Vous aimerez peut-être aussi

- Multiplication: Factors 0 to 5, Grades 2 - 3: Developmental DrillD'EverandMultiplication: Factors 0 to 5, Grades 2 - 3: Developmental DrillPas encore d'évaluation

- August & September Monthly Collection, Grade 1D'EverandAugust & September Monthly Collection, Grade 1Pas encore d'évaluation

- USA Eco Indicators Dashboard - Consumer Spending, Confidence & SentimentDocument1 pageUSA Eco Indicators Dashboard - Consumer Spending, Confidence & SentimentWallstreetablePas encore d'évaluation

- OFHEO 3% Trend Dec 2010Document1 pageOFHEO 3% Trend Dec 2010kettle1Pas encore d'évaluation

- Tier Index V Delta Dec 2010Document2 pagesTier Index V Delta Dec 2010kettle1Pas encore d'évaluation

- Matt Crooke Reforming IMSDocument12 pagesMatt Crooke Reforming IMSM.Hatta Dosen StiepanPas encore d'évaluation

- Investment Analysis 79: Figure 2.4-9 Relative Performance of Australian Dollar Versus CRB IndexDocument1 pageInvestment Analysis 79: Figure 2.4-9 Relative Performance of Australian Dollar Versus CRB IndexYeimsPas encore d'évaluation

- U3 ModelDocument2 pagesU3 Modelkettle1Pas encore d'évaluation

- Atlanta TieredDocument1 pageAtlanta Tieredkettle1Pas encore d'évaluation

- Rents and Yields Q1-2009Document5 pagesRents and Yields Q1-2009avisitoronscribdPas encore d'évaluation

- Managing The Financial Crisis: Argentina (2002)Document63 pagesManaging The Financial Crisis: Argentina (2002)ankushishwarPas encore d'évaluation

- Weekly Episode UpdateDocument30 pagesWeekly Episode UpdateumarPas encore d'évaluation

- Sovereign Gold Bonds: A Smart Choice For Gold InvestmentsDocument15 pagesSovereign Gold Bonds: A Smart Choice For Gold InvestmentsRaju SharmaPas encore d'évaluation

- Aerodrome Chart MANAUS / Ponta Pelada, MIL (SBMN) : ARP S03 08 45 W059 59 06 Am-BrasilDocument2 pagesAerodrome Chart MANAUS / Ponta Pelada, MIL (SBMN) : ARP S03 08 45 W059 59 06 Am-BrasilJoão MazzaropiPas encore d'évaluation

- HSE Dashboard For Multiple SitessDocument11 pagesHSE Dashboard For Multiple SitessAfroz Alam0% (1)

- ML12179A248Document1 039 pagesML12179A248וויסאם חטארPas encore d'évaluation

- Jan 23Document1 pageJan 23Official AulianrPas encore d'évaluation

- 0000-Aa-Dg-000103-R01-Comedor C3-Distribución ElectricaDocument1 page0000-Aa-Dg-000103-R01-Comedor C3-Distribución ElectricaFrank Cortorreal GriffinPas encore d'évaluation

- Weekly Epi Update 33Document28 pagesWeekly Epi Update 33elfiahPas encore d'évaluation

- (Four County Totals) Price Per SQ Foot vs. Residential Resale InventoryDocument5 pages(Four County Totals) Price Per SQ Foot vs. Residential Resale InventoryJim HamiltonPas encore d'évaluation

- Weekly Epi Update 109Document10 pagesWeekly Epi Update 109RENZO ARCHIE ALBERTI CHOMONPas encore d'évaluation

- JamiesonDocument6 pagesJamiesonAlly Bin AssadPas encore d'évaluation

- Weekly Epi Update 36Document30 pagesWeekly Epi Update 36Ulfa Nur RohmahPas encore d'évaluation

- NEDADraft CL RRP Updated PDFDocument27 pagesNEDADraft CL RRP Updated PDFLanie MarcellaPas encore d'évaluation

- 74 Sme Mining Engineering HandbookDocument1 page74 Sme Mining Engineering HandbookYeimsPas encore d'évaluation

- Technical Marketing Information (Tmi) : Shane GillesDocument21 pagesTechnical Marketing Information (Tmi) : Shane GillesemilioPas encore d'évaluation

