Vous aimerez peut-être aussi

- 2 Feasibility Study On DairyDocument40 pages2 Feasibility Study On DairyAdefrisPas encore d'évaluation

- Taller Modelos Unilibre INVENTARIOS EOQ EN INGLESDocument3 pagesTaller Modelos Unilibre INVENTARIOS EOQ EN INGLESjose fernando oliveros lagosPas encore d'évaluation

- Supplementary ExercisesDocument2 pagesSupplementary ExercisesemnagrichiPas encore d'évaluation

- Y4 Week 13 Day 5 PDFDocument10 pagesY4 Week 13 Day 5 PDFDaniela GrosuPas encore d'évaluation

- ACC416 Tutorial 2B Materials - Stock Valuations QtnsDocument3 pagesACC416 Tutorial 2B Materials - Stock Valuations QtnsEdrizz RizPas encore d'évaluation

- On WeightDocument21 pagesOn WeightDEEPTI50% (2)

- Quarterly Projections IDocument8 pagesQuarterly Projections IDerickMwansaPas encore d'évaluation

- Organizational Structure and History of Tat Macaroni IndustryDocument20 pagesOrganizational Structure and History of Tat Macaroni Industrydamla6k6yl6Pas encore d'évaluation

- SN 02721Document16 pagesSN 02721Redi SirbaroPas encore d'évaluation

- Project Proposal 2Document9 pagesProject Proposal 2katinuke8Pas encore d'évaluation

- Naranpur Express - JaypalDocument15 pagesNaranpur Express - Jaypalx05028Pas encore d'évaluation

- Bread Factory-5lDocument12 pagesBread Factory-5lGolden Shower தமிழ்Pas encore d'évaluation

- BTS Kakanin Corner Offers Filipino Snack InnovationDocument5 pagesBTS Kakanin Corner Offers Filipino Snack InnovationEntity RemsPas encore d'évaluation

- Scharffen Berger Case Study - Team 2Document12 pagesScharffen Berger Case Study - Team 2Andrew Bernier100% (1)

- Indigenous Milk ProductsDocument6 pagesIndigenous Milk ProductsKF SirsiPas encore d'évaluation

- Dashboard 1 - Cost of Goods Sold Product 1 - Pdt01Document13 pagesDashboard 1 - Cost of Goods Sold Product 1 - Pdt01lehilmiPas encore d'évaluation

- Verified By: Mazimpaka Jean Damascene Agronomy Officer: Production and Revenue Report The Month ofDocument3 pagesVerified By: Mazimpaka Jean Damascene Agronomy Officer: Production and Revenue Report The Month ofnteziryayoPas encore d'évaluation

- November 2020 Livestock Production and Revenue ReportDocument5 pagesNovember 2020 Livestock Production and Revenue ReportnteziryayoPas encore d'évaluation

- Measure Mass Using Kilograms and GramsDocument32 pagesMeasure Mass Using Kilograms and GramsputrlaPas encore d'évaluation

- Task 2 Unit 2 Warehouse and InventoryDocument8 pagesTask 2 Unit 2 Warehouse and InventoryVassay KhaliliPas encore d'évaluation

- FISH Feed Enterprise Business PlanDocument6 pagesFISH Feed Enterprise Business PlanELIJAH100% (1)

- Exercise 2: Market Study: Introduction To Feasibility Studies in AgricultureDocument8 pagesExercise 2: Market Study: Introduction To Feasibility Studies in AgricultureKristine Lea ClimacoPas encore d'évaluation

- Feasibility Study - PiggeryDocument12 pagesFeasibility Study - PiggeryRj Bengil100% (5)

- Tugas Persediaan 2Document6 pagesTugas Persediaan 2Bertha Liona0% (2)

- FA2 AssessmentDocument18 pagesFA2 AssessmentMinh Le Phan AnhPas encore d'évaluation

- Monitoring Harga Kepokmas Bulan NovemberDocument3 pagesMonitoring Harga Kepokmas Bulan Novemberaang hasanudinPas encore d'évaluation

- Lactococosis, Seleccion Gen y Stress, Analisis de Riesgo SanitarioDocument45 pagesLactococosis, Seleccion Gen y Stress, Analisis de Riesgo Sanitariochvrr9r9c2Pas encore d'évaluation

- Exercises On Mix Material N Labor VarianceDocument3 pagesExercises On Mix Material N Labor Variancewww.harinihariniPas encore d'évaluation

- Analisa Perhitungan Usaha Fried Chicken: QTY Satuan Harga Biaya InvestasiDocument4 pagesAnalisa Perhitungan Usaha Fried Chicken: QTY Satuan Harga Biaya InvestasiariyantoPas encore d'évaluation

- Pig Mathematics, 3rd Edition PDFDocument4 pagesPig Mathematics, 3rd Edition PDFprincekavalam2Pas encore d'évaluation

