Vous aimerez peut-être aussi

- Sample Church Audit ReportDocument5 pagesSample Church Audit Reportvrasshen580% (5)

- Summary of Richard A. Lambert's Financial Literacy for ManagersD'EverandSummary of Richard A. Lambert's Financial Literacy for ManagersPas encore d'évaluation

- N.S. Auditor General's January 2012 ReportDocument82 pagesN.S. Auditor General's January 2012 Reportnick_logan9361Pas encore d'évaluation

- Contract To Sell-Letter of IntentDocument4 pagesContract To Sell-Letter of IntentVj BrillantesPas encore d'évaluation

- Orient Fire District State Comptroller AuditDocument22 pagesOrient Fire District State Comptroller AuditTimesreviewPas encore d'évaluation

- Wallkill Hose Company Audit ReportDocument19 pagesWallkill Hose Company Audit ReportDaily FreemanPas encore d'évaluation

- North Castle AuditDocument13 pagesNorth Castle AuditCara MatthewsPas encore d'évaluation

- East Kingston Fire Company AuditDocument17 pagesEast Kingston Fire Company AuditDaily FreemanPas encore d'évaluation

- Eastchester Fire District: Internal Controls Over Financial OperationsDocument27 pagesEastchester Fire District: Internal Controls Over Financial OperationsCara MatthewsPas encore d'évaluation

- Mattituck Park District: Credit Cards and Segregation of DutiesDocument19 pagesMattituck Park District: Credit Cards and Segregation of DutiesSuffolk TimesPas encore d'évaluation

- Saratoga Springs City School District: Fund BalanceDocument13 pagesSaratoga Springs City School District: Fund BalanceBethany BumpPas encore d'évaluation

- Greenwich Central School District: Claims AuditingDocument12 pagesGreenwich Central School District: Claims AuditingBethany BumpPas encore d'évaluation

- Shandaken Payroll AuditDocument15 pagesShandaken Payroll AuditDaily FreemanPas encore d'évaluation

- Dutchess County AuditDocument15 pagesDutchess County AuditDaily FreemanPas encore d'évaluation

- Stephentown Audit by NYS ComptrollerDocument19 pagesStephentown Audit by NYS ComptrollereppelmannrPas encore d'évaluation

- Leon County District School Board: For The Fiscal Year Ended June 30, 2011Document85 pagesLeon County District School Board: For The Fiscal Year Ended June 30, 2011ChrisPas encore d'évaluation

- Mount Pleasant AuditDocument14 pagesMount Pleasant AuditCara MatthewsPas encore d'évaluation

- Audit Finds Irregularities at Guilderland Golf CourseDocument20 pagesAudit Finds Irregularities at Guilderland Golf CoursecathleencrowleyPas encore d'évaluation

- CPA EXAM QsDocument29 pagesCPA EXAM QsbajujuPas encore d'évaluation

- Spring Valley AuditDocument19 pagesSpring Valley AuditCara MatthewsPas encore d'évaluation

- Audit Report: ADMINISTRATIVE AND INTERNAL ACCOUNTING CONTROLS OVER THE OFFICE REVOLVING FUNDDocument31 pagesAudit Report: ADMINISTRATIVE AND INTERNAL ACCOUNTING CONTROLS OVER THE OFFICE REVOLVING FUNDjon_ortizPas encore d'évaluation

- Accounting and MonitoringDocument47 pagesAccounting and MonitoringslowcouchPas encore d'évaluation

- Audit of Lee County Commissioner ExpendituresDocument9 pagesAudit of Lee County Commissioner ExpendituresNews-PressPas encore d'évaluation

- Pamelia AuditDocument21 pagesPamelia AuditWatertown Daily TimesPas encore d'évaluation

- New Suffolk Audit, Dec. 2013Document29 pagesNew Suffolk Audit, Dec. 2013Grant ParpanPas encore d'évaluation

- Copenhagen Volunteer Fire 2021 114Document19 pagesCopenhagen Volunteer Fire 2021 114Jeff NelsonPas encore d'évaluation

- Week 5Document48 pagesWeek 5BookAddict721Pas encore d'évaluation

- CPA EXAM QsDocument34 pagesCPA EXAM QsYaj CruzadaPas encore d'évaluation

- Case StudyDocument6 pagesCase StudyErik PetersonPas encore d'évaluation

- Grand Jury Report On Internal Audit DivisionDocument7 pagesGrand Jury Report On Internal Audit DivisionThe Press-Enterprise / pressenterprise.comPas encore d'évaluation

- Saratoga Springs Housing Authority AuditDocument43 pagesSaratoga Springs Housing Authority AuditDavid LombardoPas encore d'évaluation

