Vous aimerez peut-être aussi

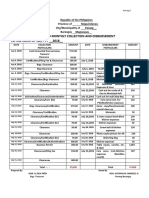

- Itemized Monthly Collection & DisbursementDocument25 pagesItemized Monthly Collection & DisbursementCyrus John VelardePas encore d'évaluation

- 40221390-Dehydrated-Onion - MarketDocument13 pages40221390-Dehydrated-Onion - MarketGourav TailorPas encore d'évaluation

- Chapter 2 Corporate TaxDocument50 pagesChapter 2 Corporate TaxNgPas encore d'évaluation

- Basis of Malaysia Income TaxDocument17 pagesBasis of Malaysia Income TaxhelenxiaochingPas encore d'évaluation

- Production Sharing AgreementsDocument106 pagesProduction Sharing AgreementsAl Hafiz Ibn HamzahPas encore d'évaluation

- Taxes and Duties at A Glance 2023-2024Document33 pagesTaxes and Duties at A Glance 2023-2024Jacob SangaPas encore d'évaluation

- Basis of Malaysian Income TaxDocument19 pagesBasis of Malaysian Income TaxMalabaris Malaya Umar SiddiqPas encore d'évaluation

- AP Cars SDN BHD - QuestionsDocument1 pageAP Cars SDN BHD - Questionsnadia0% (1)

- Business Plan - Pigger ProjectDocument19 pagesBusiness Plan - Pigger ProjectChiremba100% (1)

- CRG660-04-Lecture notes-COmpany Secretary-Sept 2018 - LatestDocument23 pagesCRG660-04-Lecture notes-COmpany Secretary-Sept 2018 - Latestauni fildzahPas encore d'évaluation

- Taxation Suggested Solution: LessDocument9 pagesTaxation Suggested Solution: LesskannadhassPas encore d'évaluation

- Al-Halal Wal Haram Fil IslamDocument380 pagesAl-Halal Wal Haram Fil IslamIzzuddin Yussof0% (1)

- Malaysian TaxationDocument19 pagesMalaysian Taxationsyahirah7767% (3)

- The Acceptance Level On GST Implementation in Malaysia: Gading Journal For The Social Sciences Vol 1 No 2 (2016)Document6 pagesThe Acceptance Level On GST Implementation in Malaysia: Gading Journal For The Social Sciences Vol 1 No 2 (2016)Harshini RamasPas encore d'évaluation

- Strategic Management PresentationDocument35 pagesStrategic Management Presentationrishuchaudhary100% (1)

- Polytechnic University of The Philippines-SurveyDocument1 pagePolytechnic University of The Philippines-SurveyCristina DanezPas encore d'évaluation

- Hydroponics SWOT AnalysisDocument21 pagesHydroponics SWOT AnalysisDPas encore d'évaluation

- Case Study 4 Papa JohnDocument9 pagesCase Study 4 Papa JohnLekha GuptaPas encore d'évaluation

- 10 Principle of FinanceDocument7 pages10 Principle of FinanceJessicaPas encore d'évaluation

- PepsiDocument107 pagesPepsiJuan Pablo Albarracin67% (3)

- Mis Applications in The F&B ServiceDocument14 pagesMis Applications in The F&B ServiceGil Teodosip100% (7)

- Tax ComputationDocument13 pagesTax ComputationEcha Sya0% (1)

- Chap-3 Company SecretaryDocument21 pagesChap-3 Company SecretaryElya Mulis100% (1)

- Research Paper On VATDocument60 pagesResearch Paper On VATjtesh2020100% (1)

- PPTDocument33 pagesPPTanis solihah0% (1)

- 03FM SM Ch3 1LPDocument6 pages03FM SM Ch3 1LPjoebloggs18880% (1)

- History of Ethiopian TaxationDocument4 pagesHistory of Ethiopian Taxationsara woldeyohannes100% (1)

- Taxation in BangladeshDocument6 pagesTaxation in BangladeshSakibPas encore d'évaluation

- Eco 415Document4 pagesEco 415Verne Skeete Jr.100% (1)

- Lecture Tutorial - P, CL and CA (A)Document3 pagesLecture Tutorial - P, CL and CA (A)yym cindyy100% (1)

- Alia Syazwani Practical Training ReportDocument22 pagesAlia Syazwani Practical Training ReportAli Hisham GholamPas encore d'évaluation

- BOP AssignmentDocument20 pagesBOP AssignmentSajid Karbari0% (1)

- A Study On Self-Assessment Tax System Awareness in MalaysiaDocument8 pagesA Study On Self-Assessment Tax System Awareness in Malaysiaaiman100% (1)

