Vous aimerez peut-être aussi

- Center For MedicareDocument1 pageCenter For Medicareapi-25909546Pas encore d'évaluation

- Summary of The Medicare and Medicaid Extenders Act of 2010Document3 pagesSummary of The Medicare and Medicaid Extenders Act of 2010api-25909546Pas encore d'évaluation

- Summary TablesDocument36 pagesSummary Tablesapi-25909546Pas encore d'évaluation

- A Bill: 111 Congress 2 SDocument3 pagesA Bill: 111 Congress 2 Sapi-25909546Pas encore d'évaluation

- PPTRASummaryFinal10 11 18Document1 pagePPTRASummaryFinal10 11 18api-25909546Pas encore d'évaluation

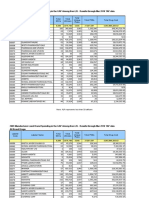

- 2009 Manufacturer-Level Brand Spending in The GAP Among Non-LIS - Results Through Mar 2010 TAP Data All Brand DrugsDocument13 pages2009 Manufacturer-Level Brand Spending in The GAP Among Non-LIS - Results Through Mar 2010 TAP Data All Brand Drugsapi-25909546Pas encore d'évaluation

- FDACensorCase10 09 29Document2 pagesFDACensorCase10 09 29api-25909546Pas encore d'évaluation

- CBO2010SGRMenu REVISEDFINAL10 04 30Document2 pagesCBO2010SGRMenu REVISEDFINAL10 04 30api-25909546Pas encore d'évaluation

- IOWAINSCOMM MLRWaiverRequest10 09 21Document2 pagesIOWAINSCOMM MLRWaiverRequest10 09 21api-25909546Pas encore d'évaluation

- Affordable Care Act Update: Implementing Medicare Costs SavingsDocument10 pagesAffordable Care Act Update: Implementing Medicare Costs Savingsapi-25909546Pas encore d'évaluation

- Security Administration, Department of Labor Office of Consumer Information and Insurance Oversight, Department of Health and Human ServicesDocument83 pagesSecurity Administration, Department of Labor Office of Consumer Information and Insurance Oversight, Department of Health and Human Servicesapi-25909546Pas encore d'évaluation

- Don Berwick For CMS Administrator: Support From Former CMS AdministratorsDocument10 pagesDon Berwick For CMS Administrator: Support From Former CMS Administratorsapi-25909546Pas encore d'évaluation

- Office of The Actuary DATE: April 22, 2010 FROM: Solomon M. Mussey SUBJECT: Estimated Effects of The "Patient Protection and Affordable Care Act,"Document3 pagesOffice of The Actuary DATE: April 22, 2010 FROM: Solomon M. Mussey SUBJECT: Estimated Effects of The "Patient Protection and Affordable Care Act,"api-25909546Pas encore d'évaluation

- Healthreformhellweeknote10 03 17Document1 pageHealthreformhellweeknote10 03 17api-25909546Pas encore d'évaluation

- To: From: Ranking Republican David Dreier (R-San Dimas, CA) Subject: The Slaughter Solution: Bending The Rules Beyond BeliefDocument4 pagesTo: From: Ranking Republican David Dreier (R-San Dimas, CA) Subject: The Slaughter Solution: Bending The Rules Beyond Beliefapi-25909546Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)