Vous aimerez peut-être aussi

- Term Paper On Inventory Control Techniques: Nikhil Ratnakaran 1PT11MBA35 Section BDocument12 pagesTerm Paper On Inventory Control Techniques: Nikhil Ratnakaran 1PT11MBA35 Section BNikhil RatnakaranPas encore d'évaluation

- Research Methodology: 5. Systematic Literature Review (SLR)Document55 pagesResearch Methodology: 5. Systematic Literature Review (SLR)karimPas encore d'évaluation

- BSBCMM401 Assessment Task 2Document10 pagesBSBCMM401 Assessment Task 2장위Pas encore d'évaluation

- IC WBS With Gantt Chart Template 8721Document8 pagesIC WBS With Gantt Chart Template 8721Shidqi PranitiPas encore d'évaluation

- Bsbrsk501b - Manage Risk-Tables.2Document11 pagesBsbrsk501b - Manage Risk-Tables.2bacharnaja50% (2)

- Assessment Brief Law of TortsDocument6 pagesAssessment Brief Law of TortsHossain Ali Al-RaziPas encore d'évaluation

- Ictict517 V3Document80 pagesIctict517 V3manpreet kaurPas encore d'évaluation

- Vpgict SupersededDocument75 pagesVpgict Superseded______.________0% (3)

- BSBMGT502 Resources Task 4 - Performance Review AssessmentDocument7 pagesBSBMGT502 Resources Task 4 - Performance Review AssessmentWai Man LeePas encore d'évaluation

- Database Case Study ReportDocument14 pagesDatabase Case Study ReportGabriel ZuanettiPas encore d'évaluation

- Cost Concepts: By: Akshat. D. YadavDocument14 pagesCost Concepts: By: Akshat. D. YadavyadavakshatPas encore d'évaluation

- ICTSAS509: Provide Client Ict Support ServicesDocument10 pagesICTSAS509: Provide Client Ict Support Servicesmanpreet kaurPas encore d'évaluation

- Ingredients Recipe Quantity (EP) Cost Total Cost Ingredients Recipe Quantity (EP) Cost Total Cost Weight Count APC/Unit Yield % EPC/UnitDocument2 pagesIngredients Recipe Quantity (EP) Cost Total Cost Ingredients Recipe Quantity (EP) Cost Total Cost Weight Count APC/Unit Yield % EPC/UnitRyannePas encore d'évaluation

- Sitxccs007 Enhance Customer Service Experience: How Social Media Affect The Hospitality Industry?Document5 pagesSitxccs007 Enhance Customer Service Experience: How Social Media Affect The Hospitality Industry?Anonymous 2WDolSOGGPas encore d'évaluation

- Assessment Task 2: Risk Management Project: Carefully Read The FollowingDocument5 pagesAssessment Task 2: Risk Management Project: Carefully Read The FollowingOhms BrangueloPas encore d'évaluation

- Lecture Assessment 1 Knowledge Test & Case Study: Unit: BSBMGT617 Develop and Implement A Business Plan QualificationDocument14 pagesLecture Assessment 1 Knowledge Test & Case Study: Unit: BSBMGT617 Develop and Implement A Business Plan QualificationPukpui Pui100% (1)

- 1 UderstandDocument23 pages1 UderstandVanushaPas encore d'évaluation

- MIS604 Assessment 2 Brief ELINK-converted ElinkDocument8 pagesMIS604 Assessment 2 Brief ELINK-converted ElinkZouh BharatPas encore d'évaluation

- BSB30115 MappingDocument27 pagesBSB30115 MappingBronwyn BlencowePas encore d'évaluation

- Paramjit Kaur: A) Supply Chain, Procurement and Purchasing?:-It Involves The Tasks and Functions WhichDocument6 pagesParamjit Kaur: A) Supply Chain, Procurement and Purchasing?:-It Involves The Tasks and Functions WhichHarkamal singhPas encore d'évaluation

- ComplexDocuments - ASS 3Document6 pagesComplexDocuments - ASS 3Renan Candura Dela LiberaPas encore d'évaluation

- Assessment Task 3 InstructionsDocument2 pagesAssessment Task 3 InstructionsVanessa May Sandoval0% (2)

- AssignmentDocument13 pagesAssignmentGRACE100% (1)

