Vous aimerez peut-être aussi

- Sale Hi 2016Document20 pagesSale Hi 2016PippoPas encore d'évaluation

- An Empirical Study On Audit Expectation Gap Role of Auditing Education in BangladeshDocument17 pagesAn Empirical Study On Audit Expectation Gap Role of Auditing Education in Bangladeshrajeshaisdu009100% (1)

- Audit Expectation Gap in AuditorDocument3 pagesAudit Expectation Gap in AuditorTantanLePas encore d'évaluation

- Audit Education Role in Decreasing The Expectation GapDocument9 pagesAudit Education Role in Decreasing The Expectation GapRONAL FERNANDO QUINTERO VEGAPas encore d'évaluation

- Disclosure on sustainable development, CSR environmental disclosure and greater value recognized to the company by usersD'EverandDisclosure on sustainable development, CSR environmental disclosure and greater value recognized to the company by usersPas encore d'évaluation

- Agyei Et Al - 2013 - An Assessment of Audit Expectation Gap in GhanaDocument7 pagesAgyei Et Al - 2013 - An Assessment of Audit Expectation Gap in GhanathoritruongPas encore d'évaluation

- Contingent Liability Effect: Case StudyDocument9 pagesContingent Liability Effect: Case StudyWinnie WenPas encore d'évaluation

- Narrowing The Expectation Gap in Auditing The Role of TheDocument11 pagesNarrowing The Expectation Gap in Auditing The Role of Theعلي الماغوطPas encore d'évaluation

- Audit Expectation Gap: Perspectives of Auditors and Audited Account Users Olagunju, AdebayoDocument19 pagesAudit Expectation Gap: Perspectives of Auditors and Audited Account Users Olagunju, AdebayosigiryaPas encore d'évaluation

- Can The Expectation Gap Be ReducedDocument7 pagesCan The Expectation Gap Be ReducedAbdulAzeemPas encore d'évaluation

- Is The External Audit Report Useful For Bankruptcy Prediction? Evidence Using Artificial IntelligenceDocument23 pagesIs The External Audit Report Useful For Bankruptcy Prediction? Evidence Using Artificial IntelligenceZylene JanelaPas encore d'évaluation

- Adeyemi and UadialeDocument8 pagesAdeyemi and UadialealiraxPas encore d'évaluation

- An Analytical Study On The Methods of Narrowing The Expectations Gap in The AuditingDocument7 pagesAn Analytical Study On The Methods of Narrowing The Expectations Gap in The AuditingaijbmPas encore d'évaluation

- The Audit Expectation Gap: An Empirical Study in MalaysiaDocument15 pagesThe Audit Expectation Gap: An Empirical Study in Malaysiaak shPas encore d'évaluation

- The Expectation Gap in AuditingDocument9 pagesThe Expectation Gap in AuditingHoài NguyễnPas encore d'évaluation

- Expectation Gap Study Case From Kingdom of BahrainDocument13 pagesExpectation Gap Study Case From Kingdom of BahrainReynardo GosalPas encore d'évaluation

- Audit II AssignmentDocument10 pagesAudit II AssignmentEric Wong Jun JiePas encore d'évaluation

- Artikel 1 UTS Ganjil 20212022Document15 pagesArtikel 1 UTS Ganjil 20212022Muthia KanshaPas encore d'évaluation

- Fraud Detection, Redress and Reporting by Auditors: Managerial Auditing Journal October 2010Document22 pagesFraud Detection, Redress and Reporting by Auditors: Managerial Auditing Journal October 2010Fred The FishPas encore d'évaluation

- The Process of Financial Planning, 2nd Edition: Developing a Financial PlanD'EverandThe Process of Financial Planning, 2nd Edition: Developing a Financial PlanPas encore d'évaluation

- Audit Expectaion GapDocument12 pagesAudit Expectaion GapCharles Guandaru Kamau100% (1)

- WilsonR Web15 1Document17 pagesWilsonR Web15 1indana afiyahPas encore d'évaluation

- Audit Firm Tenure and Financial Restatement - An Analysis of Industry Specialization N Fee EffectsDocument29 pagesAudit Firm Tenure and Financial Restatement - An Analysis of Industry Specialization N Fee EffectsDefita ThalibPas encore d'évaluation

- Accountability RooijDocument24 pagesAccountability RooijLeila SalemPas encore d'évaluation

- Canary in The Cage Mike Pinnock UK Dept Education Child Protection Report Sept 2011Document28 pagesCanary in The Cage Mike Pinnock UK Dept Education Child Protection Report Sept 2011Rick ThomaPas encore d'évaluation

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveD'EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectivePas encore d'évaluation

