Vous aimerez peut-être aussi

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachD'EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachÉvaluation : 3 sur 5 étoiles3/5 (3)

- Mastering Financial Modeling: A Professional’s Guide to Building Financial Models in ExcelD'EverandMastering Financial Modeling: A Professional’s Guide to Building Financial Models in ExcelÉvaluation : 5 sur 5 étoiles5/5 (8)

- Valuation Spreadsheet DCFDocument8 pagesValuation Spreadsheet DCFHilal MilmoPas encore d'évaluation

- LBO Excel ModelDocument6 pagesLBO Excel Modelrf_1238100% (2)

- Investment Banking LBO ModelDocument4 pagesInvestment Banking LBO Modelkirihara95100% (1)

- DCF Valuation ModelDocument25 pagesDCF Valuation Modelgwheinen100% (2)

- Finance Modeling LabDocument1 400 pagesFinance Modeling LabPradeep Krishnan86% (7)

- Full Merger Model Kraft-Kellogg - ShellDocument9 pagesFull Merger Model Kraft-Kellogg - ShellGeorgi VankovPas encore d'évaluation

- Investment Banking: Valuation, Leveraged Buyouts, and Mergers & AcquisitionsDocument22 pagesInvestment Banking: Valuation, Leveraged Buyouts, and Mergers & Acquisitionsaleaf92100% (1)

- Facebook - DCF ValuationDocument9 372 pagesFacebook - DCF ValuationDibyajyoti Oja0% (2)

- Axial Discounted Cash Flow Valuation CalculatorDocument4 pagesAxial Discounted Cash Flow Valuation CalculatorUdit AgrawalPas encore d'évaluation

- LBO Model - ValuationDocument6 pagesLBO Model - ValuationsashaathrgPas encore d'évaluation

- McKinsey Valuation DCF ModelDocument18 pagesMcKinsey Valuation DCF Modelnsksharma46% (13)

- DCF Analysis CompletedDocument8 pagesDCF Analysis Completedjason_imperial100% (1)

- Private Equity Buy Side Financial Model and ValuationDocument19 pagesPrivate Equity Buy Side Financial Model and ValuationBhaskar Shanmugam100% (3)

- Excel Spreadsheet For Mergers and Acquisitions ValuationDocument6 pagesExcel Spreadsheet For Mergers and Acquisitions Valuationisomiddinov100% (2)

- DCF Analysis JBDocument10 pagesDCF Analysis JBNoah100% (3)

- LBO Test - 75Document84 pagesLBO Test - 75conc880% (1)

- DCF ModelDocument6 pagesDCF ModelKatherine ChouPas encore d'évaluation

- Complete Private Equity ModelDocument16 pagesComplete Private Equity ModelMichel MaryanovichPas encore d'évaluation

- Equity Valuation DCFDocument28 pagesEquity Valuation DCFpriyarajan26100% (1)

- Equity ValuationDocument2 424 pagesEquity ValuationMuteeb Raina0% (1)

- LBO Sensitivity Tables BeforeDocument37 pagesLBO Sensitivity Tables BeforeMamadouB100% (2)

- PWC Financial ModelDocument92 pagesPWC Financial Modelw_fib100% (1)

- Financial Model (Solera Holdings Inc.)Document7 pagesFinancial Model (Solera Holdings Inc.)Hongrui (Henry) Chen0% (1)

- Introduction To Business Valuation: February 2013Document66 pagesIntroduction To Business Valuation: February 2013Nguyen Hoang Phuong100% (3)

- Pitchbook US TemplateDocument26 pagesPitchbook US TemplateBrian Heiligenthal100% (1)

- 107 09 IPO Valuation ModelDocument8 pages107 09 IPO Valuation ModelAnirban Bera100% (1)

- Merger Model - Blank Template: Control Panel Outputs Sensitivities Model Comps Data Diluted Shares CalculationDocument49 pagesMerger Model - Blank Template: Control Panel Outputs Sensitivities Model Comps Data Diluted Shares CalculationGugaPas encore d'évaluation

- Merger ModelDocument8 pagesMerger ModelStuti BansalPas encore d'évaluation

- AAPL DCF ValuationDocument12 pagesAAPL DCF ValuationthesaneinvestorPas encore d'évaluation

- Wall Street Prep DCF Financial ModelingDocument7 pagesWall Street Prep DCF Financial ModelingJack Jacinto100% (1)

- $ in Millions, Except Per Share DataDocument59 pages$ in Millions, Except Per Share DataTom HoughPas encore d'évaluation

- Simple LBO ModelDocument14 pagesSimple LBO ModelProfessorAsim Kumar MishraPas encore d'évaluation

- Gymboree LBO Model ComDocument7 pagesGymboree LBO Model ComrolandsudhofPas encore d'évaluation