- Assessment 3Document21 pagesAssessment 3manpreet kaurPas encore d'évaluation

- Imt 56Document4 pagesImt 56Nothing786Pas encore d'évaluation

- Rick Assignment 1 LargeDocument5 pagesRick Assignment 1 LargeNeeraj KumarPas encore d'évaluation

- Unit Assessment - ICTICT509 - Gather Data To Identify Business RequirementsDocument44 pagesUnit Assessment - ICTICT509 - Gather Data To Identify Business RequirementsManawPas encore d'évaluation

- Assessment-Task-1 ICTICT608Document9 pagesAssessment-Task-1 ICTICT608RameshPas encore d'évaluation

- AssessmentDocument38 pagesAssessmentsupriya waglePas encore d'évaluation

- BSBSTR601 Simulation Pack V3Document17 pagesBSBSTR601 Simulation Pack V3Accounts AccountsPas encore d'évaluation

- Managing ICT Solutions A2Document7 pagesManaging ICT Solutions A2pablo Sandoval100% (1)

- Case Study PresentationDocument11 pagesCase Study PresentationAman Sharma100% (1)

- Gross MarginDocument4 pagesGross MarginMihalis AristidouPas encore d'évaluation

- MB0052 - Solved Q.-4 To 6Document4 pagesMB0052 - Solved Q.-4 To 6Ankur BhavsarPas encore d'évaluation

- BSBTEC303 Project PortfolioDocument32 pagesBSBTEC303 Project PortfolioJulia BaiandinaPas encore d'évaluation

- Manage Budgets and Financial PlansDocument23 pagesManage Budgets and Financial PlansMonique BugePas encore d'évaluation

- BSBINM501 Manage An Information or Knowledge Management SystemDocument5 pagesBSBINM501 Manage An Information or Knowledge Management SystemajayPas encore d'évaluation

- BSBINM601 Assessment Task 1Document3 pagesBSBINM601 Assessment Task 1Kathleen RamientoPas encore d'évaluation

- 502 AssignmentDocument22 pages502 AssignmentSyed Bilal Ali0% (2)

- ICTICT517 SW 1of1Document62 pagesICTICT517 SW 1of1Ashutosh MaharajPas encore d'évaluation

- ICTv2 Implementation Guide - DraftDocument156 pagesICTv2 Implementation Guide - Draft______.________Pas encore d'évaluation

- A. Accredited Course or Training Package B. QualificationDocument1 pageA. Accredited Course or Training Package B. QualificationSittaraPas encore d'évaluation

- Customer Analysis: Customer Service and Research SkillsDocument11 pagesCustomer Analysis: Customer Service and Research SkillsAKRA RACHURIPas encore d'évaluation

- Evaluate Marketing Opportunities Submission DetailsDocument16 pagesEvaluate Marketing Opportunities Submission DetailsanushaPas encore d'évaluation

- Maria Paula MARTINEZ HERRERA - Answers - BSBRES411 - RESUBMISSIONDocument32 pagesMaria Paula MARTINEZ HERRERA - Answers - BSBRES411 - RESUBMISSIONPaula Martinez100% (1)

- Bsbwhs401 (Topic 3b-3d)Document37 pagesBsbwhs401 (Topic 3b-3d)robinkwok69100% (2)

- FNSACC408 LG F v1.0Document100 pagesFNSACC408 LG F v1.0Hongxiao ZhuPas encore d'évaluation

- Charter TemplateDocument11 pagesCharter Templatedeli_pedro_xPas encore d'évaluation

- Mondelez: Sales and Distribution ReportDocument17 pagesMondelez: Sales and Distribution ReportSaumya MittalPas encore d'évaluation

- System Design 903952308BDocument30 pagesSystem Design 903952308BedymaradonaPas encore d'évaluation

- Assig 2Document29 pagesAssig 2vinayPas encore d'évaluation

- Task 1 - Bsbcus501Document7 pagesTask 1 - Bsbcus501Phung KimPas encore d'évaluation

- Module Handbook - H7 BaMMDocument56 pagesModule Handbook - H7 BaMMAyesha IrumPas encore d'évaluation

- Assessment Task 1: Brief ReportDocument12 pagesAssessment Task 1: Brief ReportAshiqur Rahman100% (1)

- Lecture Assessment 1 Case Study and Projects-Group ActivitiesDocument25 pagesLecture Assessment 1 Case Study and Projects-Group ActivitiesHimanshuPas encore d'évaluation

