Vous aimerez peut-être aussi

- Asian Economic Integration Report 2021: Making Digital Platforms Work for Asia and the PacificD'EverandAsian Economic Integration Report 2021: Making Digital Platforms Work for Asia and the PacificPas encore d'évaluation

- Inductive and Deductive Reasoning LPDocument7 pagesInductive and Deductive Reasoning LPapi-313517608Pas encore d'évaluation

- Compound Financial InstrumentDocument1 pageCompound Financial InstrumentMarissaPas encore d'évaluation

- Testing of HypothesisDocument19 pagesTesting of HypothesisJayendra Kamat0% (1)

- Chapter 2+3-MCQDocument2 pagesChapter 2+3-MCQNguyễn Việt LêPas encore d'évaluation

- AfardocDocument14 pagesAfardocJhedz CartasPas encore d'évaluation

- Financial Management II Booklet It UDocument38 pagesFinancial Management II Booklet It UahmedPas encore d'évaluation

- CRITIQUE #1: On The Importance of Critical Thinking and Critical Writing in The Social SciencesDocument3 pagesCRITIQUE #1: On The Importance of Critical Thinking and Critical Writing in The Social SciencesSamson NgPas encore d'évaluation

- Fear and Risk in Audit Process PDFDocument25 pagesFear and Risk in Audit Process PDFElena DobrePas encore d'évaluation

- Financial Markets and Institutions Test Bank (011 020)Document10 pagesFinancial Markets and Institutions Test Bank (011 020)Thị Ba PhạmPas encore d'évaluation

- Case 2Document4 pagesCase 2Chris WongPas encore d'évaluation

- 9Document16 pages9edmarian0% (1)

- Problem Stock ValuationDocument5 pagesProblem Stock ValuationbajujuPas encore d'évaluation

- ISA - 315 Understanding The Entity & Its Environment & Assessing The Risks of Material MisstatementDocument13 pagesISA - 315 Understanding The Entity & Its Environment & Assessing The Risks of Material MisstatementsajedulPas encore d'évaluation

- Theory of Accounts L. R. Cabarles Toa.112 - Impairment of Assets Lecture NotesDocument5 pagesTheory of Accounts L. R. Cabarles Toa.112 - Impairment of Assets Lecture NotesPia DagmanPas encore d'évaluation

- Aou (Swot)Document4 pagesAou (Swot)Saad Ali100% (1)

- Chapter 7Document13 pagesChapter 7lov3m3Pas encore d'évaluation

- Chapter 1 Financial Asset, MoneyDocument34 pagesChapter 1 Financial Asset, Moneyasbmz16Pas encore d'évaluation

- Financial Management MCQsDocument27 pagesFinancial Management MCQsYogesh KamraPas encore d'évaluation

- PeprlDocument1 pagePeprlCarl Zenon GarciaPas encore d'évaluation

- PHLE-Module-2 PHLE - Module-2: Pharmacy (University of Bohol) Pharmacy (University of Bohol)Document53 pagesPHLE-Module-2 PHLE - Module-2: Pharmacy (University of Bohol) Pharmacy (University of Bohol)Margaret RPas encore d'évaluation

- Chapter 8 QuizDocument3 pagesChapter 8 QuizTriet Nguyen0% (1)

- Financial Planning and ForecastingDocument35 pagesFinancial Planning and Forecastingphyu swePas encore d'évaluation

- Chapter 5 MC and TFDocument12 pagesChapter 5 MC and TFAngela de Mesa100% (1)

- Illustrative CADocument2 pagesIllustrative CAEllie YsonPas encore d'évaluation

- Mgt401 Midterm 2010 McqsDocument35 pagesMgt401 Midterm 2010 McqsMèhàŕ MàŕiàPas encore d'évaluation

- Relevant Costing NotesDocument30 pagesRelevant Costing NotesJungkook100% (1)

- CapmDocument7 pagesCapmVaishali ShuklaPas encore d'évaluation

- Gitman - Test Bank CH - 14Document41 pagesGitman - Test Bank CH - 14Hazem TharwatPas encore d'évaluation

- Chapter 2Document4 pagesChapter 2HuyNguyễnQuangHuỳnhPas encore d'évaluation

- CPALE Primer 2.5Document13 pagesCPALE Primer 2.5JarvelPas encore d'évaluation

- Exercices On Chapter 13Document21 pagesExercices On Chapter 13gheedaPas encore d'évaluation

- Responsibility Accounting EvaluationDocument9 pagesResponsibility Accounting EvaluationPaulo SalanguitPas encore d'évaluation

- 1 Risk and ReturnDocument24 pages1 Risk and ReturnMohammad DwidarPas encore d'évaluation

- Conceptual Frameworks For Accounting Standards I - Chapter 1Document3 pagesConceptual Frameworks For Accounting Standards I - Chapter 1Khey ManuelPas encore d'évaluation

