Vous aimerez peut-être aussi

- India Morning Bell 5th December 2014Document18 pagesIndia Morning Bell 5th December 2014Just ChillPas encore d'évaluation

- Prime Focus - Q4FY12 - Result Update - Centrum 09062012Document4 pagesPrime Focus - Q4FY12 - Result Update - Centrum 09062012Varsha BangPas encore d'évaluation

- Aditya Birla Nuvo: Consolidating Growth BusinessesDocument6 pagesAditya Birla Nuvo: Consolidating Growth BusinessesSouravMalikPas encore d'évaluation

- Mahindra Satyam: Performance HighlightsDocument12 pagesMahindra Satyam: Performance HighlightsAngel BrokingPas encore d'évaluation

- Dishman, 12th February, 2013Document10 pagesDishman, 12th February, 2013Angel BrokingPas encore d'évaluation

- Financial AnalysisDocument7 pagesFinancial AnalysisDead ShotPas encore d'évaluation

- Wyeth - Q4FY12 Result Update - Centrum 22052012Document4 pagesWyeth - Q4FY12 Result Update - Centrum 22052012SwamiPas encore d'évaluation

- Rs 203 BUY: Key Take AwayDocument6 pagesRs 203 BUY: Key Take Awayabhi_003Pas encore d'évaluation

- Market Outlook 11th August 2011Document4 pagesMarket Outlook 11th August 2011Angel BrokingPas encore d'évaluation

- Nestle India: Performance HighlightsDocument9 pagesNestle India: Performance HighlightsAngel BrokingPas encore d'évaluation

- Jyoti Structures 4Q FY 2013Document10 pagesJyoti Structures 4Q FY 2013Angel BrokingPas encore d'évaluation

- Punjab National Bank: Performance HighlightsDocument12 pagesPunjab National Bank: Performance HighlightsAngel BrokingPas encore d'évaluation

- CIL (Maintain Buy) 3QFY12 Result Update 25 January 2012 (IFIN)Document5 pagesCIL (Maintain Buy) 3QFY12 Result Update 25 January 2012 (IFIN)Gaayaatrii BehuraaPas encore d'évaluation

- Market Outlook Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingPas encore d'évaluation

- Bharti Airtel, 1Q FY 2014Document14 pagesBharti Airtel, 1Q FY 2014Angel BrokingPas encore d'évaluation

- Hinduja Global Solutions: Healthcare Spending To Drive Growth Margins To ExpandDocument4 pagesHinduja Global Solutions: Healthcare Spending To Drive Growth Margins To Expandapi-234474152Pas encore d'évaluation

- TRIVENI140509 Wwwmon3yworldblogspotcomDocument3 pagesTRIVENI140509 Wwwmon3yworldblogspotcomAbhishek Kr. MishraPas encore d'évaluation

- BhartiAirtel-1QFY2013RU 10th AugDocument13 pagesBhartiAirtel-1QFY2013RU 10th AugAngel BrokingPas encore d'évaluation

- SBI, 19th February, 2013Document14 pagesSBI, 19th February, 2013Angel BrokingPas encore d'évaluation

- Coal India: Performance HighlightsDocument10 pagesCoal India: Performance HighlightsAngel BrokingPas encore d'évaluation

- Food Producer IndustryDocument3 pagesFood Producer IndustryAbu HurairaPas encore d'évaluation

- KSL Ongc 29jul08Document7 pagesKSL Ongc 29jul08srinivasan9Pas encore d'évaluation

- CCL Products (India) LTD: Key Financial IndicatorsDocument4 pagesCCL Products (India) LTD: Key Financial IndicatorsRk ParmarPas encore d'évaluation

- Dabur India: Performance HighlightsDocument10 pagesDabur India: Performance HighlightsAngel BrokingPas encore d'évaluation

- United Spirits: Performance HighlightsDocument11 pagesUnited Spirits: Performance HighlightsAngel BrokingPas encore d'évaluation

- United Spirits, 1Q FY 2014Document10 pagesUnited Spirits, 1Q FY 2014Angel BrokingPas encore d'évaluation

- PI Industries Q1FY12 Result 1-August-11Document6 pagesPI Industries Q1FY12 Result 1-August-11equityanalystinvestorPas encore d'évaluation

- Cordlife Group Limited: Results ReviewDocument10 pagesCordlife Group Limited: Results ReviewKelvin FuPas encore d'évaluation

- Market Outlook 26th September 2011Document3 pagesMarket Outlook 26th September 2011Angel BrokingPas encore d'évaluation