- 1 PBDocument14 pages1 PBBarzan HasanPas encore d'évaluation

- Accountability - A SynthesisDocument10 pagesAccountability - A SynthesisnailaweoungPas encore d'évaluation

- Audit Expectation Gap ThesisDocument4 pagesAudit Expectation Gap Thesisloribowiesiouxfalls100% (2)

- External Audit ThesisDocument8 pagesExternal Audit ThesisLisa Riley100% (2)

- Jurnal InternasionalDocument20 pagesJurnal InternasionalfajaradisamarthaPas encore d'évaluation

- 01chapter1 PDFDocument20 pages01chapter1 PDFRashel MahmudPas encore d'évaluation

- 01 Chapter 1Document21 pages01 Chapter 1Stylishe AliPas encore d'évaluation

- Key Audit Matter and Auditor Liability Evidence From Auditor Evaluators in ThailandDocument22 pagesKey Audit Matter and Auditor Liability Evidence From Auditor Evaluators in ThailandSalmanugraheniPas encore d'évaluation

- AREG-Users Perception in NigeriaDocument10 pagesAREG-Users Perception in NigeriaEdosa Joshua AronmwanPas encore d'évaluation

- Conceptual Framework On Forensic AuditingDocument3 pagesConceptual Framework On Forensic Auditingarcherselevators67% (3)

- Thesis Internal AuditDocument7 pagesThesis Internal Auditameliarichardsonsouthbend100% (2)

- Budgeting in The Public SectorDocument21 pagesBudgeting in The Public SectornatlyhPas encore d'évaluation

- National Project Management Maturity: A Conceptual FrameworkDocument20 pagesNational Project Management Maturity: A Conceptual FrameworkTejas CjPas encore d'évaluation

- Cox 3Document9 pagesCox 3Camilo EsquiaquiPas encore d'évaluation

- Accounting DiscussionDocument7 pagesAccounting DiscussionHuda MousaPas encore d'évaluation

- Albersmann - 2020Document38 pagesAlbersmann - 2020Iis IstianahPas encore d'évaluation

- Kamau - 2013 Determinants of Audit Expectation Gap - Evidence From Limited Companies in KenyaDocument12 pagesKamau - 2013 Determinants of Audit Expectation Gap - Evidence From Limited Companies in KenyathoritruongPas encore d'évaluation

- Thesis Audit CommitteeDocument7 pagesThesis Audit Committeelarissaswensonsiouxfalls100% (2)

- Academic Writing MidtermDocument4 pagesAcademic Writing MidtermJung AuLiaPas encore d'évaluation

- Chapters SummaryDocument13 pagesChapters SummarymorrisPas encore d'évaluation

- This Content Downloaded From 196.188.65.10 On Wed, 17 Jun 2020 10:28:08 UTCDocument19 pagesThis Content Downloaded From 196.188.65.10 On Wed, 17 Jun 2020 10:28:08 UTCembiale ayaluPas encore d'évaluation

- THESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementDocument46 pagesTHESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementVon Ianelle AguilaPas encore d'évaluation

- Defining Auditing - 1 - 1Document17 pagesDefining Auditing - 1 - 1RICHMOND GYAMFI BOATENGPas encore d'évaluation

- Final Dissertation SignificatoDocument6 pagesFinal Dissertation SignificatoBuyDissertationPaperSpringfield100% (1)

- 795-Article Text-1808-1-10-20200403Document12 pages795-Article Text-1808-1-10-20200403dhentya putriPas encore d'évaluation

- Safety Performance Literature ReviewDocument8 pagesSafety Performance Literature Reviewpnquihcnd100% (1)

- AGA AssignmentDocument16 pagesAGA AssignmentLakshmi KannanPas encore d'évaluation

- MOCK Et Al. (2013) - The Audit Reporting Model - Current Research Synthesis and ImplicationsDocument30 pagesMOCK Et Al. (2013) - The Audit Reporting Model - Current Research Synthesis and ImplicationsJoão SilvaPas encore d'évaluation

- The Audit Expectations Gap in BritainDocument33 pagesThe Audit Expectations Gap in Britainnguyenthuan1211Pas encore d'évaluation

- Audit Expectation GapDocument19 pagesAudit Expectation GapRudi FachruPas encore d'évaluation

- (IMF Working Papers) Does Performance Budgeting Work? An Analytical Review of The Empirical LiteratureDocument49 pages(IMF Working Papers) Does Performance Budgeting Work? An Analytical Review of The Empirical LiteratureHAMIDOU ATIRBI CÉPHASPas encore d'évaluation