- LBO Analysis TemplateDocument11 pagesLBO Analysis TemplateBobby Watkins75% (4)

- LBO Model Template - PE Course (Spring 08)Document18 pagesLBO Model Template - PE Course (Spring 08)chasperbrown100% (11)

- Apple LBO ModelDocument34 pagesApple LBO ModelShawn PantophletPas encore d'évaluation

- IB Merger ModelDocument12 pagesIB Merger Modelkirihara95100% (1)

- FCFF Vs FCFE Valuation ModelDocument5 pagesFCFF Vs FCFE Valuation Modelksivakumar09Pas encore d'évaluation

- Financial Model of Zynga IPODocument76 pagesFinancial Model of Zynga IPOJack Macharla100% (1)

- Core Lbo ModelDocument25 pagesCore Lbo Modelsalman_schonPas encore d'évaluation

- Pitch BookDocument80 pagesPitch Bookmmihai1100% (1)

- LBO Valuation Model 1 ProtectedDocument14 pagesLBO Valuation Model 1 ProtectedYap Thiah HuatPas encore d'évaluation

- McKinsey DCF Valuation 2005 User GuideDocument16 pagesMcKinsey DCF Valuation 2005 User GuideMichel KropfPas encore d'évaluation

- Valuation+in+the+Context+of+a+Restructuring+ (3 23 10)Document53 pagesValuation+in+the+Context+of+a+Restructuring+ (3 23 10)aniketparikh3100% (1)

- LBO Valuation Model PDFDocument101 pagesLBO Valuation Model PDFAbhishek Singh100% (3)

- LBO Model - TemplateDocument9 pagesLBO Model - TemplateByron FanPas encore d'évaluation

- Investment ValuationDocument11 pagesInvestment Valuationcontact7809Pas encore d'évaluation

- Financial Model-Mega BrandDocument4 pagesFinancial Model-Mega BrandHongrui (Henry) Chen100% (1)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelD'Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelPas encore d'évaluation

- Applied Corporate Finance. What is a Company worth?D'EverandApplied Corporate Finance. What is a Company worth?Évaluation : 3 sur 5 étoiles3/5 (2)

- Critical Financial Review: Understanding Corporate Financial InformationD'EverandCritical Financial Review: Understanding Corporate Financial InformationPas encore d'évaluation

- Summary of Joshua Rosenbaum & Joshua Pearl's Investment BankingD'EverandSummary of Joshua Rosenbaum & Joshua Pearl's Investment BankingPas encore d'évaluation

- A Pragmatist’s Guide to Leveraged Finance: Credit Analysis for Below-Investment-Grade Bonds and LoansD'EverandA Pragmatist’s Guide to Leveraged Finance: Credit Analysis for Below-Investment-Grade Bonds and LoansÉvaluation : 5 sur 5 étoiles5/5 (1)

- Lessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial Policies, and ValuationD'EverandLessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial Policies, and ValuationPas encore d'évaluation

- Mergers and Acquisitions Basics: The Key Steps of Acquisitions, Divestitures, and InvestmentsD'EverandMergers and Acquisitions Basics: The Key Steps of Acquisitions, Divestitures, and InvestmentsPas encore d'évaluation

- Private Equity Value Creation Analysis: Volume I: Theory: A Technical Handbook for the Analysis of Private Companies and PortfoliosD'EverandPrivate Equity Value Creation Analysis: Volume I: Theory: A Technical Handbook for the Analysis of Private Companies and PortfoliosPas encore d'évaluation

- The Art of Company Valuation and Financial Statement Analysis: A Value Investor's Guide with Real-life Case StudiesD'EverandThe Art of Company Valuation and Financial Statement Analysis: A Value Investor's Guide with Real-life Case StudiesÉvaluation : 4 sur 5 étoiles4/5 (10)

- Company Valuation Under IFRS - 3rd edition: Interpreting and forecasting accounts using International Financial Reporting StandardsD'EverandCompany Valuation Under IFRS - 3rd edition: Interpreting and forecasting accounts using International Financial Reporting StandardsPas encore d'évaluation

- Hawk ElectronicsDocument3 pagesHawk ElectronicsHilal Milmo0% (1)

- Fund PerformanceDocument13 pagesFund PerformanceHilal MilmoPas encore d'évaluation

- M&a IT Service SectorsDocument60 pagesM&a IT Service SectorsHilal MilmoPas encore d'évaluation

- Information Memorandum: $1,775m and 250m Senior Secured Credit FacilitiesDocument81 pagesInformation Memorandum: $1,775m and 250m Senior Secured Credit FacilitiesHilal MilmoPas encore d'évaluation

- Sample Bank Modeling TemplateDocument49 pagesSample Bank Modeling TemplaterajsalgyanPas encore d'évaluation