- Dishman 2QFY2013RUDocument10 pagesDishman 2QFY2013RUAngel BrokingPas encore d'évaluation

- Bumi Armada 4QFY11 20120228Document3 pagesBumi Armada 4QFY11 20120228Bimb SecPas encore d'évaluation

- Atlas BankDocument145 pagesAtlas BankWaqas NawazPas encore d'évaluation

- GCC Equity Report: ResearchDocument10 pagesGCC Equity Report: ResearchfahadsiddiquiPas encore d'évaluation

- Market Outlook 10th August 2011Document5 pagesMarket Outlook 10th August 2011Angel BrokingPas encore d'évaluation

- Commodity Price of #Gold, #Sliver, #Copper, #Doller/rs and Many More. Narnolia Securities Limited Market Diary 18.02.2014Document6 pagesCommodity Price of #Gold, #Sliver, #Copper, #Doller/rs and Many More. Narnolia Securities Limited Market Diary 18.02.2014Narnolia Securities LimitedPas encore d'évaluation

- TGBL, 6th February, 2013Document11 pagesTGBL, 6th February, 2013Angel BrokingPas encore d'évaluation

- Misc (Hold, Eps ) : HLIB ResearchDocument3 pagesMisc (Hold, Eps ) : HLIB ResearchJames WarrenPas encore d'évaluation

- Half Yearly Dec09-10 PDFDocument15 pagesHalf Yearly Dec09-10 PDFSalman S. ZiaPas encore d'évaluation

- Tech Mahindra: Performance HighlightsDocument11 pagesTech Mahindra: Performance HighlightsAngel BrokingPas encore d'évaluation

- Coal India: Performance HighlightsDocument11 pagesCoal India: Performance HighlightsAngel BrokingPas encore d'évaluation

- Bakrie Sumatra Plantation: Perplexing End To A Confusing YearDocument5 pagesBakrie Sumatra Plantation: Perplexing End To A Confusing YearerlanggaherpPas encore d'évaluation

- DB Corp: Key Management TakeawaysDocument6 pagesDB Corp: Key Management TakeawaysAngel BrokingPas encore d'évaluation

- Ultratech 4Q FY 2013Document10 pagesUltratech 4Q FY 2013Angel BrokingPas encore d'évaluation

- Growing Sustainably: Hindustan Unilever LimitedDocument164 pagesGrowing Sustainably: Hindustan Unilever LimitedFarid PatcaPas encore d'évaluation

- JP Associates 4Q FY 2013Document13 pagesJP Associates 4Q FY 2013Angel BrokingPas encore d'évaluation

- Aljazira Capital 2012Document14 pagesAljazira Capital 2012fathalbabPas encore d'évaluation

- Market Outlook 20th July 2011Document7 pagesMarket Outlook 20th July 2011Angel BrokingPas encore d'évaluation

- Motilal Oswal Sees 20% UPSIDE in Piramal Pharma Healthy RecoveryDocument8 pagesMotilal Oswal Sees 20% UPSIDE in Piramal Pharma Healthy RecoveryMohammed Israr ShaikhPas encore d'évaluation

- Fauji Cement Company Limited Annual-Report-2012Document63 pagesFauji Cement Company Limited Annual-Report-2012Saleem Khan0% (1)

- Astra International 1H11 Investor Summit Capital Market Expo 2011 PresentationDocument20 pagesAstra International 1H11 Investor Summit Capital Market Expo 2011 PresentationWibawo Huang Un UnPas encore d'évaluation

- Cairn India: Mopng Allows Exploration in Rajasthan BlockDocument4 pagesCairn India: Mopng Allows Exploration in Rajasthan BlockDarshan MaldePas encore d'évaluation

- Sun Pharma, 12th February, 2013Document11 pagesSun Pharma, 12th February, 2013Angel BrokingPas encore d'évaluation

- L&T 4Q Fy 2013Document15 pagesL&T 4Q Fy 2013Angel BrokingPas encore d'évaluation

- Trend Analysis of Ultratech Cement - Aditya Birla Group.Document9 pagesTrend Analysis of Ultratech Cement - Aditya Birla Group.Kanhay VishariaPas encore d'évaluation

- Abbott India, 2Q CY 2013Document12 pagesAbbott India, 2Q CY 2013Angel BrokingPas encore d'évaluation

- Tech Mahindra Result UpdatedDocument12 pagesTech Mahindra Result UpdatedAngel BrokingPas encore d'évaluation