- Assessment 2 BSBMGT517 - PerfomanceDocument20 pagesAssessment 2 BSBMGT517 - PerfomanceBoban GorgievPas encore d'évaluation

- BSBSMB401 RajbirDocument9 pagesBSBSMB401 RajbirsakshiPas encore d'évaluation

- Levels and Technique - Inventory ControlDocument6 pagesLevels and Technique - Inventory ControlMostafizul HaquePas encore d'évaluation

- Setting Up of Various Stock Levels: (A) Re-Ordering LevelDocument10 pagesSetting Up of Various Stock Levels: (A) Re-Ordering LevelAngelica Cinena GrajeraPas encore d'évaluation

- Inventory ControlDocument7 pagesInventory ControlDarshan RautPas encore d'évaluation

- Adbi wp1083Document43 pagesAdbi wp1083Armel PalerPas encore d'évaluation

- Adbi wp1083Document43 pagesAdbi wp1083Armel PalerPas encore d'évaluation

- AdromfdfdDocument1 pageAdromfdfdArmel PalerPas encore d'évaluation

- Rom 2018Document1 pageRom 2018Armel PalerPas encore d'évaluation

- Weg FRF 2Document2 pagesWeg FRF 2Armel PalerPas encore d'évaluation

- Jasc PP 202110Document1 pageJasc PP 202110Armel PalerPas encore d'évaluation

- Withholding Tax Table 1Document1 pageWithholding Tax Table 1Armel PalerPas encore d'évaluation

- Nose 3Document1 pageNose 3Armel PalerPas encore d'évaluation

- Eye 3Document1 pageEye 3Armel PalerPas encore d'évaluation

- There Is Sunshine in My Soul TodayDocument1 pageThere Is Sunshine in My Soul TodayArmel PalerPas encore d'évaluation

- Comp 2Document1 pageComp 2Armel PalerPas encore d'évaluation

- Comp 1Document1 pageComp 1Armel PalerPas encore d'évaluation

- Earth ScienceDocument2 pagesEarth ScienceArmel PalerPas encore d'évaluation

- Costing P160,000, The Decorticator Is Applicable in Small-Scale Commercial Production of Coconut Fiber and Dust. – Rudy ADocument1 pageCosting P160,000, The Decorticator Is Applicable in Small-Scale Commercial Production of Coconut Fiber and Dust. – Rudy AArmel PalerPas encore d'évaluation

- Nose 4Document1 pageNose 4Armel PalerPas encore d'évaluation

- Nose 2Document1 pageNose 2Armel PalerPas encore d'évaluation

- NoseDocument1 pageNoseArmel PalerPas encore d'évaluation

- Eye 5Document1 pageEye 5Armel PalerPas encore d'évaluation

- Eye 7Document1 pageEye 7Armel PalerPas encore d'évaluation

- EyeDocument1 pageEyeArmel PalerPas encore d'évaluation

- Eye 4Document1 pageEye 4Armel PalerPas encore d'évaluation

- Eye 6Document1 pageEye 6Armel PalerPas encore d'évaluation

- Eye 2Document1 pageEye 2Armel PalerPas encore d'évaluation

- Eye 3Document2 pagesEye 3Armel PalerPas encore d'évaluation

- Eye 2Document1 pageEye 2Armel PalerPas encore d'évaluation

- Negotiable Instruments LawDocument17 pagesNegotiable Instruments LawJeffrey Ranes Doloriel Mendoza-Paasa100% (1)

- How ToDocument1 pageHow ToArmel PalerPas encore d'évaluation

- AUDITINGDocument3 pagesAUDITINGSharn Linzi Buan MontañoPas encore d'évaluation

- Eye 3Document2 pagesEye 3Armel PalerPas encore d'évaluation

- Can The Bad Debt Expense BeDocument5 pagesCan The Bad Debt Expense BeMon Sour CalaunanPas encore d'évaluation

- Kunci Jawaban Jurnal PT JAYATAMA P3Document14 pagesKunci Jawaban Jurnal PT JAYATAMA P3sepriyadiPas encore d'évaluation

- CHAPTER 5 (Accounting For Service)Document26 pagesCHAPTER 5 (Accounting For Service)lc100% (1)

- Supply Chain SyllabusDocument4 pagesSupply Chain SyllabusProfessor MoladPas encore d'évaluation