- Everett School District Audit Exit Conference DocumentDocument6 pagesEverett School District Audit Exit Conference DocumentJessica OlsonPas encore d'évaluation

- Central Davis Sewer District 2011 AuditDocument26 pagesCentral Davis Sewer District 2011 Auditapi-257848573Pas encore d'évaluation

- Maricopa Cty 6-30-05 Mangmt Ltr1Document16 pagesMaricopa Cty 6-30-05 Mangmt Ltr1tonygoprano2850Pas encore d'évaluation

- Audit of Mohonasen School DistrictDocument11 pagesAudit of Mohonasen School DistrictDavid LombardoPas encore d'évaluation

- Central Davis Sewer District 2012 Audited StatementsDocument28 pagesCentral Davis Sewer District 2012 Audited Statementsapi-257848573Pas encore d'évaluation

- North Green BushDocument23 pagesNorth Green BushjfrancorecordPas encore d'évaluation

- Problems Chapter 7Document9 pagesProblems Chapter 7Trang Le0% (1)

- Entrance Conference Document - 2013 SSD AuditsDocument4 pagesEntrance Conference Document - 2013 SSD AuditsJulian A.Pas encore d'évaluation

- CDCR Letter To State ControllerDocument1 pageCDCR Letter To State ControllerLakeCoNewsPas encore d'évaluation

- Wheeler VilleDocument16 pagesWheeler VilleBethany BumpPas encore d'évaluation

- Wolf Kathryn Dentistar CaseDocument4 pagesWolf Kathryn Dentistar Caseapi-239635502Pas encore d'évaluation

- Audit 4-30-12 2Document12 pagesAudit 4-30-12 2api-163536539Pas encore d'évaluation

- Saratoga CoDocument16 pagesSaratoga CoDennis YuskoPas encore d'évaluation

- Internal Audit For Nueces Co. Justices of The PeaceDocument36 pagesInternal Audit For Nueces Co. Justices of The PeacecallertimesPas encore d'évaluation

- General Brown Financial Report - Nov. 2014Document16 pagesGeneral Brown Financial Report - Nov. 2014Watertown Daily TimesPas encore d'évaluation

- NYS Comptroller - Wayne Cty. Healthcare EligibilityDocument14 pagesNYS Comptroller - Wayne Cty. Healthcare EligibilityerikvsorensenPas encore d'évaluation

- Off-Ledger Bank Account Study 2018 - 0Document12 pagesOff-Ledger Bank Account Study 2018 - 0Lin ChrisPas encore d'évaluation

- 2018BreathittFFES PRDocument11 pages2018BreathittFFES PRWYMT TelevisionPas encore d'évaluation

- Distrust, Disagreements, DysfunctionDocument25 pagesDistrust, Disagreements, DysfunctionRuth SchneiderPas encore d'évaluation

- AIS, CPA Material, Revenue CycleDocument29 pagesAIS, CPA Material, Revenue CycleDamien LeePas encore d'évaluation

- Leon County District School Board: For The Fiscal Year Ended June 30, 2014Document83 pagesLeon County District School Board: For The Fiscal Year Ended June 30, 2014ChrisPas encore d'évaluation

- NPO Acct ManualDocument26 pagesNPO Acct ManualdavidkongPas encore d'évaluation

- OPP ITO Appendix CDocument4 pagesOPP ITO Appendix Cishmael daroPas encore d'évaluation

- State Comptroller's Audit of The The Hendrick Hudson School District's Financial ConditionDocument11 pagesState Comptroller's Audit of The The Hendrick Hudson School District's Financial ConditionCara MatthewsPas encore d'évaluation

- Financial Review GuideDocument17 pagesFinancial Review GuideAngelPas encore d'évaluation

- Company, Against The Client Involving Possible Defective Products. It Is Probable That TheDocument5 pagesCompany, Against The Client Involving Possible Defective Products. It Is Probable That TheLucy AnaPas encore d'évaluation

- Audited ReportDocument34 pagesAudited Reportcares_2012Pas encore d'évaluation

- Audit of Account ReceivablesDocument18 pagesAudit of Account ReceivablesnaniappoPas encore d'évaluation

- 00 555Document129 pages00 555Giora RozmarinPas encore d'évaluation

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsPas encore d'évaluation

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorPas encore d'évaluation

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- State Health CoverageDocument26 pagesState Health CoveragejspectorPas encore d'évaluation

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorPas encore d'évaluation

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorPas encore d'évaluation

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinPas encore d'évaluation

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyPas encore d'évaluation

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorPas encore d'évaluation

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinPas encore d'évaluation

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorPas encore d'évaluation

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorPas encore d'évaluation

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorPas encore d'évaluation

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanPas encore d'évaluation

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorPas encore d'évaluation

- Class of 2022Document1 pageClass of 2022jspectorPas encore d'évaluation

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorPas encore d'évaluation

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorPas encore d'évaluation

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorPas encore d'évaluation

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorPas encore d'évaluation

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonPas encore d'évaluation

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorPas encore d'évaluation

- Voting Report CardDocument1 pageVoting Report CardjspectorPas encore d'évaluation