- Maximize Agricultural Production for Three KibbutzimDocument4 pagesMaximize Agricultural Production for Three KibbutzimTelat AbiPas encore d'évaluation

- Business Proposal for PopMeChips Snack ShopDocument41 pagesBusiness Proposal for PopMeChips Snack ShopChristopher GarciaPas encore d'évaluation

- Philippines Sugar Annual Report Outlines Production, Consumption, TradeDocument10 pagesPhilippines Sugar Annual Report Outlines Production, Consumption, TradeJajejijojuPas encore d'évaluation

- Royal Canin Dog Food InventoryDocument12 pagesRoyal Canin Dog Food InventoryHimera Vet PetPas encore d'évaluation

- GRAPES - Programa Comercial - WK 50Document22 pagesGRAPES - Programa Comercial - WK 50Reyk ValentinPas encore d'évaluation

- By The Sea - Buiscuit Case StudyDocument5 pagesBy The Sea - Buiscuit Case StudyAbhi SangwanPas encore d'évaluation

- Standard Costing Variance Analysis for Manufacturing CompanyDocument5 pagesStandard Costing Variance Analysis for Manufacturing CompanyBiplob K. SannyasiPas encore d'évaluation

- Group 5 Assignment FinalDocument14 pagesGroup 5 Assignment FinalBosco Odongo OpiraPas encore d'évaluation

- Master Budgeting: June July August September October Third QuarterDocument10 pagesMaster Budgeting: June July August September October Third QuarterЭниЭ.Pas encore d'évaluation

- Scharffen Berger Chocolate Maker PDFDocument5 pagesScharffen Berger Chocolate Maker PDFAjey BhangalePas encore d'évaluation

- MathematicsDocument16 pagesMathematicsSiti Zawiyah Abdul HalimPas encore d'évaluation

- Statistics Guide Aw LowDocument41 pagesStatistics Guide Aw LowivansupermanchanPas encore d'évaluation

- 02 Feed Related CostsDocument1 page02 Feed Related CostsvegalinksPas encore d'évaluation

- Budgeting QuestionsDocument8 pagesBudgeting QuestionsumarPas encore d'évaluation

- Statistik TomatDocument2 pagesStatistik TomatfrisilPas encore d'évaluation

- Sheep Fodder Diet Trial Shows No Drop in ProductivityDocument10 pagesSheep Fodder Diet Trial Shows No Drop in ProductivitycferPas encore d'évaluation

- FORMATO ESTÁNDAR PARA COMPRAS O SABANA DE COMPRASARTÍCULOSUNIDAD CANTIDADQueso cremaKg15MantequillaKg10Crema acidaL15Pechuga de polloKg20HuevoKg20SalKg5AceiteL30PimientaKg5Tequila blancoL12RefresDocument8 pagesFORMATO ESTÁNDAR PARA COMPRAS O SABANA DE COMPRASARTÍCULOSUNIDAD CANTIDADQueso cremaKg15MantequillaKg10Crema acidaL15Pechuga de polloKg20HuevoKg20SalKg5AceiteL30PimientaKg5Tequila blancoL12Refresfranco1709Pas encore d'évaluation

- Review Problem 1: Variance Analysis Using A Flexible Budget: RequiredDocument12 pagesReview Problem 1: Variance Analysis Using A Flexible Budget: RequiredGraieszian LyraPas encore d'évaluation

- Broilers - Cashflow and BudgetDocument4 pagesBroilers - Cashflow and Budgetmarumura.onwardPas encore d'évaluation

- Joint, By, Raw Mat, FOHDocument5 pagesJoint, By, Raw Mat, FOHQuinXG ChannelPas encore d'évaluation

- Budgeting 101: Projecting and Evaluating PerformanceDocument21 pagesBudgeting 101: Projecting and Evaluating PerformanceRanier Armand Valle MagnoPas encore d'évaluation

- Animal FeedDocument27 pagesAnimal FeedYem Ane100% (1)

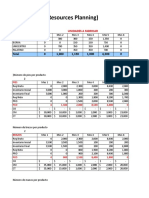

- MRP Material Resources Planning) : Resumen DRP Unidades A FabricarDocument14 pagesMRP Material Resources Planning) : Resumen DRP Unidades A FabricarPaula Vanessa CarrionPas encore d'évaluation

- Proyeksi Investasi dan Keuntungan Ayam BoilerDocument39 pagesProyeksi Investasi dan Keuntungan Ayam Boilersaleh wipgyPas encore d'évaluation

- Handa Sa Bahay RevisedDocument7 pagesHanda Sa Bahay RevisedMr. Piano DadPas encore d'évaluation

- BUDGETINGDocument3 pagesBUDGETINGcharlyneabay8Pas encore d'évaluation

- Wood Kitchen Cabinet & Counter Tops World Summary: Market Values & Financials by CountryD'EverandWood Kitchen Cabinet & Counter Tops World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Poultry World Summary: Market Values & Financials by CountryD'EverandPoultry World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Httpshhadah Github iomicroSlidesMyPresentationsCh6Ch6 PDFDocument37 pagesHttpshhadah Github iomicroSlidesMyPresentationsCh6Ch6 PDF정서윤Pas encore d'évaluation

