Vous aimerez peut-être aussi

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Analysis Using HHIDocument8 pagesAnalysis Using HHIfazlayPas encore d'évaluation

- Brand MGT Draft SlideDocument23 pagesBrand MGT Draft SlidefazlayPas encore d'évaluation

- MPORT POLICY (2009-2012) Bangladesh Import PolicyDocument3 pagesMPORT POLICY (2009-2012) Bangladesh Import PolicyfazlayPas encore d'évaluation

- Category and Brand Management, Product Identification, and New-Product PlanningDocument27 pagesCategory and Brand Management, Product Identification, and New-Product PlanningfazlayPas encore d'évaluation

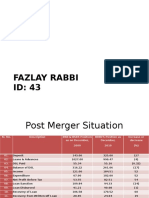

- Merger of BDBLDocument6 pagesMerger of BDBLfazlayPas encore d'évaluation

- Executive SummaryDocument3 pagesExecutive Summaryfazlay50% (2)

- Report of Cse ExportDocument24 pagesReport of Cse ExportfazlayPas encore d'évaluation

- Preface of Bangladesh Import PolicyDocument22 pagesPreface of Bangladesh Import PolicyfazlayPas encore d'évaluation

- 11 Steps For GMATDocument4 pages11 Steps For GMATfazlayPas encore d'évaluation

- Application Form Teacher 2Document3 pagesApplication Form Teacher 2fazlayPas encore d'évaluation

- The Magical Number SevenDocument3 pagesThe Magical Number SevenfazlayPas encore d'évaluation

- Chap 002Document15 pagesChap 002fazlayPas encore d'évaluation

- Stepping Stones or Building BlocsDocument3 pagesStepping Stones or Building BlocsfazlayPas encore d'évaluation

- Rmbœv - Wek We' VJQ, XVKV: WB QVM WeáwßDocument2 pagesRmbœv - Wek We' VJQ, XVKV: WB QVM WeáwßfazlayPas encore d'évaluation

- CLDocument1 pageCLfazlayPas encore d'évaluation

- Application Form Teacher 1Document3 pagesApplication Form Teacher 1fazlayPas encore d'évaluation

- BatnaDocument7 pagesBatnaSindy KangPas encore d'évaluation

- Backward Linkages in Readymade Garment Industry of Bangladesh: Appraisal and Policy ImplicationsDocument11 pagesBackward Linkages in Readymade Garment Industry of Bangladesh: Appraisal and Policy ImplicationsfazlayPas encore d'évaluation

- Leather Goods FinalDocument15 pagesLeather Goods FinalImran1978Pas encore d'évaluation

- User and Producers of A SIRIDocument2 pagesUser and Producers of A SIRIfazlayPas encore d'évaluation

- 1 s2.0 S0195666313002171 MainDocument8 pages1 s2.0 S0195666313002171 MainfazlayPas encore d'évaluation

- I. Current/Non-current Method Ii. Monetary/Non-monetary Method Iii. Currency Rate MethodDocument2 pagesI. Current/Non-current Method Ii. Monetary/Non-monetary Method Iii. Currency Rate MethodfazlayPas encore d'évaluation

- Apparel and FootwearDocument50 pagesApparel and FootwearfazlayPas encore d'évaluation

- Leather Industry of BangladeshDocument1 pageLeather Industry of BangladeshfazlayPas encore d'évaluation

- Certificate in International Trade and Finance: Michele DonnellyDocument12 pagesCertificate in International Trade and Finance: Michele DonnellyfazlayPas encore d'évaluation

- Certificate in International Trade and Finance: Michele DonnellyDocument12 pagesCertificate in International Trade and Finance: Michele DonnellyfazlayPas encore d'évaluation

- Enron Bank ScandalDocument2 pagesEnron Bank ScandalfazlayPas encore d'évaluation

- Lehman Brothers ScandalDocument1 pageLehman Brothers ScandalfazlayPas encore d'évaluation

- A Comparative Study of Financial Performance of Banking Sector in Bangladesh - B. NimalathasanDocument12 pagesA Comparative Study of Financial Performance of Banking Sector in Bangladesh - B. NimalathasanfarhanPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- TOOLS AND Materials USED IN EMBROIDERYDocument56 pagesTOOLS AND Materials USED IN EMBROIDERYChristy ParinasanPas encore d'évaluation

