Vous aimerez peut-être aussi

- #IndiaStockExchange #BSE Update On 24th June 2015Document2 pages#IndiaStockExchange #BSE Update On 24th June 2015Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Foreign Direct Investment in Equity Market in IndiaDocument4 pagesForeign Direct Investment in Equity Market in IndiaJhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

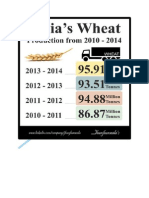

- India's Wheat Production From 2010 To 2014Document4 pagesIndia's Wheat Production From 2010 To 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Document3 pagesIndia's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Per Capita Food Grain For 2014Document3 pagesIndia's Per Capita Food Grain For 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- MSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Document4 pagesMSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India Coir Trade From April To October 2014Document4 pagesIndia Coir Trade From April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Rice Trade For 2014Document5 pagesIndia's Rice Trade For 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

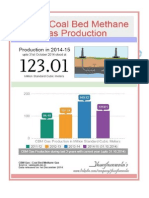

- India's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Document3 pagesIndia's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Diamond Reserves With Diamond Trade Update For 2014Document6 pagesIndia's Diamond Reserves With Diamond Trade Update For 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Foreign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Document3 pagesForeign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

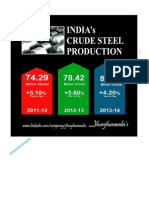

- India's Crude Steel Production Estimate For 2014 To 2017Document3 pagesIndia's Crude Steel Production Estimate For 2014 To 2017Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Coal Production For Last 5 Years Upto October 2014Document2 pagesIndia's Coal Production For Last 5 Years Upto October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India Crude Steel Production From 2011-2014Document4 pagesIndia Crude Steel Production From 2011-2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Methane Hydrates Reserves 25th November 2014Document3 pagesIndia's Methane Hydrates Reserves 25th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Global Central Banks Highlights For Monetary Policy Rates For October 2014Document31 pagesGlobal Central Banks Highlights For Monetary Policy Rates For October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Coal Reserves To Last 100 YearsDocument3 pagesIndia's Coal Reserves To Last 100 YearsJhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Kharif and Rabi Crops Area Coverage For October and January 2014Document10 pagesIndia's Kharif and Rabi Crops Area Coverage For October and January 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India Tax Collection From April To November 2014Document11 pagesIndia Tax Collection From April To November 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Foreign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Document27 pagesForeign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Mineral Production in Month of August 2014Document3 pagesIndia's Mineral Production in Month of August 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India 'S Total Kharif Crop Sowing Area As On July and August 2014Document6 pagesIndia 'S Total Kharif Crop Sowing Area As On July and August 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Index of Eight Core Industries From June To November 2014Document57 pagesIndia's Index of Eight Core Industries From June To November 2014Jhunjhunwalas Digital Finance & Business Info Library100% (1)

- India's Import and Export Update For September and December 2014Document16 pagesIndia's Import and Export Update For September and December 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Indians Railways Revenue Earnings With Freight Traffic During April To October 2014Document18 pagesIndians Railways Revenue Earnings With Freight Traffic During April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Fuel Price Change For Petrol, Diesel, and JetFuel in IndiaDocument11 pagesFuel Price Change For Petrol, Diesel, and JetFuel in IndiaJhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Tourism Sector Performance For January and October 2014Document15 pagesIndia's Tourism Sector Performance For January and October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Indian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Document5 pagesIndian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

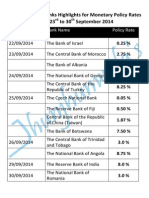

- Global Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Document11 pagesGlobal Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- A Review of Hybrid Solar PV and Wind Energy SystemDocument12 pagesA Review of Hybrid Solar PV and Wind Energy SystemTato LeonPas encore d'évaluation

- Science Electricity NotesDocument7 pagesScience Electricity NotesZIMO WANG (Student)Pas encore d'évaluation

