Vous aimerez peut-être aussi

- Works Contract - Concept and ValuationDocument31 pagesWorks Contract - Concept and ValuationArun AroraPas encore d'évaluation

- As 22 Accounting For Taxes On IncomeDocument34 pagesAs 22 Accounting For Taxes On IncomeArun AroraPas encore d'évaluation

- Strategy Execution Exemplar Balanced Score CardDocument2 pagesStrategy Execution Exemplar Balanced Score CardArun AroraPas encore d'évaluation

- 10 Causes For Low Strength in ConcreteDocument17 pages10 Causes For Low Strength in ConcreteTatineni RaviPas encore d'évaluation

- Annual ReportDocument115 pagesAnnual ReportArun AroraPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- 02 PDF MergedDocument36 pages02 PDF MergedarpanPas encore d'évaluation

- How To Find If A Wage Type Is Taxable or Not - SAP Q&ADocument4 pagesHow To Find If A Wage Type Is Taxable or Not - SAP Q&AMurali MohanPas encore d'évaluation

- Top 500 Taxpayers in The Philippines 2011Document10 pagesTop 500 Taxpayers in The Philippines 2011Mykiru IsyuseroPas encore d'évaluation

- Mindanao I Geothermal Partnership vs. Commissioner of Internal Revenue, 844 SCRA 386, November 08, 2017Document12 pagesMindanao I Geothermal Partnership vs. Commissioner of Internal Revenue, 844 SCRA 386, November 08, 2017Vida MariePas encore d'évaluation

- SA2 TAXATION Part 1Document7 pagesSA2 TAXATION Part 1Blythe teckPas encore d'évaluation

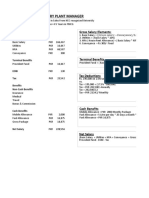

- Shoe Factory Plant Manager: Gross Salary ElementsDocument2 pagesShoe Factory Plant Manager: Gross Salary ElementsSukaina SalmanPas encore d'évaluation

- Prescriptive RulesDocument15 pagesPrescriptive Ruleslizherrero100% (3)

- PreviewDocument5 pagesPreviewFaz AliPas encore d'évaluation

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 517477100200619 Assessment Year: 2019-20Document6 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 517477100200619 Assessment Year: 2019-20SRIRAM DUTTAPas encore d'évaluation

- 20 - 22 September 2007. Chennai, India.: The 6th EditionDocument10 pages20 - 22 September 2007. Chennai, India.: The 6th EditionkavenindiaPas encore d'évaluation

- Wise Ltd. 56 Shoreditch High Street London E1 6JJ United KingdomDocument1 pageWise Ltd. 56 Shoreditch High Street London E1 6JJ United KingdomA VPas encore d'évaluation

- Unlimited VCC Method PDFDocument9 pagesUnlimited VCC Method PDFAzren Dino100% (3)

- Appendix 43 - CDRegDocument2 pagesAppendix 43 - CDRegSta. Maria ESPas encore d'évaluation

- US Internal Revenue Service: f6198 - 1999Document1 pageUS Internal Revenue Service: f6198 - 1999IRSPas encore d'évaluation

- VIMAL KUMAR Mumbai AdaniDocument1 pageVIMAL KUMAR Mumbai AdaniDHANU DANGIPas encore d'évaluation

- India Payslip May 2021Document1 pageIndia Payslip May 2021Talla KaseeswarPas encore d'évaluation

- Compensation IncomeDocument5 pagesCompensation IncomePaula Mae Dacanay100% (1)

- Module 11 - Fringe Benefit TaxDocument18 pagesModule 11 - Fringe Benefit TaxJANELLE NUEZPas encore d'évaluation

- Bitumen Price List Wef 20-04-2011 and 01-05-2011Document4 pagesBitumen Price List Wef 20-04-2011 and 01-05-2011Vizag Roads100% (1)

- Fee ChallanDocument1 pageFee ChallanManzoor HussainPas encore d'évaluation

- Singapore Withholding Tax Presented by Tax Accountants Pte LTDDocument2 pagesSingapore Withholding Tax Presented by Tax Accountants Pte LTDTax AccountantsPas encore d'évaluation

- Cash Aud Probs MCQDocument3 pagesCash Aud Probs MCQJane Ruby JennieferPas encore d'évaluation

- Procedure Text: "How To Calculate PPH 21"Document19 pagesProcedure Text: "How To Calculate PPH 21"nurul100% (1)

- 072) Parle Agro - Civil - Extra Work Qty - 3804Document4 pages072) Parle Agro - Civil - Extra Work Qty - 3804Vikrant KoulPas encore d'évaluation

- Ashutosh Sohil Salary 2020-03 PDFDocument1 pageAshutosh Sohil Salary 2020-03 PDFMohit Sharma100% (1)

- How To Log in To Your FRS Online AccountDocument4 pagesHow To Log in To Your FRS Online AccountSharan FosbinderPas encore d'évaluation

- Installment On CGT Subject To Mortgage2Document5 pagesInstallment On CGT Subject To Mortgage2Joneric RamosPas encore d'évaluation

- ContentServer Asp-3Document13 pagesContentServer Asp-3MPas encore d'évaluation

- PMHPANYD23020003Document2 pagesPMHPANYD23020003ashishPas encore d'évaluation

- Withdraw PayPal Money in Malaysia SolutionDocument16 pagesWithdraw PayPal Money in Malaysia Solutionafarz2604Pas encore d'évaluation