Vous aimerez peut-être aussi

- 1 Cost-Benefit Analysis - Concepts and Practice, 4 TH Ed. Boardman, Greenberg, Vining and Weimer. Test 1Document28 pages1 Cost-Benefit Analysis - Concepts and Practice, 4 TH Ed. Boardman, Greenberg, Vining and Weimer. Test 1Iulia Gabriela0% (1)

- Ielts Liz Essay IdeasDocument2 pagesIelts Liz Essay Ideasliya25% (4)

- Macro Macro Objectives - KEYDocument24 pagesMacro Macro Objectives - KEYRobin Kuo100% (1)

- Global Weekly Economic Update - Deloitte InsightsDocument8 pagesGlobal Weekly Economic Update - Deloitte InsightsSaba SiddiquiPas encore d'évaluation

- Kimberly - Economics Internal AssesmentDocument8 pagesKimberly - Economics Internal Assesmentkimberly.weynata.4055Pas encore d'évaluation

- MFM Jun 17 2011Document13 pagesMFM Jun 17 2011timurrsPas encore d'évaluation

- Fed YardeniDocument2 pagesFed Yardenipta123Pas encore d'évaluation

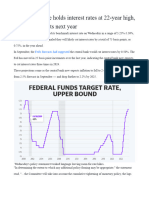

- 2023-12-13-Federal Reserve Holds Interest Rates at 22-Year High, Signals Three Cuts Next YearDocument3 pages2023-12-13-Federal Reserve Holds Interest Rates at 22-Year High, Signals Three Cuts Next YearAurel AchilPas encore d'évaluation

- WeatherDocument1 pageWeatherpathanfor786Pas encore d'évaluation

- Economy Shows Signs of Slowing, InfDocument1 pageEconomy Shows Signs of Slowing, Infandry rightPas encore d'évaluation

- Yellen Is Watching These Four Indicators For Signals On When To Raise RatesDocument4 pagesYellen Is Watching These Four Indicators For Signals On When To Raise RatesWei Hong TehPas encore d'évaluation

- Change in Fed StrategyDocument1 pageChange in Fed StrategyNeeraj GargPas encore d'évaluation

- First-Of-Its-Kind News ConferenceDocument11 pagesFirst-Of-Its-Kind News ConferenceKushal RastogiPas encore d'évaluation

- Christopher WallerDocument29 pagesChristopher WallerTim MoorePas encore d'évaluation

- Fed Slows Its Tightening With Quarter-Point Interest Rate Rise - WSJDocument6 pagesFed Slows Its Tightening With Quarter-Point Interest Rate Rise - WSJHassaan ImranPas encore d'évaluation

- Is This The Turning Point For Interest RatesDocument7 pagesIs This The Turning Point For Interest RatesJasmine MagdyPas encore d'évaluation

- (Q: Why Is Deflation Bad? A: Why Would You Buy Something If It Gets Cheaper Tomorrow)Document2 pages(Q: Why Is Deflation Bad? A: Why Would You Buy Something If It Gets Cheaper Tomorrow)Lian Wei ZhengPas encore d'évaluation

- Interest RatesDocument25 pagesInterest RatesMatthew KimPas encore d'évaluation

- Yellen HHDocument7 pagesYellen HHZerohedgePas encore d'évaluation

- The Fed's Dual Mandate Responsibilities and Challenges Facing U.S. Monetary Policy - Federal Reserve Bank of ChicagoDocument5 pagesThe Fed's Dual Mandate Responsibilities and Challenges Facing U.S. Monetary Policy - Federal Reserve Bank of ChicagoAlvaroPas encore d'évaluation

- FOMCpresconf20230503 PDFDocument4 pagesFOMCpresconf20230503 PDFJavierPas encore d'évaluation

- Federal Reserve Officials Are Keeping A Close Eye On Jobs DataDocument1 pageFederal Reserve Officials Are Keeping A Close Eye On Jobs DatafhriPas encore d'évaluation

- Fomc Pres Conf 20160615Document21 pagesFomc Pres Conf 20160615petere056Pas encore d'évaluation

- Powell 20221130Document16 pagesPowell 20221130Zerohedge100% (1)

- 2011-06-02 DBS Daily Breakfast SpreadDocument7 pages2011-06-02 DBS Daily Breakfast SpreadkjlaqiPas encore d'évaluation

- Monthly Economic Outlook 06082011Document6 pagesMonthly Economic Outlook 06082011jws_listPas encore d'évaluation

- FOMCpresconf 20220615Document27 pagesFOMCpresconf 20220615S CPas encore d'évaluation

- Here S How QuDocument4 pagesHere S How Qugcochin4Pas encore d'évaluation

- Fed's Powell Again Stresses Patience As U.S. Economy's 'Narrative' UnfoldsDocument2 pagesFed's Powell Again Stresses Patience As U.S. Economy's 'Narrative' UnfoldsAnthony JCPas encore d'évaluation

- JPM Market ReportDocument3 pagesJPM Market ReportDennis OhlssonPas encore d'évaluation

