Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- 16 - Rahul Mundada - Mudita MathurDocument8 pages16 - Rahul Mundada - Mudita MathurRahul MundadaPas encore d'évaluation

- 1844 RulesDocument20 pages1844 RulestobymaoPas encore d'évaluation

- The Project in The Organizational StructureDocument28 pagesThe Project in The Organizational StructureThuỷ VươngPas encore d'évaluation

- Test 5-ConsolidationDocument3 pagesTest 5-ConsolidationAli OptimisticPas encore d'évaluation

- VU Accounting Lesson 22Document6 pagesVU Accounting Lesson 22ranawaseemPas encore d'évaluation

- Comm3201 Individual Case Study (June 2020)Document3 pagesComm3201 Individual Case Study (June 2020)Scarlett WangPas encore d'évaluation

- Personality Case StudyDocument2 pagesPersonality Case StudyShams Ul HayatPas encore d'évaluation

- Airtel - Store Manager (SM, JDDocument2 pagesAirtel - Store Manager (SM, JDAkshat JainPas encore d'évaluation

- Session-6 Prof. Muneza Kagzi T. A. Pai Management Institute (TAPMI)Document24 pagesSession-6 Prof. Muneza Kagzi T. A. Pai Management Institute (TAPMI)tanimaPas encore d'évaluation

- 11 Quality Management - FDocument15 pages11 Quality Management - FdumPas encore d'évaluation

- Creating New Market Space SlidesDocument28 pagesCreating New Market Space SlidesMuhammad Raffay MaqboolPas encore d'évaluation

- Online Demo Session - FICO - 14 April 2021Document48 pagesOnline Demo Session - FICO - 14 April 2021Md Mukul HossainPas encore d'évaluation

- Meaningful Employee Appraisal CommentsDocument6 pagesMeaningful Employee Appraisal CommentsM Son PhamPas encore d'évaluation

- Examples SMART GOALSDocument1 pageExamples SMART GOALSMinh TranPas encore d'évaluation

- Assignment of Labor and Organizational Management by Edris AbdellaDocument14 pagesAssignment of Labor and Organizational Management by Edris AbdellaEdris Abdella NuurePas encore d'évaluation

- ThesisDocument104 pagesThesisJerry B CruzPas encore d'évaluation

- The Effect of Digital Marketing On Purchasing Decisions: A Case Study in JordanDocument10 pagesThe Effect of Digital Marketing On Purchasing Decisions: A Case Study in JordanKristine DestorPas encore d'évaluation

- Assignment 1 Outline SuggestedDocument4 pagesAssignment 1 Outline SuggestedThùy TrangPas encore d'évaluation

- Annual Report 2011Document127 pagesAnnual Report 2011Nooreza PeerooPas encore d'évaluation

- P1 Exams Set ADocument10 pagesP1 Exams Set Aerica lamsenPas encore d'évaluation

- Nism 8 - Equity Derivatives - Test-1 - Last Day RevisionDocument54 pagesNism 8 - Equity Derivatives - Test-1 - Last Day RevisionAbhijeet Kumar100% (1)

- Chapter01.the Changing Role of Managerial Accounting in A Dynamic Business EnvironmentDocument62 pagesChapter01.the Changing Role of Managerial Accounting in A Dynamic Business EnvironmentAnjo Bautista Saip100% (1)

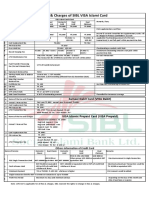

- Fees and Charges of SIBL Islami CardDocument1 pageFees and Charges of SIBL Islami CardMd YusufPas encore d'évaluation

- Blackrock Special Report - Inflation-Linked Bonds PrimerDocument8 pagesBlackrock Special Report - Inflation-Linked Bonds PrimerGreg JachnoPas encore d'évaluation

- CA IPCC Company Law Last Minute Revision Notes in PDF Format-3Document29 pagesCA IPCC Company Law Last Minute Revision Notes in PDF Format-3Naman JainPas encore d'évaluation

- Pelaksanaan Program Pembinaan Koperasi Usaha Mikro Kecil Dan Menengah (Umkm)Document7 pagesPelaksanaan Program Pembinaan Koperasi Usaha Mikro Kecil Dan Menengah (Umkm)Razief Firdaus 043Pas encore d'évaluation

- Auditing NotesDocument65 pagesAuditing NotesTushar GaurPas encore d'évaluation

- Financial Reporting and AnalysisDocument34 pagesFinancial Reporting and AnalysisNatasha AzzariennaPas encore d'évaluation

- High Income Skills - Elite IncomeDocument25 pagesHigh Income Skills - Elite IncomeSumaia AhmedPas encore d'évaluation

- Creating A Functional Process Control Configuration in HFMDocument3 pagesCreating A Functional Process Control Configuration in HFMDeva Raj0% (1)