Vous aimerez peut-être aussi

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Business Plan On Food Vending in Finland PDFDocument65 pagesBusiness Plan On Food Vending in Finland PDFAnil ChauhanPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- What Is The Role of The SecretaryDocument3 pagesWhat Is The Role of The SecretaryAnil ChauhanPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

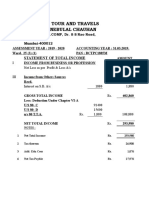

- M/S. Sunil Tour and Travels Mr. Sunil Nebulal Chauhan: Statement of Total IncomeDocument8 pagesM/S. Sunil Tour and Travels Mr. Sunil Nebulal Chauhan: Statement of Total IncomeAnil ChauhanPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- SUB: Application For Bank StatementDocument1 pageSUB: Application For Bank StatementAnil ChauhanPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Disadvantages of Joint FamilyDocument2 pagesDisadvantages of Joint FamilyAnil ChauhanPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Preparation of Balance Sheet and Profit and Loss Account: TotalDocument7 pagesPreparation of Balance Sheet and Profit and Loss Account: TotalAnil ChauhanPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Born: January 23, 1897 Died: August 18, 1945 Achievements: Passed Indian Civil Services Exam Elected CongressDocument1 pageBorn: January 23, 1897 Died: August 18, 1945 Achievements: Passed Indian Civil Services Exam Elected CongressAnil ChauhanPas encore d'évaluation

- Recycling Objectives For A Resource-Efficient Europe - Municipal Solutions For Eco-Efficient Recyclables ManagementDocument1 pageRecycling Objectives For A Resource-Efficient Europe - Municipal Solutions For Eco-Efficient Recyclables ManagementAnil ChauhanPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Surf Excerl SurndraDocument26 pagesSurf Excerl SurndraAnil ChauhanPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Evaluation Certificate: Consolidated Financial StatementDocument2 pagesEvaluation Certificate: Consolidated Financial StatementAnil ChauhanPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Foreign Exchange MarketsDocument9 pagesForeign Exchange MarketsAnil ChauhanPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Form 2-Mohan Chandrajeet Vishwakarma: Appointment ID /token No:166 Date:25/09/2014 Time:12:15 PMDocument6 pagesForm 2-Mohan Chandrajeet Vishwakarma: Appointment ID /token No:166 Date:25/09/2014 Time:12:15 PMAnil ChauhanPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Market Survey & Product Promotion in Reliance CommunicationDocument88 pagesMarket Survey & Product Promotion in Reliance CommunicationravifactPas encore d'évaluation

- Nirma ProjectDocument26 pagesNirma ProjectAnil ChauhanPas encore d'évaluation

- Test BankDocument15 pagesTest BankBWB DONALDPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Unit 15 Final ExamDocument5 pagesUnit 15 Final ExamTakuriPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Phuket Beach Hotel FinalDocument38 pagesPhuket Beach Hotel Finalsonali mishraPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Business Case For Next Generation AWS Managed Services Providers Oc...Document33 pagesThe Business Case For Next Generation AWS Managed Services Providers Oc...Saniya100% (1)

- Economical Assessment of The Impact of RFID Technology and EPC System On The Fast-Moving Consumer Goods Supply ChainDocument22 pagesEconomical Assessment of The Impact of RFID Technology and EPC System On The Fast-Moving Consumer Goods Supply ChainAlina StanciuPas encore d'évaluation

- Project Management For Renovating A Hostel: Professor Ivars LindeDocument22 pagesProject Management For Renovating A Hostel: Professor Ivars LindeVipul AlawaPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Business Case FREP HandheldDocument32 pagesBusiness Case FREP Handheldapaajaaaaa100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Practice Questions - Capital BudgetingDocument11 pagesPractice Questions - Capital Budgetingiframahmood026Pas encore d'évaluation

- P1 Investment Appraisal MethodsDocument3 pagesP1 Investment Appraisal MethodsSadeep Madhushan0% (1)

- OM Assignment - Decision Tree Using NPVDocument5 pagesOM Assignment - Decision Tree Using NPVNick SolankiPas encore d'évaluation

- Shouldice Hospital LTD: Group Case presentation-NMP25Document9 pagesShouldice Hospital LTD: Group Case presentation-NMP25Krishna TiwariPas encore d'évaluation

- Chapter 14aDocument25 pagesChapter 14aKhadiza Tul Kobra BornaPas encore d'évaluation

- Chapter TestDocument19 pagesChapter TestFia SantosPas encore d'évaluation

- Group Task - Investment Detective - Syndicate 2.Xlsx - Sheet1Document2 pagesGroup Task - Investment Detective - Syndicate 2.Xlsx - Sheet1jibrildewantaraPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Assignment - Capital BudgetingDocument2 pagesAssignment - Capital BudgetingMuhammad Ali SamarPas encore d'évaluation

- Chapter 12 - Capital BudgetingDocument26 pagesChapter 12 - Capital BudgetingSamin HaquePas encore d'évaluation

- Fin 304 Notesfdfhwefudvg Fdre Financial Markets and InstitutionDocument89 pagesFin 304 Notesfdfhwefudvg Fdre Financial Markets and InstitutionAhmed YousufzaiPas encore d'évaluation

- DWES6 - Wind Energy EconomicsDocument94 pagesDWES6 - Wind Energy EconomicsHmaedPas encore d'évaluation

- Capital BudgetingDocument15 pagesCapital Budgetingkarthik sPas encore d'évaluation

- Capital Budgeting (Penganggaran Modal)Document25 pagesCapital Budgeting (Penganggaran Modal)Beby AnggytaPas encore d'évaluation

- CO5109 - Corporate Finance PDFDocument26 pagesCO5109 - Corporate Finance PDFSayadur RahmanPas encore d'évaluation

- Net Present Value: First Principles of FinanceDocument14 pagesNet Present Value: First Principles of FinanceandresugiPas encore d'évaluation

- Group assignment-BL PDFDocument6 pagesGroup assignment-BL PDFkarthikawarrierPas encore d'évaluation

- Hansson Private LabelDocument4 pagesHansson Private Labelsd717Pas encore d'évaluation

- 241 0106Document20 pages241 0106api-27548664Pas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Aplikasi Studi Kelayakan Usaha Berbasis NPV Dan Payback Period Dalam Menganalisis Usaha Kafe Kopi Filter Andreas KikyDocument12 pagesAplikasi Studi Kelayakan Usaha Berbasis NPV Dan Payback Period Dalam Menganalisis Usaha Kafe Kopi Filter Andreas KikyTasya AdnaPas encore d'évaluation

- Solution Manual For Making Hard Decisions With Decisiontools 3rd Edition Robert T Clemen Terence ReillyDocument7 pagesSolution Manual For Making Hard Decisions With Decisiontools 3rd Edition Robert T Clemen Terence ReillyDavid Rigdon100% (29)

- Capital Budegeting (FMP)Document48 pagesCapital Budegeting (FMP)tazeenseemaPas encore d'évaluation

- Practice Exam - Part 3: Multiple ChoiceDocument4 pagesPractice Exam - Part 3: Multiple ChoiceAzeem TalibPas encore d'évaluation

- Fin Strategy Ass 1Document3 pagesFin Strategy Ass 1mqondisi nkabindePas encore d'évaluation

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)D'EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (15)