- Abm 11Document19 pagesAbm 11Charishann PerolPas encore d'évaluation

- Tipo S Movimento SapDocument3 pagesTipo S Movimento Sapruiforever0% (1)

- Statement Current yEAR KotakDocument19 pagesStatement Current yEAR KotakRikshawala 420100% (1)

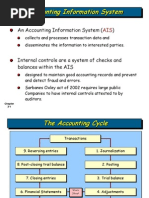

- Wiley - Chapter 3: The Accounting Information SystemDocument36 pagesWiley - Chapter 3: The Accounting Information SystemIvan BliminsePas encore d'évaluation

- Find Ur SelfDocument4 pagesFind Ur SelfMervixShasiPas encore d'évaluation

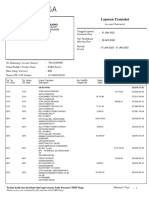

- Laporan Transaksi: Kepada / ToDocument3 pagesLaporan Transaksi: Kepada / Toridwan santosoPas encore d'évaluation

- Strategic ManagementDocument4 pagesStrategic Managementbhupesh joshi0% (1)

- Chapter 5Document12 pagesChapter 5?????0% (1)

- Name: Rowma Danielle Lactao Date Submitted: 1-28-22 Grade & Section: 10-Peace Teacher: Ms. Lizz DelosoDocument2 pagesName: Rowma Danielle Lactao Date Submitted: 1-28-22 Grade & Section: 10-Peace Teacher: Ms. Lizz DelosoRowma Danielle LactaoPas encore d'évaluation

- SampleNAB Statement X7819 26-Oct-2021Document10 pagesSampleNAB Statement X7819 26-Oct-2021Tobias PricePas encore d'évaluation

- 67 3 3 AccountancyDocument39 pages67 3 3 AccountancyHarman Singh SachdevaPas encore d'évaluation

- Loan Problems ResolutionDocument8 pagesLoan Problems ResolutionPrithwi NayakPas encore d'évaluation

- Homework P4 4ADocument8 pagesHomework P4 4AFrizky Triputra CahyahanaPas encore d'évaluation

- Principle of Accounting 1Document25 pagesPrinciple of Accounting 1Quỳnh Trang NguyễnPas encore d'évaluation

- Entry Journal PT CahayaDocument11 pagesEntry Journal PT CahayaayuafrizadestaPas encore d'évaluation

- Teresita Buenaflor Shoes Worksheet 1 RegineDocument24 pagesTeresita Buenaflor Shoes Worksheet 1 RegineBaby Babe100% (1)

- Fundamentals of Accountancy, Business and Management 1 (FABM 1)Document10 pagesFundamentals of Accountancy, Business and Management 1 (FABM 1)Angelica ParasPas encore d'évaluation

- CH 1 Introduction To Accounting and Business IndDocument45 pagesCH 1 Introduction To Accounting and Business IndUnggul Nuswantoro AjiPas encore d'évaluation

- Odoo Feature List PDFDocument2 pagesOdoo Feature List PDFRejoy Radhakrishnan0% (1)

- Module 2 - Bank ReconciliationDocument21 pagesModule 2 - Bank ReconciliationJennalyn S. GanalonPas encore d'évaluation

- Personal Assignment Week 4-GovernDocument6 pagesPersonal Assignment Week 4-GoverndivaPas encore d'évaluation

- Installments SalesDocument21 pagesInstallments Salesbekbek12Pas encore d'évaluation

- A) B) C) D) E) A) B) C) D) E) A) B) C) D) E) A) B) C) D) E)Document3 pagesA) B) C) D) E) A) B) C) D) E) A) B) C) D) E) A) B) C) D) E)Mharvie LorayaPas encore d'évaluation

- Question Bank ACM - 301 - Principles of AuditingDocument14 pagesQuestion Bank ACM - 301 - Principles of AuditingkirtiinityaPas encore d'évaluation

- Usaa Receipt Sharecd7bcc1f 3817 4d83 Bae5 Bdb429ce1a15Document12 pagesUsaa Receipt Sharecd7bcc1f 3817 4d83 Bae5 Bdb429ce1a15Rohan DuncanPas encore d'évaluation

- Understanding The Supply ChainDocument34 pagesUnderstanding The Supply ChainNauryzbek MukhanovPas encore d'évaluation