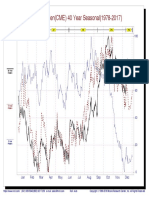

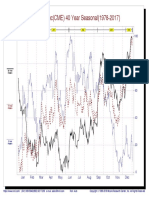

- Japanese Yen (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDocument1 pageJapanese Yen (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecjozefPas encore d'évaluation

- BT 1504Document2 pagesBT 1504Nguyễn Minh ĐứcPas encore d'évaluation

- Ch03 Functions 3rd EdDocument60 pagesCh03 Functions 3rd EdShahril MohamadPas encore d'évaluation

- Weekly Epi Update 35Document31 pagesWeekly Epi Update 35Maisury LadjidjiPas encore d'évaluation

- Weekly Epi Update 35Document31 pagesWeekly Epi Update 35QariahMaulidiahAminPas encore d'évaluation

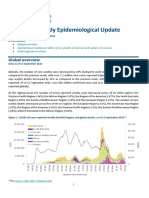

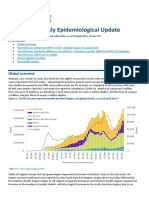

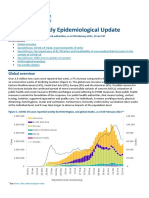

- COVID-19 Weekly Epidemiological Update: Global OverviewDocument31 pagesCOVID-19 Weekly Epidemiological Update: Global OverviewPaolaPas encore d'évaluation

- 0000-Aa-Dg-000107-R01-Comedor C2-Distribución ElectricaDocument1 page0000-Aa-Dg-000107-R01-Comedor C2-Distribución ElectricaFrank Cortorreal GriffinPas encore d'évaluation

- 01 SnyderDocument93 pages01 SnyderSopheak ThapPas encore d'évaluation

- 2013 Topo MapDocument1 page2013 Topo MapAtharva IPas encore d'évaluation

- COVID-19 Weekly Epidemiological Update: Global OverviewDocument31 pagesCOVID-19 Weekly Epidemiological Update: Global OverviewPegi PrayogaPas encore d'évaluation

- ROAD-3: 450mm THKDocument1 pageROAD-3: 450mm THKAhmed MandorPas encore d'évaluation

- FIFA 23 Draft Simulator FUTBINDocument1 pageFIFA 23 Draft Simulator FUTBINrarescp04Pas encore d'évaluation

- Built in Functions 3rd EdDocument60 pagesBuilt in Functions 3rd EdShahril MohamadPas encore d'évaluation

- Oracle Database 11g OverviewDocument46 pagesOracle Database 11g OverviewEddie Awad91% (11)

- US Dollar Index (ICE) 34 Year Seasonal (1985-2018) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDocument1 pageUS Dollar Index (ICE) 34 Year Seasonal (1985-2018) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecJuan JosePas encore d'évaluation

- Development of Bond Markets and The Market Micro StructureDocument16 pagesDevelopment of Bond Markets and The Market Micro StructureAmik TandelPas encore d'évaluation

- British Pound (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDocument1 pageBritish Pound (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecMuhamed RamadaniPas encore d'évaluation

- British Pound (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDocument1 pageBritish Pound (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecEyad QarqashPas encore d'évaluation

- 46 Active 9 Contract 33 DOM 96.6% List/Sale: Active Inventory 2009 Vs 2010 Active/Sold 2010Document6 pages46 Active 9 Contract 33 DOM 96.6% List/Sale: Active Inventory 2009 Vs 2010 Active/Sold 2010Josette SkillingPas encore d'évaluation

- Crude Oil (NYM) 35 Year Seasonal (1983-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDocument1 pageCrude Oil (NYM) 35 Year Seasonal (1983-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecjozefPas encore d'évaluation

- Sectiunu Funda A3 F7 R4D - 20Document1 pageSectiunu Funda A3 F7 R4D - 20Dani Serban0% (1)

- UM C Motorized Changeover Switches 125A - 3150ADocument3 pagesUM C Motorized Changeover Switches 125A - 3150AStif Stif100% (1)

- Modern Bear Market Mekko Chart 1947 To PresentDocument1 pageModern Bear Market Mekko Chart 1947 To PresentPraveen ChawlaPas encore d'évaluation

- Hondacivic ArDocument2 pagesHondacivic Arapi-3709675Pas encore d'évaluation

- IC Marketing Campaign Dashboard 11183Document3 pagesIC Marketing Campaign Dashboard 11183Tú Tâm NguyễnPas encore d'évaluation