- 3.0 Principles of Effective AccountabilityDocument10 pages3.0 Principles of Effective AccountabilityNor Ashqira KamarulPas encore d'évaluation

- Pad 240 PDFDocument10 pagesPad 240 PDFFais Aiman MustaphaPas encore d'évaluation

- MGT162 Individual AssignmentDocument17 pagesMGT162 Individual AssignmentMEOR HAMIZAN MEOR MOHAMMAD FAREDPas encore d'évaluation

- Drafting Financial Statements (International Stream) : Monday 1 December 2008Document9 pagesDrafting Financial Statements (International Stream) : Monday 1 December 2008salaam7860Pas encore d'évaluation

- Ways of Curbing InflationDocument3 pagesWays of Curbing InflationPooja EkkaPas encore d'évaluation

- Appeal Tax Procedure (Malaysia)Document2 pagesAppeal Tax Procedure (Malaysia)Zati TyPas encore d'évaluation

- ACC 4041 Tutorial - Corporate Tax 2Document3 pagesACC 4041 Tutorial - Corporate Tax 2Atiqah DalikPas encore d'évaluation

- Tutorial 5 Eco 415Document7 pagesTutorial 5 Eco 415ZhiXPas encore d'évaluation

- Assignment 2Document16 pagesAssignment 2Mandy OwxPas encore d'évaluation

- Tutorial 1 3Document5 pagesTutorial 1 3Faiz MohamadPas encore d'évaluation

- Constitutional Validity (Excise Duties, Custom Duties & Service Taxes)Document19 pagesConstitutional Validity (Excise Duties, Custom Duties & Service Taxes)07anshuman100% (2)

- 2014 Perodua Improving Customer SatisfaDocument16 pages2014 Perodua Improving Customer Satisfanusra_t100% (1)

- LiabilityDocument4 pagesLiabilityNor Karmila Roslan0% (1)

- 5 Social ContractDocument23 pages5 Social ContractShuq Faqat al-FansuriPas encore d'évaluation

- Eco211 210 164 219Document10 pagesEco211 210 164 219Ana MuslimahPas encore d'évaluation

- A162 Answer Tutorial 1 and Answer Siti NorlizaDocument13 pagesA162 Answer Tutorial 1 and Answer Siti NorlizaXiao Yun Yap0% (2)

- Taxation AnswerDocument13 pagesTaxation AnswerkannadhassPas encore d'évaluation

- E2MDocument2 pagesE2MEdward JohnPas encore d'évaluation

- Exam Docs Dipifr 2012Document2 pagesExam Docs Dipifr 2012aqmal16Pas encore d'évaluation

- Planning For Change in A Company Riddled With ProblemsDocument10 pagesPlanning For Change in A Company Riddled With ProblemsSasiram RajasekaranPas encore d'évaluation

- Fin430 - Dec2019Document6 pagesFin430 - Dec2019nurinsabyhahPas encore d'évaluation

- Workshop 6 (Students) ADM657Document7 pagesWorkshop 6 (Students) ADM657Khairi N WaniePas encore d'évaluation

- Far210 Topic 2 Malaysian Conceptual FrameworkDocument79 pagesFar210 Topic 2 Malaysian Conceptual FrameworkSamurai Hut100% (1)

- Topic 4 - Time Value of MoneyDocument64 pagesTopic 4 - Time Value of MoneyHisyam SeePas encore d'évaluation

- Define National Income Eco415Document3 pagesDefine National Income Eco415aishahPas encore d'évaluation

- Tutorial 2e Residence StatusDocument2 pagesTutorial 2e Residence StatusnatlyhPas encore d'évaluation

- Question AIS AssignmentDocument4 pagesQuestion AIS Assignmentfaris ikhwanPas encore d'évaluation

- Chapter 3 - Agriculture AllowancesDocument3 pagesChapter 3 - Agriculture AllowancesNURKHAIRUNNISA100% (2)

- Sme CorpDocument13 pagesSme CorpFaridz RahimPas encore d'évaluation

- Business Taxation Notes Income Tax NotesDocument303 pagesBusiness Taxation Notes Income Tax NotesIkra MalikPas encore d'évaluation

- The Industrial Training Experience Accounting EssayDocument14 pagesThe Industrial Training Experience Accounting Essayrajes2301Pas encore d'évaluation

- Export Import and EXIM PolicyDocument27 pagesExport Import and EXIM PolicyAmit JainPas encore d'évaluation

- PTX - AssignmentDocument15 pagesPTX - AssignmentNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)Pas encore d'évaluation

