Vous aimerez peut-être aussi

- The 2012 Global Green Economy IndexDocument12 pagesThe 2012 Global Green Economy IndexDual Citizen LLCPas encore d'évaluation

- 2011 Fiat SpA Sustainability ReportDocument268 pages2011 Fiat SpA Sustainability ReportAbarth USAPas encore d'évaluation

- Carrots-And-Sticks - Sustainability Reporting Policies Worldwide Today's Best Practice, Tomorrow's TrendsDocument96 pagesCarrots-And-Sticks - Sustainability Reporting Policies Worldwide Today's Best Practice, Tomorrow's TrendsElbaNereidaAlvarezPas encore d'évaluation

- Samsung Sustainability Report 2011Document94 pagesSamsung Sustainability Report 2011CSRmedia.ro NetworkPas encore d'évaluation

- GRI Based SDR ProposalDocument7 pagesGRI Based SDR ProposalIndrajeetdPas encore d'évaluation

- GRI's Carrots and Sticks ReportDocument96 pagesGRI's Carrots and Sticks ReportTameron EatonPas encore d'évaluation

- Hong Kong Real Estate Issues For Responsible Investors Full ReportDocument92 pagesHong Kong Real Estate Issues For Responsible Investors Full ReportMike WilliamsPas encore d'évaluation

- Global Reporting Initiative GuidelinesDocument19 pagesGlobal Reporting Initiative GuidelinesMonojoy BanerjeePas encore d'évaluation

- The GPM P5 Standard For Sustainability in Project ManagementDocument31 pagesThe GPM P5 Standard For Sustainability in Project ManagementCesar LizarazoPas encore d'évaluation

- Carbon Disclosure ProjectDocument1 pageCarbon Disclosure ProjectDlichrisPas encore d'évaluation

- Globe: Environmental PolicyDocument52 pagesGlobe: Environmental PolicyKlang B.Pas encore d'évaluation

- Triple Bottom Line & GRI Reporting ToolsDocument39 pagesTriple Bottom Line & GRI Reporting ToolsLuis Nash100% (1)

- SAP 2010 sustainability highlightsDocument3 pagesSAP 2010 sustainability highlightsMagdalena PalomaresPas encore d'évaluation

- Clorox Annual Report 2011Document48 pagesClorox Annual Report 2011kirkherePas encore d'évaluation

- Governance for the Sustainable Development Goals: Exploring an Integrative Framework of Theories, Tools, and CompetenciesD'EverandGovernance for the Sustainable Development Goals: Exploring an Integrative Framework of Theories, Tools, and CompetenciesPas encore d'évaluation

- WP Global Value Chain Policy Series Environment Report 2018Document16 pagesWP Global Value Chain Policy Series Environment Report 2018ocnixenPas encore d'évaluation

- NideraDocument56 pagesNideraFlorentina DragnePas encore d'évaluation

- Sustainability Reporting and The Global Reporting InitiativeDocument29 pagesSustainability Reporting and The Global Reporting Initiativeglobal3tPas encore d'évaluation

- 2011 Corporate Citizenship ReportDocument54 pages2011 Corporate Citizenship ReportIhda Arifin FaizPas encore d'évaluation

- ING finances billions in renewable projects through green loans and bondsDocument2 pagesING finances billions in renewable projects through green loans and bondsFelindBularonSaladaPas encore d'évaluation

- Review of Related Literature: Green Industries Best Management PracticesDocument5 pagesReview of Related Literature: Green Industries Best Management PracticesMae CarballoPas encore d'évaluation

- GRI Global OS OverviewDocument2 pagesGRI Global OS OverviewFederico SFPas encore d'évaluation

- Sustainability at Jubilant Life Sciences LimitedDocument13 pagesSustainability at Jubilant Life Sciences Limitedsourav84Pas encore d'évaluation

- Sustainability Report 2012 HighlightsDocument190 pagesSustainability Report 2012 HighlightsJessica AngelinaPas encore d'évaluation

- Ayala LandDocument27 pagesAyala LandAui PaulinoPas encore d'évaluation

- Singapore - An Attractive Location for Expanding BusinessDocument9 pagesSingapore - An Attractive Location for Expanding BusinessNickPas encore d'évaluation

- Corporate Governanceunit 5Document29 pagesCorporate Governanceunit 5socratesonlyPas encore d'évaluation

- 2013 Green Infrastructure Li Position StatementDocument32 pages2013 Green Infrastructure Li Position StatementKarliane MassariPas encore d'évaluation

- KKR - Creating Sustainable ValueDocument54 pagesKKR - Creating Sustainable ValueMariah SharpPas encore d'évaluation

- Business Case For Green Building Report WEB 2013-04-11Document124 pagesBusiness Case For Green Building Report WEB 2013-04-11topsygrielPas encore d'évaluation

