Vous aimerez peut-être aussi

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideD'EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuidePas encore d'évaluation

- Glossary Final MDM PDFDocument17 pagesGlossary Final MDM PDFDeepak ShekhawatPas encore d'évaluation

- 10KSB Glossary 2016 - 2 - 1Document8 pages10KSB Glossary 2016 - 2 - 1Kevin TaboasPas encore d'évaluation

- Glossary of Financial TermsDocument3 pagesGlossary of Financial Termsmanishaamba7547Pas encore d'évaluation

- Acid Test: Hariapankti@yahoo - Co.inDocument14 pagesAcid Test: Hariapankti@yahoo - Co.inAbhijeet Bhaskar100% (1)

- Financial MGT TermsDocument14 pagesFinancial MGT TermsAmit KaushikPas encore d'évaluation

- Kamus Akuntansi PDFDocument17 pagesKamus Akuntansi PDFHapsara Bhanu AdhikaPas encore d'évaluation

- NikitaDocument28 pagesNikitaPradeep NaharPas encore d'évaluation

- Business Financial Terms - Definitions: Acid TestDocument11 pagesBusiness Financial Terms - Definitions: Acid Testaishwary rana100% (1)

- Finance TerminologyDocument14 pagesFinance TerminologyMustafa AyadPas encore d'évaluation

- Glossary of AccountingDocument8 pagesGlossary of AccountingSarbuland Khan LodhiPas encore d'évaluation

- Acc Imp Points 2Document10 pagesAcc Imp Points 2AnilisaPas encore d'évaluation

- DICCIONARY - Nayelis AmadorDocument28 pagesDICCIONARY - Nayelis AmadorNayelis AmadorPas encore d'évaluation

- Acid TestDocument45 pagesAcid TestMahendar Yash100% (1)

- Understand Basic Accounting TermsDocument5 pagesUnderstand Basic Accounting Termsabu taherPas encore d'évaluation

- Glossary AccountancyDocument20 pagesGlossary Accountancymohak vilechaPas encore d'évaluation

- Mercantile Basis AccountingDocument9 pagesMercantile Basis AccountingAshish SinghalPas encore d'évaluation

- Iprimed 1Document15 pagesIprimed 1mittakollusureshkrishna12345Pas encore d'évaluation

- Glossary of Fi Nancial TermsDocument11 pagesGlossary of Fi Nancial TermsArun VishnuPas encore d'évaluation

- AccountingDocument3 pagesAccountingchelsiereyes633Pas encore d'évaluation

- MBA Supplementary Resources Finance GlossaryDocument21 pagesMBA Supplementary Resources Finance GlossaryZoe ChimPas encore d'évaluation

- Glossary Accounts A To ZDocument8 pagesGlossary Accounts A To Zritvikjindal100% (1)

- Basic DefinitionsDocument5 pagesBasic DefinitionsHamza KhaliqPas encore d'évaluation

- BasicsDocument11 pagesBasicsMukesh MukiPas encore d'évaluation

- Finance Glossary: Study. Learn. ShareDocument9 pagesFinance Glossary: Study. Learn. ShareAditya RatnamPas encore d'évaluation

- Notes For Week 1Document7 pagesNotes For Week 1algokar999Pas encore d'évaluation

- Accounting NotesDocument3 pagesAccounting NotesMir TowfiqPas encore d'évaluation

- Income StatementDocument3 pagesIncome StatementPooja SreePas encore d'évaluation

- Midterm Cheat SheetDocument3 pagesMidterm Cheat SheetHiếuPas encore d'évaluation

- Apuntes AccountingDocument35 pagesApuntes AccountingPatricia Barquin DelgadoPas encore d'évaluation

- 15 Downstream Petroleum Economics GlossaryDocument43 pages15 Downstream Petroleum Economics GlossarySwahil TrigaPas encore d'évaluation

- MGT401 Short Notes Lec 1 - 45Document33 pagesMGT401 Short Notes Lec 1 - 45HRrehmanPas encore d'évaluation

- Topic 2: Glossary: FinanceDocument4 pagesTopic 2: Glossary: FinancechristianhawkinsPas encore d'évaluation

