Vous aimerez peut-être aussi

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- IRS Exposed-Puerto Rican TrustDocument37 pagesIRS Exposed-Puerto Rican TrustJeff MaehrPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Exhibit C - Sovereignty of The People Above GovernmentsDocument5 pagesExhibit C - Sovereignty of The People Above GovernmentsJeff MaehrPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Vaccine Death ReportDocument39 pagesThe Vaccine Death ReportJeff Maehr75% (12)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Brunson v. Alma S. Adams Et Al - OcrDocument18 pagesBrunson v. Alma S. Adams Et Al - OcrJeff Maehr100% (1)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Institute For Pure and Applied Knowledge's Case Against CDC's LawbreakingDocument25 pagesThe Institute For Pure and Applied Knowledge's Case Against CDC's LawbreakingTim Brown100% (3)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Mask Fraud Links-2Document4 pagesMask Fraud Links-2Jeff MaehrPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- IRS Pre-Assessment Document FOIA RequestDocument8 pagesIRS Pre-Assessment Document FOIA RequestJeff MaehrPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Straw Man-Mem of LawDocument27 pagesStraw Man-Mem of LawJeff Maehr100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Amended Complaint Against US State Dept For Unconstitutional Passport RevocationDocument12 pagesAmended Complaint Against US State Dept For Unconstitutional Passport RevocationJeff MaehrPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- SupCt Petition For Writ On IRS Tax Fraud On AmericansDocument88 pagesSupCt Petition For Writ On IRS Tax Fraud On AmericansJeff MaehrPas encore d'évaluation

- Appeal Final Reply To ResponseDocument27 pagesAppeal Final Reply To ResponseJeff MaehrPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Freedom of Information Act (FOIA) Violation ComplaintDocument26 pagesFreedom of Information Act (FOIA) Violation ComplaintJeff MaehrPas encore d'évaluation

- Zip Codes Federal Fraud of JurisdictionDocument4 pagesZip Codes Federal Fraud of JurisdictionJeff Maehr100% (1)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Motion For Summons of Grand JuryDocument14 pagesMotion For Summons of Grand JuryJeff Maehr100% (2)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Reply To Govt IRS Response FinalDocument39 pagesReply To Govt IRS Response FinalJeff Maehr100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- 16th Amendment Did Not Authorize Income Taxes-9-27-16Document6 pages16th Amendment Did Not Authorize Income Taxes-9-27-16Jeff Maehr100% (1)

- Appeal Motion For Rehearing en Banc 10-28-16Document6 pagesAppeal Motion For Rehearing en Banc 10-28-16Jeff MaehrPas encore d'évaluation

- Appeals Opening Brief Court Stamped FiledDocument34 pagesAppeals Opening Brief Court Stamped FiledJeff MaehrPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

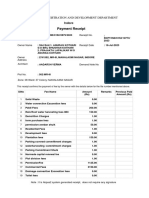

- Payment Receipt: Urban Administration and Development DepartmentDocument2 pagesPayment Receipt: Urban Administration and Development Departmentaadarsh vermaPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Income Tax Return Form-1 Sahaj - Excel FormatDocument9 pagesIncome Tax Return Form-1 Sahaj - Excel Formatswapnil007salunkePas encore d'évaluation

- Jurisprudence-Pacta Sunt ServandaDocument3 pagesJurisprudence-Pacta Sunt ServandaMavisJamesPas encore d'évaluation

- Question No: 2Document18 pagesQuestion No: 2Rameez AbbasiPas encore d'évaluation

- J.B. Hunt Transport, Inc. 615 J B Hunt Corporate Drive Lowell, AR 72745 +1 (479) 820-0000Document1 pageJ.B. Hunt Transport, Inc. 615 J B Hunt Corporate Drive Lowell, AR 72745 +1 (479) 820-0000Anonymous w4gxCdLPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Mobile Services: Your Account Summary This Month'S ChargesDocument3 pagesMobile Services: Your Account Summary This Month'S Chargesjigyesh sharmaPas encore d'évaluation