- SATE Model PDFDocument1 pageSATE Model PDFKökö Trï WidödöPas encore d'évaluation

- Swiss Franc (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDocument1 pageSwiss Franc (CME) 40 Year Seasonal (1978-2017) : Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecEyad QarqashPas encore d'évaluation

- Usth Shop DWG Deraft by Mod Rev2 B2-2Document1 pageUsth Shop DWG Deraft by Mod Rev2 B2-2Emad AliPas encore d'évaluation

- US Auto Loan DataDocument1 pageUS Auto Loan Datakettle1Pas encore d'évaluation

- OEE - Fine-Blanking (May-2011)Document41 pagesOEE - Fine-Blanking (May-2011)bluerosebachPas encore d'évaluation

- ST of NZD ST Old11125Document1 pageST of NZD ST Old11125rishabhupsc2024Pas encore d'évaluation

- FREE Printable Ramadan ChecklistDocument1 pageFREE Printable Ramadan ChecklistAbubakr MaljeePas encore d'évaluation

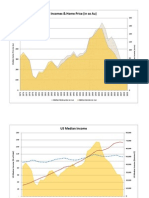

- Incomes & Home Price (In Oz Au)Document2 pagesIncomes & Home Price (In Oz Au)kettle1Pas encore d'évaluation

- Book1 Recovered)Document1 pageBook1 Recovered)kettle1Pas encore d'évaluation

- Atlanta TieredDocument1 pageAtlanta Tieredkettle1Pas encore d'évaluation

- Ofheo NJ RatioDocument1 pageOfheo NJ Ratiokettle1Pas encore d'évaluation

- NJRER Bubble Analysis Rev 4Document2 pagesNJRER Bubble Analysis Rev 4kettle1Pas encore d'évaluation

- June 2010 Cae-Shiller TrendsDocument24 pagesJune 2010 Cae-Shiller Trendskettle1Pas encore d'évaluation

- 1q10hpi StsDocument3 pages1q10hpi Stskettle1Pas encore d'évaluation

- Case Shiller Seasonality 2 Dec 2010Document8 pagesCase Shiller Seasonality 2 Dec 2010kettle1Pas encore d'évaluation

- Tier IndexDocument1 pageTier Indexkettle1Pas encore d'évaluation

- Historical RatesDocument1 pageHistorical Rateskettle1Pas encore d'évaluation

- U3 ModelDocument2 pagesU3 Modelkettle1Pas encore d'évaluation

- NJ HPI Projection 1Document1 pageNJ HPI Projection 1kettle1Pas encore d'évaluation

- Oct 2009 Unemployment UpdateDocument7 pagesOct 2009 Unemployment Updatekettle1Pas encore d'évaluation

- Fiddy TrendsDocument9 pagesFiddy Trendskettle1Pas encore d'évaluation

- Net Monthly TIC Flows: Kettle1 Research Kettle1 ResearchDocument7 pagesNet Monthly TIC Flows: Kettle1 Research Kettle1 Researchkettle1Pas encore d'évaluation

- Interest Rate ChartsDocument3 pagesInterest Rate Chartskettle1Pas encore d'évaluation

- Assumption and Data Sources:: Kettle1 ResearchDocument5 pagesAssumption and Data Sources:: Kettle1 Researchkettle1Pas encore d'évaluation

- NJ Home Sales DataDocument3 pagesNJ Home Sales Datakettle1Pas encore d'évaluation

- Unemployment DataDocument2 pagesUnemployment Datakettle1Pas encore d'évaluation

- NJ - Ca - FL Income PriceDocument1 pageNJ - Ca - FL Income Pricekettle1Pas encore d'évaluation

- NJ HPI RatioDocument1 pageNJ HPI Ratiokettle1Pas encore d'évaluation

- Earner ProfileDocument1 pageEarner Profilekettle1Pas encore d'évaluation

- Treasury Tax RecieptsDocument3 pagesTreasury Tax Recieptskettle1Pas encore d'évaluation

- Recession DepthDocument1 pageRecession Depthkettle1Pas encore d'évaluation

- Refined Projections For UnemploymentDocument4 pagesRefined Projections For Unemploymentkettle1Pas encore d'évaluation

- Unemployment Projections 2009Document1 pageUnemployment Projections 2009kettle1Pas encore d'évaluation