- H2 Accounting ProfessionDocument9 pagesH2 Accounting ProfessionTrek ApostolPas encore d'évaluation

- MAS Handout - Working Capital Management and Financing PDFDocument5 pagesMAS Handout - Working Capital Management and Financing PDFDivine VictoriaPas encore d'évaluation

- AT.M-1405 Risk Assessment and Responses To RiskDocument10 pagesAT.M-1405 Risk Assessment and Responses To RiskErika LanezPas encore d'évaluation

- 3.3.6 Mod EvaluationDocument6 pages3.3.6 Mod EvaluationWelshfyn ConstantinoPas encore d'évaluation

- M00340020220114128M0034-PT11-12-The Expenditure CycleDocument25 pagesM00340020220114128M0034-PT11-12-The Expenditure CycleriznaldoPas encore d'évaluation

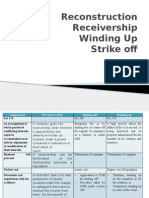

- Reconstruction Receivership Winding Up Strike OffDocument71 pagesReconstruction Receivership Winding Up Strike OffMohammad Hasrul AkmalPas encore d'évaluation

- CH06 Testbank HIH9e MCDocument19 pagesCH06 Testbank HIH9e MCGanessa RolandPas encore d'évaluation

- The Afn FormulaDocument1 pageThe Afn Formulasplendidhcc100% (2)

- CH 11Document34 pagesCH 11ReneePas encore d'évaluation

- TBCH 12Document35 pagesTBCH 12Tornike JashiPas encore d'évaluation

- Chapter 16Document2 pagesChapter 16hanna sanchezPas encore d'évaluation

- Payout Policy: File, Then Send That File Back To Google Classwork - Assignment by Due Date & Due Time!Document4 pagesPayout Policy: File, Then Send That File Back To Google Classwork - Assignment by Due Date & Due Time!Gian RandangPas encore d'évaluation

- Capital Structure and Leverage: Multiple Choice: ConceptualDocument1 pageCapital Structure and Leverage: Multiple Choice: ConceptualKaye JavellanaPas encore d'évaluation

- New Venture Finance Startup Funding For Entrepreneurs PDFDocument26 pagesNew Venture Finance Startup Funding For Entrepreneurs PDFBhagavan BangalorePas encore d'évaluation

- Test Bank 8Document13 pagesTest Bank 8Jason Lazaroff67% (3)

- Gitman Chapter4Document19 pagesGitman Chapter4Hannah Jane UmbayPas encore d'évaluation

- Acctg 100C 08Document2 pagesAcctg 100C 08Maddie ManganoPas encore d'évaluation

- B&a - MCQDocument11 pagesB&a - MCQAniket PuriPas encore d'évaluation

- 07 TQMDocument32 pages07 TQMimran27pk50% (2)

- AT 05 Auditor - S Response To Assessed RiskDocument4 pagesAT 05 Auditor - S Response To Assessed RiskjeromyPas encore d'évaluation

- CAS 520 Analytical ProceduresDocument8 pagesCAS 520 Analytical ProcedureszelcomeiaukPas encore d'évaluation

- Finals Conceptual Framework and Accounting Standards AnswerkeyDocument7 pagesFinals Conceptual Framework and Accounting Standards AnswerkeyMay Anne MenesesPas encore d'évaluation

- Chapter 3Document37 pagesChapter 3Haniyah LazimPas encore d'évaluation

- Chap 16 Organizational CultureDocument16 pagesChap 16 Organizational CultureMuhammad Hashim MemonPas encore d'évaluation

- Hedge&Mutual MCQ 1581Document12 pagesHedge&Mutual MCQ 1581Bryan GohPas encore d'évaluation

- IPPTChap 001Document30 pagesIPPTChap 001ttu3319Pas encore d'évaluation

- Management: Leading & Collaborating in A Competitive WorldDocument32 pagesManagement: Leading & Collaborating in A Competitive WorldHuey Koon TeePas encore d'évaluation

- Instructions For Installing Problem Solver - Docx and DurationDocument1 pageInstructions For Installing Problem Solver - Docx and DurationГал БадрахPas encore d'évaluation

- Alibaba ArticleDocument3 pagesAlibaba ArticleГал БадрахPas encore d'évaluation

- Ayush JavDocument1 pageAyush JavГал БадрахPas encore d'évaluation

- Chapter Three A Review of Statistical Principles Useful in FinanceDocument6 pagesChapter Three A Review of Statistical Principles Useful in FinanceГал БадрахPas encore d'évaluation

- ClintonDocument1 pageClintonГал БадрахPas encore d'évaluation

- AxasxDocument26 pagesAxasxГал БадрахPas encore d'évaluation

- AxasxDocument26 pagesAxasxГал БадрахPas encore d'évaluation

- Problem Set 4Document3 pagesProblem Set 4Гал БадрахPas encore d'évaluation

- Starting A Bookstore BusinessDocument11 pagesStarting A Bookstore BusinessBunkun15Pas encore d'évaluation

