Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Guide To Documentary Credits: Fourth EditionDocument422 pagesGuide To Documentary Credits: Fourth EditionRomil 2015100% (2)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Problems CceDocument4 pagesProblems CceajkoywatanabeeexxPas encore d'évaluation

- BNK 214: Commercial Banking Operations: (Focus Area III)Document2 pagesBNK 214: Commercial Banking Operations: (Focus Area III)Suvash KhanalPas encore d'évaluation

- World Bank.Document22 pagesWorld Bank.Kashish GuptaPas encore d'évaluation

- DSSSB DOE PRT 2019.11.11, Shift 1 - 08.30AM - 10.30 PM, EnglishDocument46 pagesDSSSB DOE PRT 2019.11.11, Shift 1 - 08.30AM - 10.30 PM, EnglishDebasish GoraiPas encore d'évaluation

- FM Notes Unit 1Document21 pagesFM Notes Unit 1Himani ThakkerPas encore d'évaluation

- FULL Download Ebook PDF Introduction To Finance Markets Investments and Financial Management 15th Edition PDF EbookDocument41 pagesFULL Download Ebook PDF Introduction To Finance Markets Investments and Financial Management 15th Edition PDF Ebookdavid.conrad655100% (30)

- Floating Charge Advantages and DisadvantagesDocument5 pagesFloating Charge Advantages and DisadvantagesVitaraPas encore d'évaluation

- Your Financial Activities As of May 27, 2021Document3 pagesYour Financial Activities As of May 27, 2021Loan LoanPas encore d'évaluation

- BSP Circular No. 510 of 2006 Guidelines of Supervision by RiskDocument7 pagesBSP Circular No. 510 of 2006 Guidelines of Supervision by RiskE de GuiaPas encore d'évaluation

- RPR Format 2022Document84 pagesRPR Format 2022GodFatherPas encore d'évaluation

- Bank Frauds and Role of RBI - Taxguru - inDocument3 pagesBank Frauds and Role of RBI - Taxguru - inSamarth jhunjhunwalaPas encore d'évaluation

- Statement of account summaryDocument4 pagesStatement of account summaryShaikh MohammedPas encore d'évaluation

- Personal Finance Canadian Canadian 6th Edition Kapoor Test BankDocument8 pagesPersonal Finance Canadian Canadian 6th Edition Kapoor Test BankDrAnnaHubbardDVMitaj100% (34)

- Project ReportDocument95 pagesProject ReportPragya DixitPas encore d'évaluation

- Agricultural Loan Satisfaction Study of Kerala Gramin Bank CustomersDocument7 pagesAgricultural Loan Satisfaction Study of Kerala Gramin Bank Customerskrishnatradingcompany udtPas encore d'évaluation

- Topic 5 Accounting For PartnershipsDocument56 pagesTopic 5 Accounting For Partnershipstwahirwajeanpierre50Pas encore d'évaluation

- Pages 55 Capital Market Operation FinalDocument38 pagesPages 55 Capital Market Operation FinalAakash SharmaPas encore d'évaluation

- Payment Methods - Cheques: Clearing SystemDocument2 pagesPayment Methods - Cheques: Clearing SystemCephas PanguisaPas encore d'évaluation

- Telenor Microfinance Bank Limited - NORTH REGIONDocument2 pagesTelenor Microfinance Bank Limited - NORTH REGIONAhmad H.Pas encore d'évaluation

- 4NI20CS104 SklitaDocument12 pages4NI20CS104 SklitaSandeep HangaragiPas encore d'évaluation

- Blueprint MODECORDocument70 pagesBlueprint MODECORsrinivasPas encore d'évaluation

- HDFC Bank Was Amongst The First To Receive An PDFDocument83 pagesHDFC Bank Was Amongst The First To Receive An PDFSairam SajanePas encore d'évaluation

- The Crypto OTC Market at A Glance - v5Document3 pagesThe Crypto OTC Market at A Glance - v5Abra ChakraPas encore d'évaluation

- RKG Accounts (XI) CH 9 To 16 SolDocument3 pagesRKG Accounts (XI) CH 9 To 16 SolJohn WickPas encore d'évaluation

- Home Electricity Bill PaymentDocument1 pageHome Electricity Bill PaymentDivision3 CGST SuratPas encore d'évaluation

- Merger of HDFC and Centurion Bank of Punjab Motives and Deal StructureDocument2 pagesMerger of HDFC and Centurion Bank of Punjab Motives and Deal Structureanant ashwaryaPas encore d'évaluation

- Foundations of Finance Session 1: Prof. Udayan SharmaDocument23 pagesFoundations of Finance Session 1: Prof. Udayan SharmaSACHIN KUMARPas encore d'évaluation

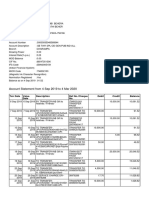

- Account Statement From 4 Sep 2019 To 4 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 pagesAccount Statement From 4 Sep 2019 To 4 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChiranjibi Behera ChiruPas encore d'évaluation

- Recent Measures To Tackle NPADocument3 pagesRecent Measures To Tackle NPAJyotiPas encore d'évaluation