- The Complete Guide to Building Your Own Home and Saving Thousands on Your New HouseD'EverandThe Complete Guide to Building Your Own Home and Saving Thousands on Your New HouseÉvaluation : 5 sur 5 étoiles5/5 (3)

- How to Estimate with RSMeans Data: Basic Skills for Building ConstructionD'EverandHow to Estimate with RSMeans Data: Basic Skills for Building ConstructionÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- A Place of My Own: The Architecture of DaydreamsD'EverandA Place of My Own: The Architecture of DaydreamsÉvaluation : 4 sur 5 étoiles4/5 (242)

- Building Physics -- Heat, Air and Moisture: Fundamentals and Engineering Methods with Examples and ExercisesD'EverandBuilding Physics -- Heat, Air and Moisture: Fundamentals and Engineering Methods with Examples and ExercisesPas encore d'évaluation

- The Complete HVAC BIBLE for Beginners: The Most Practical & Updated Guide to Heating, Ventilation, and Air Conditioning Systems | Installation, Troubleshooting and Repair | Residential & CommercialD'EverandThe Complete HVAC BIBLE for Beginners: The Most Practical & Updated Guide to Heating, Ventilation, and Air Conditioning Systems | Installation, Troubleshooting and Repair | Residential & CommercialPas encore d'évaluation

- Field Guide for Construction Management: Management by Walking AroundD'EverandField Guide for Construction Management: Management by Walking AroundÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- THE PROPTECH GUIDE: EVERYTHING YOU NEED TO KNOW ABOUT THE FUTURE OF REAL ESTATED'EverandTHE PROPTECH GUIDE: EVERYTHING YOU NEED TO KNOW ABOUT THE FUTURE OF REAL ESTATEÉvaluation : 4 sur 5 étoiles4/5 (1)

- Building Construction Technology: A Useful Guide - Part 1D'EverandBuilding Construction Technology: A Useful Guide - Part 1Évaluation : 4 sur 5 étoiles4/5 (3)

- 1,001 Questions & Answers for the CWI Exam: Welding Metallurgy and Visual Inspection Study GuideD'Everand1,001 Questions & Answers for the CWI Exam: Welding Metallurgy and Visual Inspection Study GuideÉvaluation : 3.5 sur 5 étoiles3.5/5 (7)

- Civil Engineer's Handbook of Professional PracticeD'EverandCivil Engineer's Handbook of Professional PracticeÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- Pressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedD'EverandPressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedÉvaluation : 5 sur 5 étoiles5/5 (1)

- Post Weld Heat Treatment PWHT: Standards, Procedures, Applications, and Interview Q&AD'EverandPost Weld Heat Treatment PWHT: Standards, Procedures, Applications, and Interview Q&APas encore d'évaluation

- The Complete Guide to Building With Rocks & Stone: Stonework Projects and Techniques Explained SimplyD'EverandThe Complete Guide to Building With Rocks & Stone: Stonework Projects and Techniques Explained SimplyÉvaluation : 4 sur 5 étoiles4/5 (1)

- Nuclear Energy in the 21st Century: World Nuclear University PressD'EverandNuclear Energy in the 21st Century: World Nuclear University PressÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- The Everything Woodworking Book: A Beginner's Guide To Creating Great Projects From Start To FinishD'EverandThe Everything Woodworking Book: A Beginner's Guide To Creating Great Projects From Start To FinishÉvaluation : 4 sur 5 étoiles4/5 (3)

- Real Life: Construction Management Guide from A-ZD'EverandReal Life: Construction Management Guide from A-ZÉvaluation : 4.5 sur 5 étoiles4.5/5 (4)

- Construction Project Management 101: For Beginners & New GraduatesD'EverandConstruction Project Management 101: For Beginners & New GraduatesPas encore d'évaluation

- Principles of Welding: Processes, Physics, Chemistry, and MetallurgyD'EverandPrinciples of Welding: Processes, Physics, Chemistry, and MetallurgyÉvaluation : 4 sur 5 étoiles4/5 (1)

- Shipping Container Homes: How to build a shipping container home, including plans, cool ideas, and more!D'EverandShipping Container Homes: How to build a shipping container home, including plans, cool ideas, and more!Pas encore d'évaluation

- Practical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsD'EverandPractical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsÉvaluation : 3.5 sur 5 étoiles3.5/5 (3)