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorPas encore d'évaluation

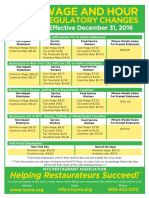

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorPas encore d'évaluation

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorPas encore d'évaluation

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanPas encore d'évaluation

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorPas encore d'évaluation

- KMI 30 IndexDocument27 pagesKMI 30 IndexSyed NomaanPas encore d'évaluation

- Fashion Retail Merchandising Retail Visit ReportDocument6 pagesFashion Retail Merchandising Retail Visit Reportchins1289Pas encore d'évaluation

- 2023 HSC Business StudiesDocument22 pages2023 HSC Business StudiesSreemoye ChakrabortyPas encore d'évaluation

- MGT657 Chapter 7Document49 pagesMGT657 Chapter 7adamPas encore d'évaluation

- The Compact For Responsive and Responsible Leadership: A Roadmap For Sustainable Long-Term Growth and OpportunityDocument1 pageThe Compact For Responsive and Responsible Leadership: A Roadmap For Sustainable Long-Term Growth and OpportunityMiguel AugustoPas encore d'évaluation

- OTHM L5 Diploma in Tourism and Hospitality Management Spec 2022 09 NewDocument31 pagesOTHM L5 Diploma in Tourism and Hospitality Management Spec 2022 09 Newajaya nathPas encore d'évaluation

- Strategic Choice: Group 1 Eugenio - Fernandez - Gabito - Goño - Iglopas - RamosDocument14 pagesStrategic Choice: Group 1 Eugenio - Fernandez - Gabito - Goño - Iglopas - Ramosjethro eugenioPas encore d'évaluation

- Financial Statement Analysis and Security Valuation 5th Edition by Penman ISBN Test BankDocument16 pagesFinancial Statement Analysis and Security Valuation 5th Edition by Penman ISBN Test Bankcindy100% (24)

- Death of Big LawDocument55 pagesDeath of Big Lawmaxxwe11Pas encore d'évaluation

- Mag BudgetDocument120 pagesMag BudgetPriya SinghPas encore d'évaluation

- GTE Financial Capacity Matrix (S) - Title & Name (2021)Document4 pagesGTE Financial Capacity Matrix (S) - Title & Name (2021)Anupriya RoyPas encore d'évaluation

- A Survey Paper - PM 1.0Document5 pagesA Survey Paper - PM 1.0Aswin KrishnanPas encore d'évaluation

- HRP Case StudyDocument1 pageHRP Case Studymruga_123Pas encore d'évaluation

- SalvoDocument8 pagesSalvoAlamgir HossainPas encore d'évaluation

- CF Final Group 3Document8 pagesCF Final Group 3Armyboy 1804Pas encore d'évaluation

- REACTIONDocument3 pagesREACTIONVhia ParajasPas encore d'évaluation

- Huntersvsfarmers 131204084857 Phpapp01Document1 pageHuntersvsfarmers 131204084857 Phpapp01Charles BronsonPas encore d'évaluation

- GPS vs. TJX Financial AnalysisDocument12 pagesGPS vs. TJX Financial AnalysisBen Van NestePas encore d'évaluation

- Standalone Accounts 2008Document87 pagesStandalone Accounts 2008Noore NayabPas encore d'évaluation

- Group 10 - ABC Case Study Corelio PrintingDocument10 pagesGroup 10 - ABC Case Study Corelio Printingmuhammad ifwatPas encore d'évaluation

- Tomato ProductsDocument5 pagesTomato ProductsDan Man100% (1)

- ENVYSION Commodity Strategy Fund PresentationDocument17 pagesENVYSION Commodity Strategy Fund PresentationNicky TsaiPas encore d'évaluation

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument5 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSandesh Pujari100% (1)

- Quality Cost SummaryDocument2 pagesQuality Cost SummaryirfanPas encore d'évaluation

- A Study On Credit Risk Management at Canara BankDocument10 pagesA Study On Credit Risk Management at Canara BankBhaswani33% (6)

- The History of The Philippine Currency: Republic Central CollegesDocument8 pagesThe History of The Philippine Currency: Republic Central CollegesDaishin Kingsley SesePas encore d'évaluation

- Fountil BriefDocument28 pagesFountil BriefRAJYOGPas encore d'évaluation

- PRABHAVATHI Form26QBDocument2 pagesPRABHAVATHI Form26QBPrakash BattalaPas encore d'évaluation