- Allowance For Bad Debts: Allowance Method Direct Write-Off MethodDocument5 pagesAllowance For Bad Debts: Allowance Method Direct Write-Off MethodChandradhari JhaPas encore d'évaluation

- Part 2 Accounting EquationDocument88 pagesPart 2 Accounting EquationDONALD GUTIERREZPas encore d'évaluation

- Hospitality Industry Accounting GlossaryDocument26 pagesHospitality Industry Accounting GlossaryKathy Holcomb CraigPas encore d'évaluation

- MG T 401 Short Notes by Khalid BilalDocument33 pagesMG T 401 Short Notes by Khalid BilalhayyaPas encore d'évaluation

- Financial Accounting GlossaryDocument5 pagesFinancial Accounting GlossaryDheeraj SunthaPas encore d'évaluation

- Glossary of Accounting TermsDocument16 pagesGlossary of Accounting TermsSamarpan RoyPas encore d'évaluation

- Finance GlossaryDocument16 pagesFinance Glossarybla csdcdPas encore d'évaluation

- Account Form: Glossary For CMA Part 2Document42 pagesAccount Form: Glossary For CMA Part 2ajithsubramanianPas encore d'évaluation

- Glossary of Business Terms CssDocument39 pagesGlossary of Business Terms CssDanyal TariqPas encore d'évaluation

- F&A Terms 1Document17 pagesF&A Terms 1Rohan SomaniPas encore d'évaluation

- Accounting EquationDocument5 pagesAccounting EquationMatthew BentleyPas encore d'évaluation

- Financial Statement AnalysisDocument48 pagesFinancial Statement Analysisroygaurav142Pas encore d'évaluation

- Common Terms Used in FinanceDocument22 pagesCommon Terms Used in FinanceAli Riaz KhanPas encore d'évaluation

- Lecture 2 and 3 Revision Notes Balance Sheet What Is It?Document4 pagesLecture 2 and 3 Revision Notes Balance Sheet What Is It?Anisah HabibPas encore d'évaluation

- Terminology Asset: Share CapitalDocument8 pagesTerminology Asset: Share CapitalHenna HussainPas encore d'évaluation

- Elements of Financial Statements & The Recognition Criteria For Assets & LiabilitiesDocument13 pagesElements of Financial Statements & The Recognition Criteria For Assets & LiabilitiesdeepshrmPas encore d'évaluation

- Discounted Cash Flow ModelDocument21 pagesDiscounted Cash Flow Modelvaibhavsachdeva0326Pas encore d'évaluation

- What Are The Disadvantages of The Perpetual and Period Inventory System?Document4 pagesWhat Are The Disadvantages of The Perpetual and Period Inventory System?Siwei TangPas encore d'évaluation

- Updated Lecture Partnership and CorporationDocument10 pagesUpdated Lecture Partnership and CorporationApplePas encore d'évaluation

- Business Financial Terms and Ratios DefinitionsDocument18 pagesBusiness Financial Terms and Ratios DefinitionssubburamsharmaPas encore d'évaluation

- Chart of AccountsDocument7 pagesChart of Accountsdilip_ajjuPas encore d'évaluation

- Engineering Economy TerminologyDocument7 pagesEngineering Economy Terminologygrachellesvampirebite100% (1)

- Financial Terms and Ratios DefinitionsDocument25 pagesFinancial Terms and Ratios DefinitionsKtn Patil100% (1)

- FAQs For F&a InterviewsDocument13 pagesFAQs For F&a InterviewsVamsi Chowdary KolliPas encore d'évaluation

- The Original Attachment: BasicsDocument32 pagesThe Original Attachment: BasicsvijayPas encore d'évaluation

- Finance QuestionsDocument10 pagesFinance QuestionsAkash ChauhanPas encore d'évaluation

- Project DocumentationDocument82 pagesProject DocumentationMani Bhargavi KommareddyPas encore d'évaluation

- Advanced Financial Management PDFDocument203 pagesAdvanced Financial Management PDFSanthosh Kumar100% (1)

- Andarikiayurvedam-June 2007 PDFDocument36 pagesAndarikiayurvedam-June 2007 PDFMani Bhargavi KommareddyPas encore d'évaluation