- (Intl Investment) Chapter 1 - InvestmentDocument49 pages(Intl Investment) Chapter 1 - InvestmentJane VickyPas encore d'évaluation

- 2016 Bar ExaminationsDocument37 pages2016 Bar ExaminationsPingotMagangaPas encore d'évaluation

- A. Risks and Rates of ReturnDocument74 pagesA. Risks and Rates of ReturnJuna Rose MamarilPas encore d'évaluation

- Kuhn Trading With The Cup With HandleDocument7 pagesKuhn Trading With The Cup With HandlebengaltigerPas encore d'évaluation

- Accf 2204Document7 pagesAccf 2204Avi StrikyPas encore d'évaluation

- Tugas Manajemen Keuangan IIDocument8 pagesTugas Manajemen Keuangan IIL RakkimanPas encore d'évaluation

- Strategic Management and Strategic Competitiveness: Knowledge ObjectivesDocument23 pagesStrategic Management and Strategic Competitiveness: Knowledge ObjectivessuriakumaranPas encore d'évaluation

- BankingDocument68 pagesBankingK59 Nguyen Thi Thu HaPas encore d'évaluation

- Performance ManagementDocument19 pagesPerformance ManagementSigei Leonard100% (2)

- Tpbank Annual Report 2014Document44 pagesTpbank Annual Report 2014Stella NguyenPas encore d'évaluation

- Presentation ON Cash Management OF Ans Steel Tubes Ltd. (JBM Group)Document23 pagesPresentation ON Cash Management OF Ans Steel Tubes Ltd. (JBM Group)soniaPas encore d'évaluation

- CFA1 (2011) Corporate FinanceDocument9 pagesCFA1 (2011) Corporate FinancenilakashPas encore d'évaluation

- Brand Valuation ApproachDocument17 pagesBrand Valuation ApproachSam_nitkPas encore d'évaluation

- Project AppraisalDocument3 pagesProject AppraisalnailwalnamitaPas encore d'évaluation

- Northern Trust Company - 30.08.20Document64 pagesNorthern Trust Company - 30.08.20Danijel DjordjicPas encore d'évaluation

- Trading Journal 10 Pips + Money ManagementDocument6 pagesTrading Journal 10 Pips + Money ManagementmmPas encore d'évaluation

- JohnsonDocument12 pagesJohnsonJannah Victoria AmoraPas encore d'évaluation

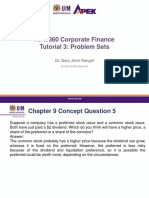

- Tutorial 3 Problem Set Answers - FinalDocument19 pagesTutorial 3 Problem Set Answers - FinalHello100% (1)

- Presentation 4 - Basics of Capital Budgeting (Draft)Document27 pagesPresentation 4 - Basics of Capital Budgeting (Draft)sanjuladasanPas encore d'évaluation

- Coach Gruden's Trading Playbook:: "If YOU Are Not Succeeding, WE Are Not Happy"Document20 pagesCoach Gruden's Trading Playbook:: "If YOU Are Not Succeeding, WE Are Not Happy"Sebastian100% (2)

- Schedule of Assessment Programs Fees Infinity Forex Funds V5Document14 pagesSchedule of Assessment Programs Fees Infinity Forex Funds V5newalbertblkyanPas encore d'évaluation

- Risk ManagementDocument57 pagesRisk ManagementAvtaar SinghPas encore d'évaluation

- A Comparative Performance Analysis of Conventional and Islamic Exchange-Traded FundsDocument11 pagesA Comparative Performance Analysis of Conventional and Islamic Exchange-Traded FundsTijjani Ridwanulah AdewalePas encore d'évaluation

- Intermediate Accounting RTP May 20Document44 pagesIntermediate Accounting RTP May 20Durgadevi BaskaranPas encore d'évaluation

- ResumeDocument4 pagesResumeapi-3826517Pas encore d'évaluation

- 2022 - Strategic Management 731 - CA Test 2 Review QuestionsDocument19 pages2022 - Strategic Management 731 - CA Test 2 Review QuestionsMaria LettaPas encore d'évaluation

- Understanding Single Period Chart Patterns: Hantec Research Webinars - Technical Analysis SeriesDocument6 pagesUnderstanding Single Period Chart Patterns: Hantec Research Webinars - Technical Analysis Seriessaran21Pas encore d'évaluation

- Unit 1 Role of Financial Institutions and MarketsDocument11 pagesUnit 1 Role of Financial Institutions and MarketsGalijang ShampangPas encore d'évaluation

- Individual Assignment Bui Van Thanh MMDocument9 pagesIndividual Assignment Bui Van Thanh MMThanh BuiPas encore d'évaluation

- IS Definitions v2Document13 pagesIS Definitions v2Ajith VPas encore d'évaluation