- 2019 Global Status Report For Buildings and Constructi OnDocument41 pages2019 Global Status Report For Buildings and Constructi OnJessica R. Molina CastilloPas encore d'évaluation

- What GRI Reporting Tells About Corporate SustainabilityDocument3 pagesWhat GRI Reporting Tells About Corporate SustainabilityAnuja HardahaPas encore d'évaluation

- Corporate Social Responsibility and SustainabilityDocument38 pagesCorporate Social Responsibility and Sustainabilitygua Siapa yaPas encore d'évaluation

- JurnalDocument12 pagesJurnalaprilia islaPas encore d'évaluation

- Presentation of Why Sustainability Reporting Presented at CII KarnatakaDocument43 pagesPresentation of Why Sustainability Reporting Presented at CII Karnatakalathasn6627Pas encore d'évaluation

- ELECTRIC UTILITY ALIGNMENT WITH THE SDGs THE PARIS CLIMDocument34 pagesELECTRIC UTILITY ALIGNMENT WITH THE SDGs THE PARIS CLIMRafael OsunaPas encore d'évaluation

- PRIAnnualReport2020 EnhanceourglobalfootprintDocument7 pagesPRIAnnualReport2020 Enhanceourglobalfootprinttradingjournal888Pas encore d'évaluation

- Sun Hung Kai Properties Limited: Sustainability Report 2014/15Document48 pagesSun Hung Kai Properties Limited: Sustainability Report 2014/15Eddie NgPas encore d'évaluation

- Barclays and AvivaDocument17 pagesBarclays and Avivakunwar showvhaPas encore d'évaluation

- 2013-06-20 Gifford Megatrends MorningDocument23 pages2013-06-20 Gifford Megatrends MorningNils MellquistPas encore d'évaluation

- 50 Innovations To Inspire Bussiness TransformationDocument92 pages50 Innovations To Inspire Bussiness TransformationastronautasPas encore d'évaluation

- Sustainability Vision: Vision An Opportunity To Do BetterDocument17 pagesSustainability Vision: Vision An Opportunity To Do Betterjuan gualdronPas encore d'évaluation

- 22 Dbs 06 T 32 PsDocument6 pages22 Dbs 06 T 32 PscarlriiberknudsenPas encore d'évaluation

- The Alphabet Soup of ESG ReportingDocument3 pagesThe Alphabet Soup of ESG ReportingkushagraPas encore d'évaluation

- Inditex Group Annual Report 2013 PDFDocument296 pagesInditex Group Annual Report 2013 PDFNataliaKostyshakPas encore d'évaluation

- The Impact of Sustainability (Environmental, Social, and Governance) Disclosure and Board Diversity On Firm Value - The Moderating Role of Industry SensitivityDocument16 pagesThe Impact of Sustainability (Environmental, Social, and Governance) Disclosure and Board Diversity On Firm Value - The Moderating Role of Industry SensitivityHENI YUSNITAPas encore d'évaluation

- WPP Sr12 IntroductionDocument5 pagesWPP Sr12 IntroductiondaniellemuntyanPas encore d'évaluation

- Indesit Sustainability Report 2012Document79 pagesIndesit Sustainability Report 2012CSRMedia NetworkPas encore d'évaluation

- Progress Through Partnership 2013 Esg and Citizenship Report Progress Through Partnership 2013 Esg and Citizenship ReportDocument55 pagesProgress Through Partnership 2013 Esg and Citizenship Report Progress Through Partnership 2013 Esg and Citizenship ReportsupersethPas encore d'évaluation

- A Snapshot of Sustainability Reporting in The Construction Real Estate SectorDocument15 pagesA Snapshot of Sustainability Reporting in The Construction Real Estate SectorFernando PauwelsPas encore d'évaluation

- Global Reporting InitiativeDocument57 pagesGlobal Reporting Initiativesurbhimo100% (1)

- Green Real Estate: Does It Create Value? Financial and Sustainability Analysis On European Green ReitsDocument13 pagesGreen Real Estate: Does It Create Value? Financial and Sustainability Analysis On European Green ReitsCarolina MacielPas encore d'évaluation

- Accounting Assignment GroupDocument1 pageAccounting Assignment GroupTùng Linh TrầnPas encore d'évaluation

- Henkel Sustainability Report 2013 enDocument54 pagesHenkel Sustainability Report 2013 enCSRMedia NetworkPas encore d'évaluation

- Framework Sustainability Business TheoryDocument3 pagesFramework Sustainability Business TheoryElla KinaPas encore d'évaluation

- Inclusive Green Growth Index: A New Benchmark for Quality of GrowthD'EverandInclusive Green Growth Index: A New Benchmark for Quality of GrowthPas encore d'évaluation