- Crochets Ruby Gloom PatternDocument9 pagesCrochets Ruby Gloom PatternLauraPas encore d'évaluation

- Cutting Machine Spreading Machine Fabric IdDocument1 pageCutting Machine Spreading Machine Fabric IdEruPas encore d'évaluation

- NSQF - Knitting Machine Operator - Circular KnittingDocument23 pagesNSQF - Knitting Machine Operator - Circular KnittingSakibMDShafiuddinPas encore d'évaluation

- Short Notes On FabricsDocument4 pagesShort Notes On Fabricsmaisura nayeemPas encore d'évaluation

- Croma Ceramic MoaDocument28 pagesCroma Ceramic MoaAmit GajjarPas encore d'évaluation

- TESTEX Brochure 210414Document46 pagesTESTEX Brochure 210414Tahir NizamPas encore d'évaluation

- Indian ImportersDocument18 pagesIndian ImportersSarika YadavPas encore d'évaluation

- Sublimation Heat Press Settings: Quick Reference GuideDocument1 pageSublimation Heat Press Settings: Quick Reference GuideDavid BrownPas encore d'évaluation

- DetailedDocument12 pagesDetailedHiawatha Ares ReyesPas encore d'évaluation

- Atlas of Goat ProductsDocument384 pagesAtlas of Goat ProductsFaisal MohommadPas encore d'évaluation

- End Term Assigment Fibre To ConsumerDocument33 pagesEnd Term Assigment Fibre To ConsumerShweeta jambhulkarPas encore d'évaluation

- TT - R19 - 184p 25 BooksDocument184 pagesTT - R19 - 184p 25 BooksKanchiSrinivasPas encore d'évaluation

- Application Generator InsulationDocument5 pagesApplication Generator Insulationsrsethu00Pas encore d'évaluation

- ASCC L2Lecture Two THE INDUSTRIAL REVOLUTION - 1Document8 pagesASCC L2Lecture Two THE INDUSTRIAL REVOLUTION - 1ABDOU T O U M IPas encore d'évaluation

- 18 NTU TE 0060 - PDFDocument10 pages18 NTU TE 0060 - PDFFahad HussainPas encore d'évaluation

- Industrial Revolution NotesDocument62 pagesIndustrial Revolution Noteskwezi kennedyPas encore d'évaluation

- Best Available Techniques in Textile ClothingDocument53 pagesBest Available Techniques in Textile ClothingKingson_786Pas encore d'évaluation

- Assessor Eligibility Criteria 18 01 2021 FinalDocument342 pagesAssessor Eligibility Criteria 18 01 2021 FinalDheeraj SinghPas encore d'évaluation

- Elements of Textile: Instruction To CandidatesDocument2 pagesElements of Textile: Instruction To CandidatesGaganpreet Kaur Fashion DesigningPas encore d'évaluation

- Syllabus For TR Supervisors Quality AssurnaceDocument67 pagesSyllabus For TR Supervisors Quality Assurnaceadnanlibra194Pas encore d'évaluation

- Clothing Guide Men Latest Lowres PDFDocument35 pagesClothing Guide Men Latest Lowres PDFEncarniVergaraPas encore d'évaluation

- As 1818-1976 Flax Canvas Including Water-Bag CanvasDocument5 pagesAs 1818-1976 Flax Canvas Including Water-Bag CanvasSAI Global - APACPas encore d'évaluation

- FlameStopI FicheTechnique EngDocument1 pageFlameStopI FicheTechnique EngTestPas encore d'évaluation

- Textile DictionaryDocument40 pagesTextile DictionaryMd Noman100% (1)

- Catalogo Dainese Bike 2017 Low-ResDocument23 pagesCatalogo Dainese Bike 2017 Low-ResVeronica MicozziPas encore d'évaluation

- PLM Case StudyDocument4 pagesPLM Case StudyMANOJPas encore d'évaluation

- Cotton Yarn Fabrics ExportersDocument9 pagesCotton Yarn Fabrics Exportersfayyazbhatti178Pas encore d'évaluation

- New Hybrids Lienhard EversmannDocument7 pagesNew Hybrids Lienhard EversmannparatinadanaPas encore d'évaluation

- Textile Softeners On Cotton Dyed With Direct Dyes: Re Ectance and Fastness AssessmentsDocument5 pagesTextile Softeners On Cotton Dyed With Direct Dyes: Re Ectance and Fastness AssessmentsIrfak SaputraPas encore d'évaluation