Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- EPC ContractsDocument36 pagesEPC Contractskesharinaresh50% (2)

- Re - 1989-09Document100 pagesRe - 1989-09Anonymous kdqf49qb100% (1)

- FSCM-01 Credit ManagementDocument23 pagesFSCM-01 Credit ManagementAvinash Malladhi67% (6)

- ALGO2 Algorithm2 TutorialDocument7 pagesALGO2 Algorithm2 Tutorialhc87Pas encore d'évaluation

- Lean Vs Six SigmaDocument23 pagesLean Vs Six SigmaTrichy MaheshPas encore d'évaluation

- Account Statement: Penyata AkaunDocument2 pagesAccount Statement: Penyata AkaunArif nazmiPas encore d'évaluation

- Daniel's Draft PresentationDocument21 pagesDaniel's Draft PresentationdanookyerePas encore d'évaluation

- Newtech Advant Business Plan9 PDFDocument38 pagesNewtech Advant Business Plan9 PDFdanookyerePas encore d'évaluation

- BoA CFE-CMStatistics 2017 PDFDocument272 pagesBoA CFE-CMStatistics 2017 PDFdanookyerePas encore d'évaluation

- Basic Financial Econometrics PDFDocument167 pagesBasic Financial Econometrics PDFdanookyerePas encore d'évaluation

- Models and Theories of Customer SatisfactionDocument31 pagesModels and Theories of Customer SatisfactiondanookyerePas encore d'évaluation

- Financing Small Scale Oil Palm Producers in The Western Region of Ghana-Ahanta West DistrictDocument18 pagesFinancing Small Scale Oil Palm Producers in The Western Region of Ghana-Ahanta West DistrictdanookyerePas encore d'évaluation

- Joshua 1:9: Bible Quotations For The Bible Reading MarathonDocument5 pagesJoshua 1:9: Bible Quotations For The Bible Reading MarathondanookyerePas encore d'évaluation

- MKTG Res CUSTOMER DELIGHT IN HOSPITALITY INDUSTRYDocument51 pagesMKTG Res CUSTOMER DELIGHT IN HOSPITALITY INDUSTRYdanookyerePas encore d'évaluation

- Customer Satisfaction Theories PDFDocument34 pagesCustomer Satisfaction Theories PDFdanookyerePas encore d'évaluation

- Customer Satisfaction Theories PDFDocument34 pagesCustomer Satisfaction Theories PDFdanookyerePas encore d'évaluation

- Theories in Marketing StrategyDocument4 pagesTheories in Marketing StrategydanookyerePas encore d'évaluation

- Parenting) 10 Tips To Healthy Eating and Physical Activity For KidsDocument5 pagesParenting) 10 Tips To Healthy Eating and Physical Activity For KidssteriandediuPas encore d'évaluation

- Customer Satisfaction Theories PDFDocument34 pagesCustomer Satisfaction Theories PDFdanookyerePas encore d'évaluation

- Consumer Buying DecisionsDocument2 pagesConsumer Buying DecisionsdanookyerePas encore d'évaluation

- Consumer Buying DecisionsDocument2 pagesConsumer Buying DecisionsdanookyerePas encore d'évaluation

- The Role of Communication in Contemporary MarketingDocument4 pagesThe Role of Communication in Contemporary MarketingdanookyerePas encore d'évaluation

- The Role of Communication in Contemporary MarketingDocument4 pagesThe Role of Communication in Contemporary MarketingdanookyerePas encore d'évaluation

- Accounting For DepreciationDocument28 pagesAccounting For DepreciationdanookyerePas encore d'évaluation

- Accounting For Cash FlowDocument2 pagesAccounting For Cash FlowdanookyerePas encore d'évaluation

- The Role of Communication in Contemporary MarketingDocument4 pagesThe Role of Communication in Contemporary MarketingdanookyerePas encore d'évaluation

- Importance of A Trial BalanceDocument1 pageImportance of A Trial Balancedanookyere100% (3)