- Introduction To Microeconomics 2022 Second Semester Test No. 2Document3 pagesIntroduction To Microeconomics 2022 Second Semester Test No. 2May JuniorroarPas encore d'évaluation

- Answer Chapter 1 QuestionsDocument1 pageAnswer Chapter 1 QuestionsMeizhao QianPas encore d'évaluation

- Parcial 2017 1 Cfa UpcDocument7 pagesParcial 2017 1 Cfa UpcCarlos AriasPas encore d'évaluation

- IB Business and ManagementDocument52 pagesIB Business and ManagementAkshat YadavPas encore d'évaluation

- Managerial Economics Ch3Document67 pagesManagerial Economics Ch3Ashe BalchaPas encore d'évaluation

- PC Chip Market Structure and Game Theory ModelsDocument1 pagePC Chip Market Structure and Game Theory ModelsHinna HussainPas encore d'évaluation

- IBDP Economic HL Chapter 3 NotesDocument8 pagesIBDP Economic HL Chapter 3 NotesAditya RathiPas encore d'évaluation

- 8 Inventory SystemDocument48 pages8 Inventory SystemPollyPas encore d'évaluation

- SS & DD Problem Set Chapter 3Document7 pagesSS & DD Problem Set Chapter 3IshmamPas encore d'évaluation

- Module 4Document45 pagesModule 4Hajarath Prasad AbburuPas encore d'évaluation

- MAS First Preboard QuestionsDocument12 pagesMAS First Preboard QuestionsVillanueva, Mariella De VeraPas encore d'évaluation

- Diminishing Marginal UtilityDocument13 pagesDiminishing Marginal Utilitysingadianarendra57Pas encore d'évaluation

- Network Design OptimizationDocument5 pagesNetwork Design OptimizationCristian DumitrachePas encore d'évaluation

- Statements of Adventa Berhad Marketing EssayDocument41 pagesStatements of Adventa Berhad Marketing EssayHND Assignment Help100% (1)

- Test Bank For Managerial Accounting Binder Ready Version 6th EditionDocument44 pagesTest Bank For Managerial Accounting Binder Ready Version 6th Editionmelissamosleybxoqardnew100% (21)

- Business Studies Chapter 10 Marketing Competition and The CustomerDocument22 pagesBusiness Studies Chapter 10 Marketing Competition and The Customer牛仔danielPas encore d'évaluation

- The Copperbelt University School of Business Department of EconomicsDocument1 pageThe Copperbelt University School of Business Department of EconomicsNthanzi MuwandiaPas encore d'évaluation

- Factors of Production and Economic Systems QuizDocument4 pagesFactors of Production and Economic Systems QuizPHILIP CAERMAREPas encore d'évaluation

- Lecture-3 Determination of Interest RatesDocument31 pagesLecture-3 Determination of Interest RatesZamir StanekzaiPas encore d'évaluation

- Measuring Exchange Rate MovementsDocument26 pagesMeasuring Exchange Rate MovementsNouman AhmadPas encore d'évaluation

- Multiple-Choice Questions: B: Rejecting Is A Term Used To Describe A Situation WhenDocument4 pagesMultiple-Choice Questions: B: Rejecting Is A Term Used To Describe A Situation WhenRavi SatyapalPas encore d'évaluation

- Public Finance - Notes Stiglitz 17-20Document5 pagesPublic Finance - Notes Stiglitz 17-20SimonVlcekPas encore d'évaluation

- In Depth Study of Housing LoanDocument77 pagesIn Depth Study of Housing LoanJugal Thakkar50% (2)

- Microeconomics Course OverviewDocument2 pagesMicroeconomics Course OverviewJp KaflePas encore d'évaluation

- FM Master Air Control NewDocument4 pagesFM Master Air Control Newajay singhPas encore d'évaluation

- Psoc Textbook by SivanagarajuDocument925 pagesPsoc Textbook by SivanagarajuBhanu BkvPas encore d'évaluation

- Practice Exam 1 - OnlineDocument9 pagesPractice Exam 1 - OnlineMaria Quinones SestoPas encore d'évaluation

- Question Bank: ७०८ सदाशिव पेठ, कुमठेकर मार्ग, पुणे ४११०३० संपकग क्रमांक (020) 2447 6938 E-mailDocument32 pagesQuestion Bank: ७०८ सदाशिव पेठ, कुमठेकर मार्ग, पुणे ४११०३० संपकग क्रमांक (020) 2447 6938 E-mailshruti gawarePas encore d'évaluation

- Marketing Exam 10 DecDocument152 pagesMarketing Exam 10 DecTauseef AhmedPas encore d'évaluation