- FMR Special Report 2015-008 02-02-2015 GBDocument5 pagesFMR Special Report 2015-008 02-02-2015 GBMontasser KhelifiPas encore d'évaluation

- At Long Last, Inflation: By: Jens Erik Gould Published: May 12, 2014Document3 pagesAt Long Last, Inflation: By: Jens Erik Gould Published: May 12, 2014Theng RogerPas encore d'évaluation

- March 22, 2023 - Fed Chair Prepared RemarksDocument5 pagesMarch 22, 2023 - Fed Chair Prepared RemarksRam AhluwaliaPas encore d'évaluation

- Rise in US Core Inflation Highlights Stubborn Price PressuresDocument4 pagesRise in US Core Inflation Highlights Stubborn Price PressuresTrường Trường XuânPas encore d'évaluation

- Westpac - Fed Doves Might Have Last Word (August 2013)Document4 pagesWestpac - Fed Doves Might Have Last Word (August 2013)leithvanonselenPas encore d'évaluation

- The Pensford Letter - 06.01.2015Document4 pagesThe Pensford Letter - 06.01.2015Pensford FinancialPas encore d'évaluation

- Transcript of Chair Powell's Press Conference May 4, 2022Document24 pagesTranscript of Chair Powell's Press Conference May 4, 2022Learning的生活Pas encore d'évaluation

- The Pensford Letter - 4.21.14Document3 pagesThe Pensford Letter - 4.21.14Pensford FinancialPas encore d'évaluation

- Fomc Pres Conf 20231101Document26 pagesFomc Pres Conf 20231101Quynh Le Thi NhuPas encore d'évaluation

- Australia Inflation - Why Plenty of Heav... Ing Lies Ahead Despite Recent SlowdownDocument6 pagesAustralia Inflation - Why Plenty of Heav... Ing Lies Ahead Despite Recent SlowdownmxPas encore d'évaluation

- EC3073 WS2 Part 2Document1 pageEC3073 WS2 Part 2Antonin GonzalezPas encore d'évaluation

- FOMCpresconf 20230503Document25 pagesFOMCpresconf 20230503Edi SaputraPas encore d'évaluation

- Stock Market UnstableDocument2 pagesStock Market UnstableHiroaki KomatsuPas encore d'évaluation

- The Pensford Letter - 7.28.14Document3 pagesThe Pensford Letter - 7.28.14Pensford FinancialPas encore d'évaluation

- Is The Relationship Between Growth and in Ation Shifting?: Photo: Daniel Munoz/Getty ImagesDocument6 pagesIs The Relationship Between Growth and in Ation Shifting?: Photo: Daniel Munoz/Getty ImagesDiannaPas encore d'évaluation

- Weekly Trends March 20, 2015Document4 pagesWeekly Trends March 20, 2015dpbasicPas encore d'évaluation

- Leuthold 082013Document4 pagesLeuthold 082013alphathesisPas encore d'évaluation

- Weekly Economic Commentary 3/25/2013Document5 pagesWeekly Economic Commentary 3/25/2013monarchadvisorygroupPas encore d'évaluation

- Article EnglishDocument4 pagesArticle EnglishAnggoro BeePas encore d'évaluation

- FOMCpresconf 20230920Document4 pagesFOMCpresconf 20230920KHAIRULPas encore d'évaluation

- US Economic Outlook - For 2017 and BeyondDocument6 pagesUS Economic Outlook - For 2017 and BeyondpiyushPas encore d'évaluation

- The Pensford Letter - 12.9.13-1Document6 pagesThe Pensford Letter - 12.9.13-1Pensford FinancialPas encore d'évaluation

- Weekly Economic Commentary 3/18/2013Document7 pagesWeekly Economic Commentary 3/18/2013monarchadvisorygroupPas encore d'évaluation

- FOMCpresconf 20210922Document26 pagesFOMCpresconf 20210922marcoPas encore d'évaluation

- Federal Reserve Issues FOMC Statement: ShareDocument2 pagesFederal Reserve Issues FOMC Statement: ShareTREND_7425Pas encore d'évaluation

- Transcript of Chair Powell's Press Conference July 27, 2022Document26 pagesTranscript of Chair Powell's Press Conference July 27, 2022Psilocybe CubensisPas encore d'évaluation

- Week of November 7, 2022Document14 pagesWeek of November 7, 2022Steve PattrickPas encore d'évaluation

- Weekly Economic Commentary 07-30-2012Document4 pagesWeekly Economic Commentary 07-30-2012Jeremy A. MillerPas encore d'évaluation

- Fed Hikes 50bp With Much More To Come: Economic and Financial AnalysisDocument5 pagesFed Hikes 50bp With Much More To Come: Economic and Financial AnalysisOwm Close CorporationPas encore d'évaluation

- Fomc Pres Conf 20230614Document26 pagesFomc Pres Conf 20230614LAKHAN TRIVEDIPas encore d'évaluation

- Bernanke Faces InquisitionDocument17 pagesBernanke Faces InquisitionJeroen VandammePas encore d'évaluation

- Hike Now, Pay LaterDocument10 pagesHike Now, Pay LaterrexPas encore d'évaluation