- Aruna by ChalamDocument49 pagesAruna by ChalamMani Bhargavi Kommareddy100% (1)

- The Following Candidates Selected by Union Bank of India at Respective CentreDocument7 pagesThe Following Candidates Selected by Union Bank of India at Respective CentreMani Bhargavi KommareddyPas encore d'évaluation

- FI-By Upendar Reddy, ICWAIDocument270 pagesFI-By Upendar Reddy, ICWAIUpendar ReddyPas encore d'évaluation

- Managingaccountspayablesprocess 140620172001 Phpapp01Document29 pagesManagingaccountspayablesprocess 140620172001 Phpapp01Mani Bhargavi KommareddyPas encore d'évaluation

- 1AppFormMP15 16Document3 pages1AppFormMP15 16Mani Bhargavi KommareddyPas encore d'évaluation

- IGNOU Admission Ad EngDocument1 pageIGNOU Admission Ad EngtheprinceninuPas encore d'évaluation

- CO Account Assignment LogicDocument4 pagesCO Account Assignment LogicvenkatPas encore d'évaluation

- VedicReport8 11 20154 47 27PM PDFDocument47 pagesVedicReport8 11 20154 47 27PM PDFMani Bhargavi KommareddyPas encore d'évaluation

- Jr. Material English (Sanskrit) FinalDocument12 pagesJr. Material English (Sanskrit) FinalMani Bhargavi KommareddyPas encore d'évaluation

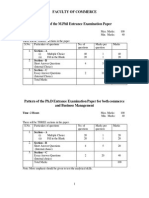

- Faculty of CommerceDocument5 pagesFaculty of CommerceMani Bhargavi KommareddyPas encore d'évaluation

- New General LedgerDocument17 pagesNew General LedgermlopegaPas encore d'évaluation

- Design of Web Based NewspaperDocument42 pagesDesign of Web Based NewspaperBabita BhagatPas encore d'évaluation

- Direct Indirect TaxDocument6 pagesDirect Indirect TaxcrappitycarapPas encore d'évaluation

- Nageswararao 136814341Document2 pagesNageswararao 136814341Mani Bhargavi KommareddyPas encore d'évaluation

- NCEC LALL ART FromSiberiaWithLoveDocument3 pagesNCEC LALL ART FromSiberiaWithLoveMani Bhargavi KommareddyPas encore d'évaluation

- SAP FI CertificationDocument100 pagesSAP FI CertificationMani Bhargavi Kommareddy100% (1)

- Chatlog Fico Online Training 2015-06-17 19 - 21Document1 pageChatlog Fico Online Training 2015-06-17 19 - 21Mani Bhargavi KommareddyPas encore d'évaluation

- Jr. Material Telugu (Sanskrit) FinalDocument12 pagesJr. Material Telugu (Sanskrit) FinalMani Bhargavi KommareddyPas encore d'évaluation

- Notification SBI Special Management Executive BankingDocument2 pagesNotification SBI Special Management Executive BankingkdvprasadPas encore d'évaluation

- Viruses NewDocument7 pagesViruses NewMani Bhargavi KommareddyPas encore d'évaluation

- Sap Fico SatyanarayanaDocument0 pageSap Fico Satyanarayanasubbavelama100% (3)

- Design of Web Based NewspaperDocument42 pagesDesign of Web Based NewspaperBabita BhagatPas encore d'évaluation

- AP ProcessorUserGuideV1.2Document65 pagesAP ProcessorUserGuideV1.2rajesh1978.nair2381100% (1)

- SAP FI Bank ConfigurationDocument68 pagesSAP FI Bank Configurationhassan sabry92% (25)

- Divisional PRO, NuziveeduDocument6 pagesDivisional PRO, NuziveeduMani Bhargavi KommareddyPas encore d'évaluation

- Gaurav Jain: SAP FICO, GM & FM ConsultantDocument5 pagesGaurav Jain: SAP FICO, GM & FM ConsultantMani Bhargavi KommareddyPas encore d'évaluation

- Cost Accounting Mastery - 2Document2 pagesCost Accounting Mastery - 2Mark Revarez0% (1)

- (Agamata Relevant Costing) Chap 9 - Short-Term Decision PDFDocument66 pages(Agamata Relevant Costing) Chap 9 - Short-Term Decision PDFMatthew Tiu80% (20)