- Siyaram Silk Mills Result UpdatedDocument9 pagesSiyaram Silk Mills Result UpdatedAngel BrokingPas encore d'évaluation

- JP Associates: Performance HighlightsDocument12 pagesJP Associates: Performance HighlightsAngel BrokingPas encore d'évaluation

- Bank of India: Performance HighlightsDocument12 pagesBank of India: Performance HighlightsAngel BrokingPas encore d'évaluation

- List of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosD'EverandList of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosPas encore d'évaluation

- First Morning Technical Call 3rd February 2015Document5 pagesFirst Morning Technical Call 3rd February 2015Just ChillPas encore d'évaluation

- Daily White Board 3rd February 2015Document1 pageDaily White Board 3rd February 2015Just ChillPas encore d'évaluation

- Monetary Policy Review Dec 2014 - ComposedDocument8 pagesMonetary Policy Review Dec 2014 - ComposedJust ChillPas encore d'évaluation

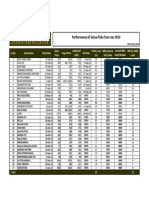

- Performance of Value Pick Since 2014-2Document1 pagePerformance of Value Pick Since 2014-2Just ChillPas encore d'évaluation

- News & Events 3rd February 2015Document1 pageNews & Events 3rd February 2015Just ChillPas encore d'évaluation

- WeSchool PGDM Finance 98Document26 pagesWeSchool PGDM Finance 98Just ChillPas encore d'évaluation

- Links SlideshareDocument4 pagesLinks SlideshareJust ChillPas encore d'évaluation

- 1600 Amphitheatre Parkway Mountain View California: Google IncDocument7 pages1600 Amphitheatre Parkway Mountain View California: Google IncJust ChillPas encore d'évaluation

- Gopeekrishnan Pillai Retail ManagementDocument1 pageGopeekrishnan Pillai Retail ManagementJust ChillPas encore d'évaluation

- AFS - Automotive Sector Caselet - Strategy For Rural MarketsDocument2 pagesAFS - Automotive Sector Caselet - Strategy For Rural MarketsJust ChillPas encore d'évaluation

- BimaruDocument2 pagesBimaruJust ChillPas encore d'évaluation

- SSRN Id896802Document35 pagesSSRN Id896802Just ChillPas encore d'évaluation

- Presentation Title Impact Assessment Of: 1. Sports Education 2. Jan Jagruti Aabhiyan 3. Project With Magic BusDocument16 pagesPresentation Title Impact Assessment Of: 1. Sports Education 2. Jan Jagruti Aabhiyan 3. Project With Magic BusJust ChillPas encore d'évaluation

- Executive SummaryDocument1 pageExecutive SummaryJust ChillPas encore d'évaluation

- BoiDocument1 pageBoiJust ChillPas encore d'évaluation

- Privatization of Coal Mines in IndiaDocument2 pagesPrivatization of Coal Mines in IndiaJust ChillPas encore d'évaluation

- Amol Micromax Brand RepositioningDocument5 pagesAmol Micromax Brand RepositioningJust ChillPas encore d'évaluation

- FinanceSolutions Manual of FMDocument170 pagesFinanceSolutions Manual of FMRahman Ullah Khan100% (2)

- Project On Retail Banking With Special Reference To YES BANKDocument111 pagesProject On Retail Banking With Special Reference To YES BANKWaxen Vency DmelloPas encore d'évaluation

- Sampling PJDocument1 pageSampling PJJust ChillPas encore d'évaluation

- Problems Faced by Agriculture in IndiaDocument5 pagesProblems Faced by Agriculture in IndiaJust ChillPas encore d'évaluation

- Banking Statistics: 2.1.1. Statistics Based On Statutory ReturnsDocument63 pagesBanking Statistics: 2.1.1. Statistics Based On Statutory ReturnsKirubaker PrabuPas encore d'évaluation

- A Summary of Key Financial RatiosDocument4 pagesA Summary of Key Financial Ratiosroshan24Pas encore d'évaluation

- Banking LicensesDocument7 pagesBanking LicensesJust ChillPas encore d'évaluation

- Privatization of Coal Mines in IndiaDocument2 pagesPrivatization of Coal Mines in IndiaJust ChillPas encore d'évaluation

- Lecture1-Fundamentals of Direct Taxes - 8.2.2013Document31 pagesLecture1-Fundamentals of Direct Taxes - 8.2.2013Just ChillPas encore d'évaluation

- Cash CE Bank Recon POC PCFDocument8 pagesCash CE Bank Recon POC PCFemman neriPas encore d'évaluation