- Asia’s Progress toward Greater Sustainable Finance Market Efficiency and IntegrityD'EverandAsia’s Progress toward Greater Sustainable Finance Market Efficiency and IntegrityPas encore d'évaluation

- Nihms128437Document18 pagesNihms128437maywayrandomPas encore d'évaluation

- Light at Night Increases Body Mass by Shifting Time of Food IntakeDocument6 pagesLight at Night Increases Body Mass by Shifting Time of Food IntakemaywayrandomPas encore d'évaluation

- International Symposium On Total Worker Health: ST TMDocument3 pagesInternational Symposium On Total Worker Health: ST TMmaywayrandomPas encore d'évaluation

- IHCM Foundation - Wellness FINAL Electonic VersionDocument23 pagesIHCM Foundation - Wellness FINAL Electonic VersionmaywayrandomPas encore d'évaluation

- Ecovent - Under Pressure Whitepaper WebDocument14 pagesEcovent - Under Pressure Whitepaper Webmaywayrandom100% (1)

- Gallup-In U.S., Engaged Employees Exercise More, Eat HealthierDocument4 pagesGallup-In U.S., Engaged Employees Exercise More, Eat HealthiermaywayrandomPas encore d'évaluation

- Iscebs Benefits QuarterlyDocument12 pagesIscebs Benefits QuarterlymaywayrandomPas encore d'évaluation

- Internet of ThingsDocument23 pagesInternet of ThingsbarmilliPas encore d'évaluation

- NanoSilver Health RisksDocument27 pagesNanoSilver Health RisksmaywayrandomPas encore d'évaluation

- Mattress Manufacturing in The US Industry ReportDocument40 pagesMattress Manufacturing in The US Industry Reportmaywayrandom100% (1)

- Survey BizofHealthyEEs15Document17 pagesSurvey BizofHealthyEEs15maywayrandomPas encore d'évaluation

- Fidelty-Health Care Survey Finds SpendingDocument2 pagesFidelty-Health Care Survey Finds SpendingmaywayrandomPas encore d'évaluation

- HERO ScorecardDocument32 pagesHERO ScorecardmaywayrandomPas encore d'évaluation

- GCP Creating Successful Wellness Incentives - Original PDFDocument15 pagesGCP Creating Successful Wellness Incentives - Original PDFmaywayrandomPas encore d'évaluation

- Sample ActionPlan2 3Document23 pagesSample ActionPlan2 3maywayrandomPas encore d'évaluation

- Roi of Engagement-JiffDocument5 pagesRoi of Engagement-JiffmaywayrandomPas encore d'évaluation

- Johns Hopkins - IHPS - CITI StudyDocument2 pagesJohns Hopkins - IHPS - CITI StudymaywayrandomPas encore d'évaluation

- Employee Wellness Programs Buyer's GuideDocument15 pagesEmployee Wellness Programs Buyer's GuidemaywayrandomPas encore d'évaluation

- Johns Hopkins - IHPS - JNJ StudyDocument2 pagesJohns Hopkins - IHPS - JNJ StudymaywayrandomPas encore d'évaluation

- On Solid GroundDocument12 pagesOn Solid GroundmaywayrandomPas encore d'évaluation

- JLL Asia Pacific Property Digest 3q 2014Document76 pagesJLL Asia Pacific Property Digest 3q 2014maywayrandomPas encore d'évaluation

- The Real Estate Development MatrixDocument27 pagesThe Real Estate Development MatrixTvan Bao100% (5)

- Bank CEOs Advocate LGBT Rights Abroad Behind ScenesDocument2 pagesBank CEOs Advocate LGBT Rights Abroad Behind ScenesmaywayrandomPas encore d'évaluation

- JLL Asia Pacific Property Digest 2q 2014Document72 pagesJLL Asia Pacific Property Digest 2q 2014maywayrandomPas encore d'évaluation

- Fed Feels Heat To Tailor Capital Rules For Nonbank FirmsDocument3 pagesFed Feels Heat To Tailor Capital Rules For Nonbank FirmsmaywayrandomPas encore d'évaluation

- Regulators Tell Smaller Banks Not To Follow Zions' Lead On Volcker RuleDocument2 pagesRegulators Tell Smaller Banks Not To Follow Zions' Lead On Volcker RulemaywayrandomPas encore d'évaluation

- Real Estate Private Equity NewsletterDocument7 pagesReal Estate Private Equity NewslettermaywayrandomPas encore d'évaluation

- FICO To Add Hadoop Support To Its Analytics Cloud: Amilda DymiDocument1 pageFICO To Add Hadoop Support To Its Analytics Cloud: Amilda DymimaywayrandomPas encore d'évaluation