- IntershipDocument40 pagesIntershipNishaPas encore d'évaluation

- RRL and ReferencesDocument6 pagesRRL and ReferencesDeveen SolisPas encore d'évaluation

- Plant-Inspection Midterm ExamsDocument5 pagesPlant-Inspection Midterm ExamsClarence Jay AcaylarPas encore d'évaluation

- 'Documents - MX 20130411223811 PDFDocument103 pages'Documents - MX 20130411223811 PDFRdy SimangunsongPas encore d'évaluation

- Agency Blacklisting RulesDocument10 pagesAgency Blacklisting Rulesrpshvju100% (1)

- Seminar Presentation On Micro Power GeneratorDocument25 pagesSeminar Presentation On Micro Power GeneratorDev Kumar100% (5)

- VSP Final ReportDocument53 pagesVSP Final ReportAnand GautamPas encore d'évaluation

- 162U1A0243 (Masthan Basha)Document54 pages162U1A0243 (Masthan Basha)Venkata SaiPas encore d'évaluation

- Automatic Generation Control of Interconnected Power System With Diverse Sources of Power GenerationDocument15 pagesAutomatic Generation Control of Interconnected Power System With Diverse Sources of Power GenerationVahid SadeghiPas encore d'évaluation

- Impact of Energy From Bagasse On Mauritius/SocietyDocument46 pagesImpact of Energy From Bagasse On Mauritius/SocietyVedhish HalkhariPas encore d'évaluation

- Ee 367 Unit 2 NewDocument86 pagesEe 367 Unit 2 NewyaaPas encore d'évaluation

- Thesis Defense: Group 1 10-St. CorneliusDocument39 pagesThesis Defense: Group 1 10-St. CorneliusMatt Gabriell LegaspiPas encore d'évaluation

- Invertir en Renovables en La ArgentinaDocument78 pagesInvertir en Renovables en La ArgentinaCronista.com100% (1)

- Pei201309 DLDocument116 pagesPei201309 DLNinh Quoc TrungPas encore d'évaluation

- Solar Hybrid PowerplantDocument29 pagesSolar Hybrid PowerplantSulaim Abdul LatheefPas encore d'évaluation

- Reports DCRTPP June15Document105 pagesReports DCRTPP June15Parmeshwar Nath TripathiPas encore d'évaluation

- Large Motor Starting CalculationDocument5 pagesLarge Motor Starting CalculationBert De Borja100% (1)

- SST interfaced PMSG based offshore wind energy analysisDocument10 pagesSST interfaced PMSG based offshore wind energy analysisrishabh shahPas encore d'évaluation

- Capstone Ni Harrold Na Naka PDFDocument41 pagesCapstone Ni Harrold Na Naka PDFJeus BatadlanPas encore d'évaluation

- IRJET V5I4179 With Cover Page v2Document9 pagesIRJET V5I4179 With Cover Page v2yifiyyfyi bhvxhddfiPas encore d'évaluation

- Victorian Annual Planning Report 2019Document87 pagesVictorian Annual Planning Report 2019Kory WangPas encore d'évaluation

- Project Scope for Sustainable Home ConstructionDocument7 pagesProject Scope for Sustainable Home ConstructionFridaPas encore d'évaluation

- Pursuing Master Degree in Sustainable EnergyDocument20 pagesPursuing Master Degree in Sustainable EnergyChristianto LukmantoroPas encore d'évaluation

- 2005 Report CardDocument24 pages2005 Report Carddod108Pas encore d'évaluation

- Endress Präsentation Prettl Partnertag 09.2017 en V3Document71 pagesEndress Präsentation Prettl Partnertag 09.2017 en V3Daniel MuratallaPas encore d'évaluation

- Nuursnii SudalgaaDocument69 pagesNuursnii SudalgaaBayarmaa Bat-OrshikhPas encore d'évaluation

- Global Energy Perspectives by Dr. H. RameshDocument48 pagesGlobal Energy Perspectives by Dr. H. Rameshhram_phdPas encore d'évaluation