- Bsba BMDocument3 pagesBsba BMAe R ONPas encore d'évaluation

- ROA and ROEDocument20 pagesROA and ROEPassmore DubePas encore d'évaluation

- Business Finance TGDocument339 pagesBusiness Finance TGCharisse Dianne P. Andoy100% (2)

- Exercise of Merger and AcquisitionDocument2 pagesExercise of Merger and AcquisitionzainabhayatPas encore d'évaluation

- GSK Report 2008 FullDocument212 pagesGSK Report 2008 FullSerhat ERTANPas encore d'évaluation

- Chapter 1 Accounting and Business EnvironmentDocument18 pagesChapter 1 Accounting and Business EnvironmentKim FloresPas encore d'évaluation

- A Signal Processing Perspective On Financial EngineeringDocument39 pagesA Signal Processing Perspective On Financial EngineeringSam SonPas encore d'évaluation

- Nordstrom Investment ProjectDocument11 pagesNordstrom Investment ProjectThiaka GilbertPas encore d'évaluation

- Khalid Nail Factory PlantDocument25 pagesKhalid Nail Factory Plantmuluken walelgn100% (1)

- Answer - Practice Question 1 - Statement of Changes in Equity.Document2 pagesAnswer - Practice Question 1 - Statement of Changes in Equity.Rizzy Ice-cream Milo0% (1)

- Quiz 13Document23 pagesQuiz 13Syeda Raiha Raza GardeziPas encore d'évaluation

- Dawn EditorialDocument92 pagesDawn EditorialShahryarPas encore d'évaluation

- LLQP: Quickfact Formulas: Underwriting & Claims Need For InsuranceDocument2 pagesLLQP: Quickfact Formulas: Underwriting & Claims Need For Insurancepkgarg_iitkgp100% (2)

- Company Update - ISAT 20181019 Network Rejuvenation in 2019 Will The New Era Turly Arrive PDFDocument5 pagesCompany Update - ISAT 20181019 Network Rejuvenation in 2019 Will The New Era Turly Arrive PDFFathur Abrar hazimiPas encore d'évaluation

- Profit PlanningDocument10 pagesProfit Planningsanjay parmarPas encore d'évaluation

- Maybank SR2015Document84 pagesMaybank SR2015de_stanszaPas encore d'évaluation

- TrueBridge Capital Partners State of The Venture Capital Industry 2018Document28 pagesTrueBridge Capital Partners State of The Venture Capital Industry 2018Joshua ElkingtonPas encore d'évaluation

- ConclusionDocument2 pagesConclusiondivya dawdaPas encore d'évaluation

- Chapter 1 Flashcards - QuizletDocument6 pagesChapter 1 Flashcards - QuizletyonasPas encore d'évaluation

- A Walk On The (Asian) Wild Side: James Chanos Kynikos AssociatesDocument24 pagesA Walk On The (Asian) Wild Side: James Chanos Kynikos AssociatessubflacherPas encore d'évaluation

- Lesson 1.1 Simple Interest Visual AidDocument13 pagesLesson 1.1 Simple Interest Visual AidJerald SamsonPas encore d'évaluation

- Buyback of SharesDocument32 pagesBuyback of SharesKARISHMAATA2Pas encore d'évaluation

- Financial Market Trader - Intern: Bearstreet Research and Analysis PVT LTD 1 - 6 Yrs Delhi NCRDocument2 pagesFinancial Market Trader - Intern: Bearstreet Research and Analysis PVT LTD 1 - 6 Yrs Delhi NCRCesar De JesusPas encore d'évaluation

- Introduction To Applied EconomicsDocument58 pagesIntroduction To Applied EconomicsGina Calling Danao100% (4)

- Chapter 7 - Forecasting Financial StatementsDocument23 pagesChapter 7 - Forecasting Financial Statementsamanthi gunarathna95Pas encore d'évaluation

- Chapter 21Document8 pagesChapter 21Huế ThùyPas encore d'évaluation

- Ex. 5-120-Statement of Financial Position ClassificationsDocument4 pagesEx. 5-120-Statement of Financial Position ClassificationsEli KrismayantiPas encore d'évaluation

- Motor Insurance Claims in IndiaDocument13 pagesMotor Insurance Claims in IndiaNagavyas KanugoviPas encore d'évaluation

- GS-China Real Estate DevelopersDocument10 pagesGS-China Real Estate DevelopersAaron ひろき ZhangPas encore d'évaluation