- Regulators Seek Stiffer Capital Rules for Large BanksDocument3 pagesRegulators Seek Stiffer Capital Rules for Large BanksmaywayrandomPas encore d'évaluation

- Forest Restoration and Rehabilitation in PHDocument45 pagesForest Restoration and Rehabilitation in PHakosiwillyPas encore d'évaluation

- IAS 2 InventoriesDocument13 pagesIAS 2 InventoriesFritz MainarPas encore d'évaluation

- Comparative Analysis of Broking FirmsDocument12 pagesComparative Analysis of Broking FirmsJames RamirezPas encore d'évaluation

- Original PDF Global Problems and The Culture of Capitalism Books A La Carte 7th EditionDocument61 pagesOriginal PDF Global Problems and The Culture of Capitalism Books A La Carte 7th Editioncarla.campbell348100% (41)

- RenatoPolimeno Resume 2010 v01Document2 pagesRenatoPolimeno Resume 2010 v01Isabela RodriguesPas encore d'évaluation

- Investment Opportunities in Bosnia and Herzegovina 2016Document69 pagesInvestment Opportunities in Bosnia and Herzegovina 2016Elvir Harun Ibrovic100% (1)

- Seminar Paper11111Document22 pagesSeminar Paper11111Mulugeta88% (8)

- ReidtaylorDocument326 pagesReidtayloralankriti12345Pas encore d'évaluation

- Money Market and Its InstrumentsDocument8 pagesMoney Market and Its InstrumentsKIRANMAI CHENNURUPas encore d'évaluation

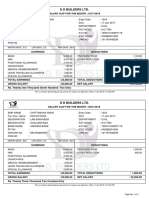

- Pay - Slip Oct. & Nov. 19Document1 pagePay - Slip Oct. & Nov. 19Atul Kumar MishraPas encore d'évaluation

- Economics For Everyone: Problem Set 2Document4 pagesEconomics For Everyone: Problem Set 2kogea2Pas encore d'évaluation

- KjujDocument17 pagesKjujMohamed KamalPas encore d'évaluation

- SymbolsDocument8 pagesSymbolsMaría GrilloPas encore d'évaluation

- Strategic Planning For Small Business: Presented By: Mary Ann Dimco Raul de La Cruz Iii Faith Cabando Bsba 2-ADocument26 pagesStrategic Planning For Small Business: Presented By: Mary Ann Dimco Raul de La Cruz Iii Faith Cabando Bsba 2-Amary ann dimcoPas encore d'évaluation

- G20 Leaders to Agree on Trade, CurrencyDocument5 pagesG20 Leaders to Agree on Trade, CurrencysunitbagadePas encore d'évaluation

- Chapter - 9 Multifactor ModelsDocument15 pagesChapter - 9 Multifactor ModelsAntora Hoque100% (1)

- 2022-11-13 2bat TDR Francesc MorenoDocument76 pages2022-11-13 2bat TDR Francesc MorenoFrancesc Moreno MorataPas encore d'évaluation

- Provident Fund InformationDocument2 pagesProvident Fund Informationsk_gazanfarPas encore d'évaluation

- Balance StatementDocument5 pagesBalance Statementmichael anthonyPas encore d'évaluation

- 5014 Environmental Management: MARK SCHEME For The May/June 2015 SeriesDocument3 pages5014 Environmental Management: MARK SCHEME For The May/June 2015 Seriesmuti rehmanPas encore d'évaluation

- Social ResponsibilityDocument2 pagesSocial ResponsibilityAneeq Raheem100% (1)

- Research Article StudyDocument2 pagesResearch Article StudyRica Mae DacoyloPas encore d'évaluation

- Far QuizDocument7 pagesFar QuizMeldred EcatPas encore d'évaluation

- Characteristics and Economic Outlook of Indonesia in the Globalization EraDocument63 pagesCharacteristics and Economic Outlook of Indonesia in the Globalization EraALIFAHPas encore d'évaluation

- 20 Years of Ecotourism Letter From DR Kelly BrickerDocument1 page20 Years of Ecotourism Letter From DR Kelly BrickerThe International Ecotourism SocietyPas encore d'évaluation

- Data 73Document4 pagesData 73Abhijit BarmanPas encore d'évaluation

- List of Companies: Group - 1 (1-22)Document7 pagesList of Companies: Group - 1 (1-22)Mohammad ShuaibPas encore d'évaluation

- AssignmentDocument8 pagesAssignmentnaabbasiPas encore d'évaluation

- Foreign Employment and Remittance in NepalDocument19 pagesForeign Employment and Remittance in Nepalsecondarydomainak6Pas encore d'évaluation

- Bilateral Trade Between Bangladesh and IndiaDocument30 pagesBilateral Trade Between Bangladesh and IndiaAnika ParvinPas encore d'évaluation