- Map A Curricular Period OsDocument1 pageMap A Curricular Period OsJeniffer GuillenPas encore d'évaluation

- 02europe The UnreadyDocument2 pages02europe The UnreadyJeniffer GuillenPas encore d'évaluation

- Paris Slowly Coming To Terms With A New VulnerabilityDocument7 pagesParis Slowly Coming To Terms With A New VulnerabilityJeniffer GuillenPas encore d'évaluation

- Adm - Leading in The 21st CenturyDocument9 pagesAdm - Leading in The 21st CenturyJeniffer GuillenPas encore d'évaluation

- Bulletin OpendataDocument299 pagesBulletin OpendataTej PandyaPas encore d'évaluation

- 10 - Case - Econ08 - PPT - 27Document35 pages10 - Case - Econ08 - PPT - 27abu bakarPas encore d'évaluation

- Junior Worldmark Encyclopedia of The Nations Vol 1Document296 pagesJunior Worldmark Encyclopedia of The Nations Vol 1feritPas encore d'évaluation

- Unit 2 Urbanisation (Key)Document11 pagesUnit 2 Urbanisation (Key)Huy TranPas encore d'évaluation

- Grossman ModelDocument11 pagesGrossman ModelMarium Binte Aziz UrmiPas encore d'évaluation

- Technical EducationDocument44 pagesTechnical EducationLokuliyanaN100% (1)

- Capital As Power - Toward A New Cosmology of CapitalismDocument23 pagesCapital As Power - Toward A New Cosmology of Capitalismvidovdan9852Pas encore d'évaluation

- Interview Frank Martin 9.24.2018Document6 pagesInterview Frank Martin 9.24.2018mdorneanuPas encore d'évaluation

- Addressing Workers' Rights in The Textile and Apparel Industries: Consequences For The Bangladesh EconomyDocument15 pagesAddressing Workers' Rights in The Textile and Apparel Industries: Consequences For The Bangladesh EconomyAmna AroojPas encore d'évaluation

- HG-G10 Module 4 RTPDocument11 pagesHG-G10 Module 4 RTPCamille Lumontad Marco100% (2)

- The Effect of Unemployment On Economic Development in NigeriaDocument56 pagesThe Effect of Unemployment On Economic Development in Nigeriajamessabraham2Pas encore d'évaluation

- Understanding Labour Issues in Pakistan Dec 2009Document26 pagesUnderstanding Labour Issues in Pakistan Dec 2009عبداللہ عبداللہPas encore d'évaluation

- OECD - The Impact of AI On The Workplace SurveyDocument157 pagesOECD - The Impact of AI On The Workplace SurveyNOmePas encore d'évaluation

- Aft1023 Group 11Document10 pagesAft1023 Group 11Auni Arifah Binti Usaini A22A1000Pas encore d'évaluation

- Organisation Study On SHREE CEMENT, BEAWARDocument92 pagesOrganisation Study On SHREE CEMENT, BEAWARnitin_moyal88% (8)

- Globalisation RevisionDocument22 pagesGlobalisation RevisionLaura2611100% (2)

- E - Portfolio Assignment MacroDocument8 pagesE - Portfolio Assignment Macroapi-316969642Pas encore d'évaluation

- Swot Analysis Axis Iii (With SWOT Analysis of Sub Sectors: Rural Tourism, Craft and Traditional Local Products and Food)Document6 pagesSwot Analysis Axis Iii (With SWOT Analysis of Sub Sectors: Rural Tourism, Craft and Traditional Local Products and Food)Baskaran VarathanPas encore d'évaluation

- State of India's LivelihoodsDocument166 pagesState of India's LivelihoodsShreya KalePas encore d'évaluation

- Future of Work ReportDocument53 pagesFuture of Work ReportChristopher GavinPas encore d'évaluation

- The Natural Rate of Unemployment and The Phillips Curve: Prepared By: Fernando Quijano and Yvonn QuijanoDocument34 pagesThe Natural Rate of Unemployment and The Phillips Curve: Prepared By: Fernando Quijano and Yvonn QuijanoFerdinand MacolPas encore d'évaluation

- Employment, Migration, and UrbanizationDocument14 pagesEmployment, Migration, and UrbanizationAlzen Marie DelvoPas encore d'évaluation

- CsDocument2 pagesCsusamaumerPas encore d'évaluation

- The Financial Management of Minimum Wage Earners in Pulilan, Bulacan: An AnalysisDocument35 pagesThe Financial Management of Minimum Wage Earners in Pulilan, Bulacan: An AnalysisKrizel Ignacio100% (3)

- South Africa's Bold Priorities For Inclusive Growth McKinsey Global Institute Full ReportDocument164 pagesSouth Africa's Bold Priorities For Inclusive Growth McKinsey Global Institute Full Reporthh.deepakPas encore d'évaluation

- TUTMACDocument63 pagesTUTMACThùy Dương NguyễnPas encore d'évaluation

- Build Build Build Program of Duterte's AdministrationDocument6 pagesBuild Build Build Program of Duterte's AdministrationjohnnyPas encore d'évaluation