- ABC Costing Literature ReviewDocument5 pagesABC Costing Literature Reviewafmzkbuvlmmhqq100% (1)

- Muh - Syukur - A031191077 (Problem 1-23 Dan Problem 1-24) Akuntansi ManajemenDocument5 pagesMuh - Syukur - A031191077 (Problem 1-23 Dan Problem 1-24) Akuntansi ManajemenRismayantiPas encore d'évaluation

- Engineering Management NoteDocument77 pagesEngineering Management NoteDamisi PikudaPas encore d'évaluation

- CH PDFDocument68 pagesCH PDFFabrienne Kate Eugenio LiberatoPas encore d'évaluation

- Hca 353 Proposal UpdatedDocument18 pagesHca 353 Proposal Updatedapi-490705060Pas encore d'évaluation

- Assigment 5.34Document7 pagesAssigment 5.34Indahna SulfaPas encore d'évaluation

- Organisational Study Report OnDocument70 pagesOrganisational Study Report OnÂbîjîţh KBPas encore d'évaluation

- Job Order Costing ADocument31 pagesJob Order Costing AAnji GoyPas encore d'évaluation

- (C) Present Value of Future Benefits: Multiple Choice Questions (MCQS)Document8 pages(C) Present Value of Future Benefits: Multiple Choice Questions (MCQS)Z the officerPas encore d'évaluation

- Costruction Cost EstimateDocument53 pagesCostruction Cost EstimatePipolo PippoPas encore d'évaluation

- Chapter 02 Job Order CostingDocument52 pagesChapter 02 Job Order Costingbaloojan100% (1)

- Managerial Accounting - MHRM 515Document151 pagesManagerial Accounting - MHRM 515Titima Nyum100% (1)

- Darwin Capuno PT 2 Las 4Document3 pagesDarwin Capuno PT 2 Las 4Darwin CapunoPas encore d'évaluation

- Factory OverheadDocument21 pagesFactory OverheadRey Joyce AbuelPas encore d'évaluation

- Standard Costs and Variance Analysis ERDocument19 pagesStandard Costs and Variance Analysis ERElyana SulayPas encore d'évaluation

- Cake Pricing WorksheetDocument2 pagesCake Pricing WorksheetJerico LapurgaPas encore d'évaluation

- Profit Center Accounting (EC-PCA) Profitability Analysis (COPA)Document18 pagesProfit Center Accounting (EC-PCA) Profitability Analysis (COPA)asmitaPas encore d'évaluation

- Managerial Accounting Tools For Business Decision Making 8th Edition Weygandt Test BankDocument36 pagesManagerial Accounting Tools For Business Decision Making 8th Edition Weygandt Test Bankrenewerelamping1psm100% (22)

- Non-BOQ Rates (Revised)Document3 pagesNon-BOQ Rates (Revised)ahcivil2021Pas encore d'évaluation

- Labour Control: Ashim Bhatta (CA, MBS, ISA)Document41 pagesLabour Control: Ashim Bhatta (CA, MBS, ISA)roshinaPas encore d'évaluation

- Resa Afar 1Document26 pagesResa Afar 1Princess JoannaPas encore d'évaluation

- Chapter 10: Acquisition and Disposition of Property, Plant, and EquipmentDocument26 pagesChapter 10: Acquisition and Disposition of Property, Plant, and EquipmentOumer ShaffiPas encore d'évaluation

- P2 - Performance ManagementDocument20 pagesP2 - Performance ManagementNoor Liza AliPas encore d'évaluation

- CH 3 Job OrderDocument5 pagesCH 3 Job Orderagm25Pas encore d'évaluation

- MAS-42E (Budgeting With Probability Analysis)Document10 pagesMAS-42E (Budgeting With Probability Analysis)Fella GultianoPas encore d'évaluation

- Ica Question BankDocument22 pagesIca Question Bankicchapurtiutsavmandal1Pas encore d'évaluation

- Chapter 02 TestbankDocument372 pagesChapter 02 TestbankAvisha SinghPas encore d'évaluation

- BudgetingDocument4 pagesBudgetingYaj Cruzada100% (1)