- A Study On The Importance of Corporate Restructuring Approches in MalaysiaDocument13 pagesA Study On The Importance of Corporate Restructuring Approches in MalaysiaValerie SintiPas encore d'évaluation

- Source: (Extracted From An Overview of GST MalaysiaDocument9 pagesSource: (Extracted From An Overview of GST MalaysiaYeehui HayleyPas encore d'évaluation

- Malawi DeloitteDocument14 pagesMalawi DeloitteMwawiPas encore d'évaluation

- An Overview of GST MalaysiaDocument23 pagesAn Overview of GST MalaysiaParimalar RajindranPas encore d'évaluation

- VAT Reform in BangladeshDocument28 pagesVAT Reform in BangladeshhossainmzPas encore d'évaluation

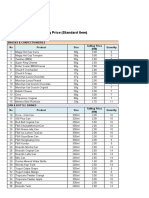

- Product Price List (Standard Item)Document1 pageProduct Price List (Standard Item)Izzuddin YussofPas encore d'évaluation

- BQDocument2 pagesBQIzzuddin YussofPas encore d'évaluation

- Week 1 Update Foundations of Monetary EconomicsDocument15 pagesWeek 1 Update Foundations of Monetary EconomicsIzzuddin YussofPas encore d'évaluation

- Joomla1.5 Installation Manual Version 0.5Document52 pagesJoomla1.5 Installation Manual Version 0.5Ivan_Obillos_5435Pas encore d'évaluation

- Kitchen ToolsDocument12 pagesKitchen ToolsZie BeaPas encore d'évaluation

- Presentation JBSDocument34 pagesPresentation JBSJBS RIPas encore d'évaluation

- Anil Kumar Singh Archana Pawar Bharti Gyanchandani Sohit Kadwey Sonam Seth Srashti SuneriyaDocument13 pagesAnil Kumar Singh Archana Pawar Bharti Gyanchandani Sohit Kadwey Sonam Seth Srashti SuneriyaSrashti SuneriyaPas encore d'évaluation

- B1 25.7Document11 pagesB1 25.7Hoàng Dương TrịnhPas encore d'évaluation

- Pizza Report PDFDocument7 pagesPizza Report PDFjuhi agarwalPas encore d'évaluation

- Oil and Gas Sector Research in Uganda - Constraints and Opportunities For SMEsDocument61 pagesOil and Gas Sector Research in Uganda - Constraints and Opportunities For SMEsGyagenda Kenneth100% (1)

- Math 3 LM Draft 4.10.2014Document367 pagesMath 3 LM Draft 4.10.2014Golden SunrisePas encore d'évaluation

- Lamp Color Temperature GuideDocument2 pagesLamp Color Temperature GuidesvmrPas encore d'évaluation

- Indiana DOR, Letter of Findings Number 04-2010069 (Nov. 4, 2011)Document2 pagesIndiana DOR, Letter of Findings Number 04-2010069 (Nov. 4, 2011)Paul MastersPas encore d'évaluation

- Chick-Fil-A EvaluationDocument4 pagesChick-Fil-A Evaluationapi-450935011Pas encore d'évaluation

- Gender Agricultural InnovationDocument31 pagesGender Agricultural InnovationAPPROCenterPas encore d'évaluation

- Kentucky Fried ChickenDocument5 pagesKentucky Fried ChickenShraddha SuvarnaPas encore d'évaluation

- Being Matt BaumgartnerDocument1 pageBeing Matt BaumgartnerErin PihlajaPas encore d'évaluation

- Red ProjectDocument30 pagesRed ProjectApoorva SrivastavaPas encore d'évaluation

- Full Text Lamb To SlaughterDocument10 pagesFull Text Lamb To SlaughterFakhrurrazi OppaPas encore d'évaluation

- FijiTimes - Dec 14 2012 WebDocument48 pagesFijiTimes - Dec 14 2012 WebfijitimescanadaPas encore d'évaluation

- Slickables Marketing ResearchDocument23 pagesSlickables Marketing ResearchJessa Kali ShortPas encore d'évaluation

- Wine Tasting EtiquetteDocument1 pageWine Tasting EtiquetteCellarsWineClubPas encore d'évaluation

- Chapter 1 - The Business of AgribusinessDocument17 pagesChapter 1 - The Business of AgribusinessBill ALPas encore d'évaluation

- Tugas Artikel Beserta Tenses Astri Armaya HasibuanDocument2 pagesTugas Artikel Beserta Tenses Astri Armaya HasibuanL-LILANZZPas encore d'évaluation

- Sheel Dele2goDocument8 pagesSheel Dele2goAnonymous vWFDPWPas encore d'évaluation