- Mechanics 123999Document3 pagesMechanics 123999Momonew TalismanPas encore d'évaluation

- Franchise Accounting - DoneDocument3 pagesFranchise Accounting - DoneJymldy EnclnPas encore d'évaluation

- Vetan Deyak Praptra Vittiya Niyam Sangrah, Khand-5, Bhag-1 See Chapter 6 Para-108, Chapter 7 Para-131Document9 pagesVetan Deyak Praptra Vittiya Niyam Sangrah, Khand-5, Bhag-1 See Chapter 6 Para-108, Chapter 7 Para-131Madan ChaturvediPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Name: Ali Ahmad Sabir Name: Ali Ahmad Sabir Name: Ali Ahmad Sabir Name: Ali Ahmad SabirDocument1 pageName: Ali Ahmad Sabir Name: Ali Ahmad Sabir Name: Ali Ahmad Sabir Name: Ali Ahmad SabirRanja JePas encore d'évaluation

- As485070 Dec2022 PayslipDocument2 pagesAs485070 Dec2022 PayslipAKM Enterprises Pvt LtdPas encore d'évaluation

- Dayang Norita Binti Awang Bujang Lorong 2C Lorong 2C 7 Lorong 2C, JLN Tung Yee 96100, SARIKEI, SARDocument3 pagesDayang Norita Binti Awang Bujang Lorong 2C Lorong 2C 7 Lorong 2C, JLN Tung Yee 96100, SARIKEI, SARgoku sonPas encore d'évaluation

- EXCLUSIONSDocument8 pagesEXCLUSIONSMeliodas SamaPas encore d'évaluation

- Retirement Withdrawal CalculatorDocument17 pagesRetirement Withdrawal CalculatorSanjeev NehruPas encore d'évaluation

- SAP CIN ProcedureDocument9 pagesSAP CIN Procedurebharti2485100% (1)

- Acct Statement - XX3589 - 24112022Document2 pagesAcct Statement - XX3589 - 24112022Udit KumarPas encore d'évaluation

- MZ Ex NTK 0 MZ UDocument2 pagesMZ Ex NTK 0 MZ UUsman AhmedPas encore d'évaluation

- Standard Accounts: IntroducingDocument24 pagesStandard Accounts: IntroducingsathishPas encore d'évaluation

- Airline Academy India: English Question PaperDocument3 pagesAirline Academy India: English Question PaperGaming With VoltPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- CIBC Bank LKRDocument2 pagesCIBC Bank LKRJames HacherPas encore d'évaluation

- My Sip 2021-22Document28 pagesMy Sip 2021-22Xenqiyj XyenttukPas encore d'évaluation

- Please Confirm DUTY/TAXES Payment X: Notice For Shipment Clearance NoDocument2 pagesPlease Confirm DUTY/TAXES Payment X: Notice For Shipment Clearance NoAngie Tan100% (1)

- Bank StatementDocument3 pagesBank Statementapexindustries5199100% (1)

- eBTAC 100Document66 pageseBTAC 100Maria Christina Hiceta Maynes100% (1)

- LBR JWB Sesi 2 - MEDIKA ADIJAYA - 2021Document13 pagesLBR JWB Sesi 2 - MEDIKA ADIJAYA - 2021Sandi RiswandiPas encore d'évaluation

- GIRO - FAST WITH INV - V1.5 (With PayNow)Document7 pagesGIRO - FAST WITH INV - V1.5 (With PayNow)chriskhohkPas encore d'évaluation

- FEES SCHEDULE 2011 - 2012: Australian International SchoolDocument2 pagesFEES SCHEDULE 2011 - 2012: Australian International SchoollephammydungPas encore d'évaluation

- Chap 0005Document25 pagesChap 0005HadiPas encore d'évaluation

- Negotin Bar Exam QuestionsDocument13 pagesNegotin Bar Exam QuestionsVenz LacrePas encore d'évaluation

- Income Tax Midterm ExamDocument9 pagesIncome Tax Midterm ExamhyasPas encore d'évaluation