- Outcome Costinginthe Public SectorDocument28 pagesOutcome Costinginthe Public SectorTHILAKA A/P VELOOSAMY MoePas encore d'évaluation

- International Financial Management: Harvard Business School Ec Course Paper December 2005Document31 pagesInternational Financial Management: Harvard Business School Ec Course Paper December 2005Rishika JainPas encore d'évaluation

- Soal Audit Chapter 7-13Document26 pagesSoal Audit Chapter 7-13Jhayanti Nithyananda KalyaniPas encore d'évaluation

- Soal Audit Chapter 7-13Document6 pagesSoal Audit Chapter 7-13Jhayanti Nithyananda KalyaniPas encore d'évaluation

- Sas 110Document23 pagesSas 110Jhayanti Nithyananda KalyaniPas encore d'évaluation

- GCU CHP Flowchart PDFDocument1 pageGCU CHP Flowchart PDFJhayanti Nithyananda KalyaniPas encore d'évaluation

- DCUBS Research Paper Series 13Document33 pagesDCUBS Research Paper Series 13Jhayanti Nithyananda KalyaniPas encore d'évaluation

- Audit PrinciplesDocument34 pagesAudit PrinciplesJhayanti Nithyananda KalyaniPas encore d'évaluation

- Audit Expectaion GapDocument12 pagesAudit Expectaion GapCharles Guandaru Kamau100% (1)

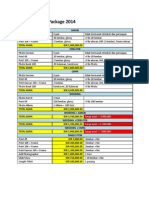

- Vphotography Package 2014: Harga Awal - 3.900.000 Harga Awal - 5.700.000 Harga Awal - 7.400.000Document1 pageVphotography Package 2014: Harga Awal - 3.900.000 Harga Awal - 5.700.000 Harga Awal - 7.400.000Jhayanti Nithyananda KalyaniPas encore d'évaluation

- Sony: Betting It All On Blu-Ray SynopsisDocument4 pagesSony: Betting It All On Blu-Ray SynopsisJhayanti Nithyananda KalyaniPas encore d'évaluation

- Branch Node City Node City Distance NodeDocument3 pagesBranch Node City Node City Distance NodeJhayanti Nithyananda KalyaniPas encore d'évaluation

- Vphotography Package 2014: Harga Awal - 3.900.000 Harga Awal - 5.700.000 Harga Awal - 7.400.000Document1 pageVphotography Package 2014: Harga Awal - 3.900.000 Harga Awal - 5.700.000 Harga Awal - 7.400.000Jhayanti Nithyananda KalyaniPas encore d'évaluation

- Book 1Document4 pagesBook 1Namaku IzamPas encore d'évaluation

- Objective Function Z X + X + X + X + X + X + X + X + X: Branch Node City Node City Distance Node Network FlowDocument3 pagesObjective Function Z X + X + X + X + X + X + X + X + X: Branch Node City Node City Distance Node Network FlowJhayanti Nithyananda KalyaniPas encore d'évaluation

- Pertemuan 7Document2 pagesPertemuan 7Jhayanti Nithyananda KalyaniPas encore d'évaluation

- Chap 011Document18 pagesChap 011Yana Pandu PrawiraPas encore d'évaluation

- AuditingDocument52 pagesAuditingJhayanti Nithyananda KalyaniPas encore d'évaluation

- Marketing EthicDocument24 pagesMarketing EthicJhayanti Nithyananda KalyaniPas encore d'évaluation

- 990i 1 PDFDocument0 page990i 1 PDFJhayanti Nithyananda KalyaniPas encore d'évaluation

- F017468736 3Document22 pagesF017468736 3Jhayanti Nithyananda KalyaniPas encore d'évaluation

- Marketing EthicDocument24 pagesMarketing EthicJhayanti Nithyananda KalyaniPas encore d'évaluation

- Au 00110 PDFDocument3 pagesAu 00110 PDFJhayanti Nithyananda KalyaniPas encore d'évaluation

- APL Vancouver QA - 18Feb-AL (FAQ)Document5 pagesAPL Vancouver QA - 18Feb-AL (FAQ)sreejith100% (1)

- DASAR - Slide Fondasi Audit Internal - Hananto Widhiatmoko (PUBLISH)Document58 pagesDASAR - Slide Fondasi Audit Internal - Hananto Widhiatmoko (PUBLISH)Pingkan OmpiPas encore d'évaluation

- Behre Dolbear Feasibility Studies SOQDocument14 pagesBehre Dolbear Feasibility Studies SOQKhishigbayar PurevdavgaPas encore d'évaluation

- KS SDN BHD - Account AdjustmentsDocument6 pagesKS SDN BHD - Account Adjustmentsalia_aziziPas encore d'évaluation

