d'évaluation

- History of Banking IndustryDocument7 pagesHistory of Banking IndustryKimberly PasaloPas encore d'évaluation

- 1history 2etymology 3definition 4banking 4.1standard Activities 4.2range of Activities 4.3channelsDocument10 pages1history 2etymology 3definition 4banking 4.1standard Activities 4.2range of Activities 4.3channelsjohnsrs92Pas encore d'évaluation

- Fundamental F Banking Law-1Document88 pagesFundamental F Banking Law-1ramadhanamos620Pas encore d'évaluation

- Mendoza Lance - 1st AssignmentDocument5 pagesMendoza Lance - 1st AssignmentLance Jimwell MendozaPas encore d'évaluation

- Role of BankingDocument47 pagesRole of BankingMubashir QureshiPas encore d'évaluation

- The Impact of Brand Extension On Parent Brand ImageDocument10 pagesThe Impact of Brand Extension On Parent Brand ImageKR BurkiPas encore d'évaluation

- Internship Sindh BankDocument34 pagesInternship Sindh BankKR Burki100% (1)

- Title Page Qurtuba 2Document71 pagesTitle Page Qurtuba 2KR BurkiPas encore d'évaluation

- FINANCE Internship Report Guidelines MBA BBADocument2 pagesFINANCE Internship Report Guidelines MBA BBAMunira TurarovaPas encore d'évaluation

- IndictmentDocument14 pagesIndictmentLansingStateJournalPas encore d'évaluation

- San Miguel Corporation vs. Bartolome Puzon Jr.Document2 pagesSan Miguel Corporation vs. Bartolome Puzon Jr.RavenFoxPas encore d'évaluation

- Morgan Allen Position Description Operations and Comm DirectorDocument2 pagesMorgan Allen Position Description Operations and Comm Directorj_morgan_allen1528Pas encore d'évaluation

- ChallanFormDocument1 pageChallanFormAman GargPas encore d'évaluation

- Report of Collections and DepositsDocument3 pagesReport of Collections and DepositsReign Hernandez100% (1)

- Teresita Suson and Antonio Fortich Vs People of The Philippines GR NO. 152848 July 12, 2006Document7 pagesTeresita Suson and Antonio Fortich Vs People of The Philippines GR NO. 152848 July 12, 2006Francis V MartinezPas encore d'évaluation

- Ca No. Ge (E) /agr/ of 2021-22 Serial Page No: 01Document50 pagesCa No. Ge (E) /agr/ of 2021-22 Serial Page No: 01fakePas encore d'évaluation

- Tax July 21 SugesstedDocument28 pagesTax July 21 SugesstedShailjaPas encore d'évaluation

- 2017-Botswana Business Application Form - JennyDocument1 page2017-Botswana Business Application Form - JennyCalvawell MuzvondiwaPas encore d'évaluation

- Bouncing Checks LawDocument29 pagesBouncing Checks Lawrachel panlilio100% (1)

- Locker ModuleDocument32 pagesLocker ModulebinalamitPas encore d'évaluation

- Application Form NIE (MoS&T)Document3 pagesApplication Form NIE (MoS&T)Muhammad AslamPas encore d'évaluation

- Equiable Banking v. IACDocument1 pageEquiable Banking v. IACEr BurgosPas encore d'évaluation

- An Analysis On Cash Management at Standard PolymersDocument20 pagesAn Analysis On Cash Management at Standard PolymersSathish BillaPas encore d'évaluation

- Purpose: Fiscal Procedure F525 - Petty CashDocument6 pagesPurpose: Fiscal Procedure F525 - Petty CashVictor TucoPas encore d'évaluation

- Voucher For Mobilization AdvanceDocument2 pagesVoucher For Mobilization AdvanceSaroj AcharyaPas encore d'évaluation

- Your Branch DetailsDocument7 pagesYour Branch DetailsAartiPas encore d'évaluation

- April StatementDocument2 pagesApril StatementRAHUL SINGH50% (2)

- Sosa V Atty. MendozaDocument6 pagesSosa V Atty. MendozacyrinecalPas encore d'évaluation

- Lozano vs. Martinez Political Law Case DigestsDocument3 pagesLozano vs. Martinez Political Law Case DigestsJulia JumagdaoPas encore d'évaluation

- Chapter 1: Literature Review: Overview of Commercial BankDocument16 pagesChapter 1: Literature Review: Overview of Commercial BankThảo NgọcPas encore d'évaluation

- Meezan BankDocument50 pagesMeezan BankUsman NasirPas encore d'évaluation

- Psychology of MoneyDocument34 pagesPsychology of MoneyMiriam Columbro33% (3)

- Quijano v. Bartolabac Labor StandardsDocument229 pagesQuijano v. Bartolabac Labor StandardsPaula BitorPas encore d'évaluation

- Methodex - Sap FicoDocument4 pagesMethodex - Sap Ficon_ashok_2020Pas encore d'évaluation

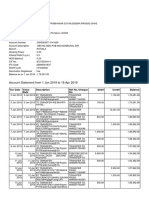

- Account Statement From 1 Jan 2019 To 18 Apr 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 1 Jan 2019 To 18 Apr 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceManoj PrabhakarPas encore d'évaluation

- Trial BalanceDocument3 pagesTrial BalanceFranca Okechukwu0% (2)

- Application For Convocation 37906 Gadage Sourabh ParmeshwarDocument2 pagesApplication For Convocation 37906 Gadage Sourabh ParmeshwarAshlesh KulkarniPas encore d'évaluation

- Interim PPT Abhinav KumarDocument18 pagesInterim PPT Abhinav Kumaramirana4uPas encore d'évaluation