- Drapeau Resume May09Document5 pagesDrapeau Resume May09drmark212Pas encore d'évaluation

- Pagan and Wiccan Quotes and GuidanceDocument8 pagesPagan and Wiccan Quotes and GuidanceStinkyBooPas encore d'évaluation

- Approaches To Violence in IndiaDocument17 pagesApproaches To Violence in IndiaDeepa BhatiaPas encore d'évaluation

- Lodge LeadershipDocument216 pagesLodge LeadershipIoannis KanlisPas encore d'évaluation

- Communication and Globalization Lesson 2Document13 pagesCommunication and Globalization Lesson 2Zetrick Orate0% (1)

- Working Capital Management-FinalDocument70 pagesWorking Capital Management-FinalharmitkPas encore d'évaluation

- Directions: Choose The Best Answer For Each Multiple Choice Question. Write The Best Answer On The BlankDocument2 pagesDirections: Choose The Best Answer For Each Multiple Choice Question. Write The Best Answer On The BlankRanulfo MayolPas encore d'évaluation

- 5HP500-590 4139 - 751 - 627dDocument273 pages5HP500-590 4139 - 751 - 627ddejanflojd100% (24)

- Ivler vs. Republic, G.R. No. 172716Document23 pagesIvler vs. Republic, G.R. No. 172716Joey SalomonPas encore d'évaluation

- Education Law OutlineDocument53 pagesEducation Law Outlinemischa29100% (1)

- ImpetigoDocument16 pagesImpetigokikimasyhurPas encore d'évaluation

- A Lei Do Sucesso Napoleon Hill Download 2024 Full ChapterDocument23 pagesA Lei Do Sucesso Napoleon Hill Download 2024 Full Chapterdavid.brown752100% (12)

- From Jest To Earnest by Roe, Edward Payson, 1838-1888Document277 pagesFrom Jest To Earnest by Roe, Edward Payson, 1838-1888Gutenberg.org100% (1)

- MPCDocument193 pagesMPCpbaculimaPas encore d'évaluation

- Em 1.4 RMDocument18 pagesEm 1.4 RMMangam RajkumarPas encore d'évaluation

- SuperconductorDocument33 pagesSuperconductorCrisanta GanadoPas encore d'évaluation

- Payment Billing System DocumentDocument65 pagesPayment Billing System Documentshankar_718571% (7)

- Google Automatically Generates HTML Versions of Documents As We Crawl The WebDocument2 pagesGoogle Automatically Generates HTML Versions of Documents As We Crawl The Websuchi ravaliaPas encore d'évaluation

- Jurnal Politik Dan Cinta Tanah Air Dalam Perspektif IslamDocument9 pagesJurnal Politik Dan Cinta Tanah Air Dalam Perspektif Islamalpiantoutina12Pas encore d'évaluation

- EdExcel A Level Chemistry Unit 5 Mark Scheme Jan 2000Document3 pagesEdExcel A Level Chemistry Unit 5 Mark Scheme Jan 2000Nabeeha07Pas encore d'évaluation

- Talent Development - FranceDocument6 pagesTalent Development - FranceAkram HamiciPas encore d'évaluation

- Personal Philosophy of Education-Exemplar 1Document2 pagesPersonal Philosophy of Education-Exemplar 1api-247024656Pas encore d'évaluation

- WaiverDocument1 pageWaiverWilliam GrundyPas encore d'évaluation

- De La Salle Araneta University Grading SystemDocument2 pagesDe La Salle Araneta University Grading Systemnicolaus copernicus100% (2)

- Sucesos de Las Islas Filipinas PPT Content - Carlos 1Document2 pagesSucesos de Las Islas Filipinas PPT Content - Carlos 1A Mi YaPas encore d'évaluation

- Bgs Chapter 2Document33 pagesBgs Chapter 2KiranShettyPas encore d'évaluation

- 2,3,5 Aqidah Dan QHDocument5 pages2,3,5 Aqidah Dan QHBang PaingPas encore d'évaluation

- Lets Install Cisco ISEDocument8 pagesLets Install Cisco ISESimon GarciaPas encore d'évaluation

- Layos vs. VillanuevaDocument2 pagesLayos vs. VillanuevaLaura MangantulaoPas encore d'évaluation

- Shrek FSCDocument5 pagesShrek FSCMafer CastroPas encore d'évaluation