- Implication of Clauses in EPCDocument9 pagesImplication of Clauses in EPCSrinivas AmaraPas encore d'évaluation

- DTMFIs Minimum Licensing Requirements 2020 FinalDocument21 pagesDTMFIs Minimum Licensing Requirements 2020 FinalLesley munikwaPas encore d'évaluation

- Public Service Delivery Audit (Pasada)Document26 pagesPublic Service Delivery Audit (Pasada)HR DILG-CARPas encore d'évaluation

- Chapter 18 - Financial Management Learning GoalsDocument25 pagesChapter 18 - Financial Management Learning GoalsRille LuPas encore d'évaluation

- HAND BOOK ON Audit of WorksDocument160 pagesHAND BOOK ON Audit of WorksnathanabsPas encore d'évaluation

- Accounting Accruals and Prepayments ExerciseDocument5 pagesAccounting Accruals and Prepayments ExerciseAdelynePas encore d'évaluation

- Running Head: Project ManagementDocument23 pagesRunning Head: Project ManagementHassan SiddiquiPas encore d'évaluation

- McDonalds Charities CEO Refuses To Explain Why Save-A-Life Foundation Grant Records Were Prematurely DestroyedDocument14 pagesMcDonalds Charities CEO Refuses To Explain Why Save-A-Life Foundation Grant Records Were Prematurely DestroyedPeter M. HeimlichPas encore d'évaluation

- Financial Accountant Manager Controller in Lexington KY Resume Philip WiemerDocument2 pagesFinancial Accountant Manager Controller in Lexington KY Resume Philip WiemerPhilipWeimerPas encore d'évaluation

- Ministry of Finance Strategy For Afghanistan National Development StrategyDocument28 pagesMinistry of Finance Strategy For Afghanistan National Development StrategyAchaemenidAdvisorsPas encore d'évaluation

- Annalyn Flore NDO: ObjectiveDocument8 pagesAnnalyn Flore NDO: ObjectiveAnnalyn O. FlorendoPas encore d'évaluation

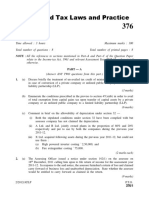

- Advanced Tax Laws and PracticeDocument8 pagesAdvanced Tax Laws and Practicesheena2saPas encore d'évaluation

- Benoy Mathew Resume-1Document2 pagesBenoy Mathew Resume-1Benoy MathewPas encore d'évaluation

- Statutory AuditDocument3 pagesStatutory Auditnurlieya09Pas encore d'évaluation

- Chap03 ProblemsDocument16 pagesChap03 ProblemsCyrilCalaloPas encore d'évaluation

- PMTE - PM TE and SAD Nominal Amount (Effective For Audits of Periods Ending On or After 15 December 2020)Document47 pagesPMTE - PM TE and SAD Nominal Amount (Effective For Audits of Periods Ending On or After 15 December 2020)Monirul Islam Moniirr100% (1)

- Project ProposalDocument9 pagesProject ProposalJohn Christoper ErminoPas encore d'évaluation

- Empanelment of ValuersDocument4 pagesEmpanelment of ValuersNandlal KumavatPas encore d'évaluation

- Tema EnglezaDocument7 pagesTema EnglezaLupitu Aura DanielaPas encore d'évaluation

- Statement of Management Responsibility For Financial StatementsDocument3 pagesStatement of Management Responsibility For Financial StatementsmocsPas encore d'évaluation

- CHAPTER 3 - Organizational Ethics: Lesson OverviewDocument22 pagesCHAPTER 3 - Organizational Ethics: Lesson OverviewTrúc NguyễnPas encore d'évaluation

- ACCO 30053 - Audit of Investments - MARPDocument10 pagesACCO 30053 - Audit of Investments - MARPBanna SplitPas encore d'évaluation

- 6 Essentials in Oil and Gas Project Management 2011Document25 pages6 Essentials in Oil and Gas Project Management 2011Mendez Forbes JinPas encore d'évaluation

- Test Bank For Auditing A Risk Based Approach To Conducting A Quality Audit 9th Edition by JohnstoneDocument24 pagesTest Bank For Auditing A Risk Based Approach To Conducting A Quality Audit 9th Edition by JohnstoneOmarPerrysqjp100% (46)

- Internship Report of Global Insurance Ltd. by M A Muhaimin Alveen Batch-XIIDocument16 pagesInternship Report of Global Insurance Ltd. by M A Muhaimin Alveen Batch-XIIKIRAN BHATTARAIPas encore d'évaluation

- GCG AssessmentDocument29 pagesGCG AssessmentDinda MediyantiPas encore d'évaluation