- The Role of Communication in Contemporary MarketingDocument4 pagesThe Role of Communication in Contemporary MarketingdanookyerePas encore d'évaluation

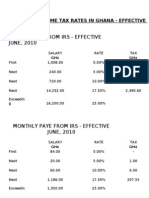

- Personal Income Tax Rates in GhanaDocument2 pagesPersonal Income Tax Rates in GhanadanookyerePas encore d'évaluation

- 2011 M ClassDocument22 pages2011 M ClassdanookyerePas encore d'évaluation

- Importance of A Trial BalanceDocument1 pageImportance of A Trial Balancedanookyere100% (3)

- Catalog ATEX 2013Document116 pagesCatalog ATEX 2013Lucian AlexandruPas encore d'évaluation

- Management Engr GardeniaDocument3 pagesManagement Engr GardeniaJ'Carlo CarpioPas encore d'évaluation

- Najmi Osconf2009Document30 pagesNajmi Osconf2009Harisfazillah JamelPas encore d'évaluation

- Macha Mani Rajesh: Duties and ResponsibilitiesDocument2 pagesMacha Mani Rajesh: Duties and ResponsibilitiesrajeshPas encore d'évaluation

- S 296001-1 A3 APQP Status Report enDocument2 pagesS 296001-1 A3 APQP Status Report enfdsa01Pas encore d'évaluation

- Daily Booking List - Final Year - Petrochemical Engineering - Electiveregistration PDFDocument1 pageDaily Booking List - Final Year - Petrochemical Engineering - Electiveregistration PDFSamuel Prada SaabomePas encore d'évaluation

- Final ExamDocument8 pagesFinal Examviraivil9417Pas encore d'évaluation

- Statement of Requirements For Seat ManufacturingDocument10 pagesStatement of Requirements For Seat ManufacturingBrian KaweesaPas encore d'évaluation

- Marina MC 2017-04Document10 pagesMarina MC 2017-04PortCallsPas encore d'évaluation

- Chadwick 2010 KDocument5 pagesChadwick 2010 KMarkusMakuAldoPas encore d'évaluation

- Piping Insulation Project Planned Schedule-Rev1Document1 pagePiping Insulation Project Planned Schedule-Rev1Anene EmmanuelPas encore d'évaluation

- CBDocument2 pagesCBSelvaraj SimiyonPas encore d'évaluation

- Greenfield Mass Police Log 02/24/2014 Through 03/02/2014Document59 pagesGreenfield Mass Police Log 02/24/2014 Through 03/02/2014Greenfield Ma PolicePas encore d'évaluation

- Tektronix, Inc.: Global ERP Implementation: Case Write-Up - IIDocument3 pagesTektronix, Inc.: Global ERP Implementation: Case Write-Up - IIkevalPas encore d'évaluation

- Dbms NotesDocument59 pagesDbms NotesRehan SabirPas encore d'évaluation

- COBIT 5 Assessor Course PDFDocument4 pagesCOBIT 5 Assessor Course PDFadseguraPas encore d'évaluation

- ISA Symbology PDFDocument1 pageISA Symbology PDFhanisumar100% (1)

- Mail FormatDocument2 pagesMail FormatHarish KumarPas encore d'évaluation

- AIF - LY23-069 - Eco System - FPIP CWTF 3 - Aeration BlowersDocument11 pagesAIF - LY23-069 - Eco System - FPIP CWTF 3 - Aeration BlowersBrainard ConcordiaPas encore d'évaluation

- UESI Presentation Webinar March 29 2016 PDFDocument65 pagesUESI Presentation Webinar March 29 2016 PDFmunim87Pas encore d'évaluation

- AsDocument19 pagesAshufuents-1Pas encore d'évaluation

- NCHRP RPT 395Document143 pagesNCHRP RPT 395sakashefPas encore d'évaluation

- Tri WheelDocument6 pagesTri WheelAminul HoquePas encore d'évaluation

- Precision MODEL - SL19 - INSTALL01-10-19Document16 pagesPrecision MODEL - SL19 - INSTALL01-10-19Ahmed AbdelftahPas encore d'évaluation