- SUGI Report - III - 2018Document87 pagesSUGI Report - III - 2018KevinPas encore d'évaluation

- Book by IcmaiDocument262 pagesBook by IcmaiRashmeet AroraPas encore d'évaluation

- The Salvage Law Act No. 2616: Sanilyn V. Ramirez Llb3Document9 pagesThe Salvage Law Act No. 2616: Sanilyn V. Ramirez Llb3Syannil ViePas encore d'évaluation

- The Two Different Concepts of PrivatizationDocument8 pagesThe Two Different Concepts of PrivatizationGiancarlo Palomino CamaPas encore d'évaluation

- Net Present Value (NPV) Definition - Calculation - ExamplesDocument3 pagesNet Present Value (NPV) Definition - Calculation - ExamplesKadiri OlanrewajuPas encore d'évaluation

- Bangalore Property Buying ChecklistDocument42 pagesBangalore Property Buying ChecklistSudhakar GanjikuntaPas encore d'évaluation

- LDNA Tool FinancialDocument2 pagesLDNA Tool FinancialJonathan Marc Fule CastilloPas encore d'évaluation

- Extremely Important Proforma of Projected P L Balance Sheet of Both Partnership Firm Sole Proprietorship Business With Cma Data Analysis For Cash Credit LoanDocument31 pagesExtremely Important Proforma of Projected P L Balance Sheet of Both Partnership Firm Sole Proprietorship Business With Cma Data Analysis For Cash Credit LoanMonty 20Pas encore d'évaluation

- Detail Project Report On Export of Bracken FernDocument19 pagesDetail Project Report On Export of Bracken FernHarpy happyPas encore d'évaluation

- Gillard Ariff Liquidator GattoDocument4 pagesGillard Ariff Liquidator GattoSenateBriberyInquiryPas encore d'évaluation

- Lecture 08 - Relative Valuation - Using Market ComparablesDocument76 pagesLecture 08 - Relative Valuation - Using Market ComparablesDanila GallaratoPas encore d'évaluation

- Ch03 ExercisesDocument19 pagesCh03 Exercisesfunke michaelsPas encore d'évaluation

- DMRC Project ManagementDocument21 pagesDMRC Project ManagementArputhaPas encore d'évaluation

- Coca-Cola Co., NOPAT CalculationDocument2 pagesCoca-Cola Co., NOPAT CalculationNiomi GolraiPas encore d'évaluation

- Xacc280 Week3 Reading2Document56 pagesXacc280 Week3 Reading2osharpening9402Pas encore d'évaluation

- Excel - 33 - 38Document4 pagesExcel - 33 - 38api-259228049Pas encore d'évaluation

- Identifying The Problems and Finding Solutions of The Billing Section of Janata Bank LimitedDocument79 pagesIdentifying The Problems and Finding Solutions of The Billing Section of Janata Bank LimitedMd Abu Sayeed MustafaPas encore d'évaluation

- Vince Courtney Response To SFPUC Staff ComplaintDocument4 pagesVince Courtney Response To SFPUC Staff ComplaintAnonymous exSSC0Pz100% (1)

- Bank StatementsDocument4 pagesBank StatementsFrancisco NaranjoPas encore d'évaluation

- w2-2020 Fillabalbe BlankDocument1 pagew2-2020 Fillabalbe Blankmuhammad mudassarPas encore d'évaluation

- Police Personal File: 2 X 2 PictureDocument6 pagesPolice Personal File: 2 X 2 PicturePuma Base CcpsPas encore d'évaluation

- Financial StatementDocument5 pagesFinancial StatementJubelle Tacusalme PunzalanPas encore d'évaluation

- Name ACC1204 Chapter Quiz #1, Chapter 1 Time: 10 MinutesDocument2 pagesName ACC1204 Chapter Quiz #1, Chapter 1 Time: 10 MinutesMutong ZhengPas encore d'évaluation

- MC DonalDocument42 pagesMC DonalSeema RahulPas encore d'évaluation

- Starbucks Case AnalysisDocument14 pagesStarbucks Case AnalysisJade Marie CoronadoPas encore d'évaluation

- House Bill 667Document10 pagesHouse Bill 667daggerpressPas encore d'évaluation

- Chap06 Cost AllocationDocument62 pagesChap06 Cost AllocationSamsiah SukardiPas encore d'évaluation

- Definitions For IB EconomicsDocument26 pagesDefinitions For IB EconomicsMohamed Mohideen50% (2)

- Tax Exemptions On Retirement PlansDocument3 pagesTax Exemptions On Retirement PlansVola AriPas encore d'évaluation