Vous aimerez peut-être aussi

- Working With Project Planning and Management SoftwareDocument10 pagesWorking With Project Planning and Management Softwaresadiqaftab786Pas encore d'évaluation

- The Origins of The S Curve in Business FunctionsDocument4 pagesThe Origins of The S Curve in Business Functionssadiqaftab786Pas encore d'évaluation

- S-Curve Analysis - Project LifecycleDocument9 pagesS-Curve Analysis - Project Lifecyclesrkumar_bePas encore d'évaluation

- Tcf2007 DK RDGDocument9 pagesTcf2007 DK RDGsadiqaftab786Pas encore d'évaluation

- E2 EM Chapter 7Document50 pagesE2 EM Chapter 7Str Engr Mohammad AliPas encore d'évaluation

- The Monal MenuDocument9 pagesThe Monal Menusadiqaftab786Pas encore d'évaluation

- Scurve231 M enDocument20 pagesScurve231 M ensadiqaftab786Pas encore d'évaluation

- S Curve Tutorial1Document7 pagesS Curve Tutorial1sadiqaftab786Pas encore d'évaluation

- Isarc2007-4.3 2 065Document4 pagesIsarc2007-4.3 2 065sadiqaftab786Pas encore d'évaluation

- Innovation LifecyclesDocument4 pagesInnovation Lifecyclessadiqaftab786Pas encore d'évaluation

- S CurveDocument12 pagesS Curvesadiqaftab786Pas encore d'évaluation

- Isarc2007-4.3 2 065Document4 pagesIsarc2007-4.3 2 065sadiqaftab786Pas encore d'évaluation

- The S Curves Made Easy With Oracle Primavera P6Document7 pagesThe S Curves Made Easy With Oracle Primavera P6sadiqaftab786Pas encore d'évaluation

- Exploring The Limits of The Technology S-CurveDocument24 pagesExploring The Limits of The Technology S-Curvesadiqaftab786Pas encore d'évaluation

- On Algorithms For Planning S-Curve Motion ProfilesDocument8 pagesOn Algorithms For Planning S-Curve Motion Profilessadiqaftab786Pas encore d'évaluation

- Gartner Maturity and Adoption-1Document22 pagesGartner Maturity and Adoption-1sadiqaftab786Pas encore d'évaluation

- Easec13 E 3 1Document8 pagesEasec13 E 3 1sadiqaftab786Pas encore d'évaluation

- S CurveDocument4 pagesS CurveArindam MitraPas encore d'évaluation

- S-Curve Dynamics of Trade: Evidence From US-Canada Commodity TradeDocument16 pagesS-Curve Dynamics of Trade: Evidence From US-Canada Commodity TradeUyen DongPas encore d'évaluation

- Brice DatteeDocument36 pagesBrice Datteesadiqaftab786Pas encore d'évaluation

- S CurveDocument12 pagesS CurvethlsatheeshPas encore d'évaluation

- 1005 2122Document19 pages1005 2122sadiqaftab786Pas encore d'évaluation

- 2007 02tDocument30 pages2007 02tsadiqaftab786Pas encore d'évaluation

- 1005 2122Document19 pages1005 2122sadiqaftab786Pas encore d'évaluation

- Planning Engineer ResumeDocument4 pagesPlanning Engineer Resumesadiqaftab7860% (1)

- Human Resource ManagementDocument16 pagesHuman Resource Managementsadiqaftab786Pas encore d'évaluation

- Oxford English Testing LMSDocument1 pageOxford English Testing LMSsadiqaftab7860% (1)

- 73Document19 pages73sadiqaftab786Pas encore d'évaluation

- Tibb e NabviS.a.W Aur Jadeed Science Vol 1Document353 pagesTibb e NabviS.a.W Aur Jadeed Science Vol 1sadiqaftab786Pas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

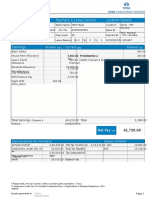

- Employee Details Payment & Leave Details Location Details: Arrears Current AmountDocument1 pageEmployee Details Payment & Leave Details Location Details: Arrears Current AmountSanjeev ChoudhuryPas encore d'évaluation

- 2008 Publication 553 Highlights of 2008 Tax ChangesDocument38 pages2008 Publication 553 Highlights of 2008 Tax ChangesgrosofPas encore d'évaluation

- HW Questions Income TaxDocument34 pagesHW Questions Income TaxAina Niaz100% (1)

- The Oriental Insurance Company LimitedDocument3 pagesThe Oriental Insurance Company Limitedpooja boraPas encore d'évaluation

- FPDI PDF Parser LicenseDocument4 pagesFPDI PDF Parser LicensesohinPas encore d'évaluation

- Proy Balotario Preguntas II 20140611Document31 pagesProy Balotario Preguntas II 20140611Clau OrunaPas encore d'évaluation

- Insurance C OutlineDocument3 pagesInsurance C OutlineStanley SitholePas encore d'évaluation

- When Does Time Start Running For A Claim Under An Indemnity?Document3 pagesWhen Does Time Start Running For A Claim Under An Indemnity?AVChecchiPas encore d'évaluation

- Table of Tax ComparisonDocument5 pagesTable of Tax ComparisonJessica RoncesvallesPas encore d'évaluation

- B2100148 - Dell EMC PowerScale A300Document17 pagesB2100148 - Dell EMC PowerScale A300Le ThienPas encore d'évaluation

- Standard Contract AmendmentsDocument66 pagesStandard Contract Amendmentsmarx0506Pas encore d'évaluation

- CV-Aniruddha Sen V 4.0Document5 pagesCV-Aniruddha Sen V 4.0Ajay PradhanPas encore d'évaluation

- Ayushi MishraDocument100 pagesAyushi Mishraravi singhPas encore d'évaluation

- K Municipal Plan. & Dev. Coordinator KDocument32 pagesK Municipal Plan. & Dev. Coordinator KMary Jane Katipunan CalumbaPas encore d'évaluation

- Consumer RightsDocument88 pagesConsumer RightsMathangi JeyaramanPas encore d'évaluation

- Duties of A Personal Representative in Georgia Probate CourtDocument10 pagesDuties of A Personal Representative in Georgia Probate CourtSean McEvoy100% (1)

- Three Palms Pointe, Inc. v. State Farm Fire, 362 F.3d 1317, 11th Cir. (2004)Document3 pagesThree Palms Pointe, Inc. v. State Farm Fire, 362 F.3d 1317, 11th Cir. (2004)Scribd Government DocsPas encore d'évaluation

- Birla SunlifeDocument27 pagesBirla SunlifeVinney KumarPas encore d'évaluation

- Health Care USA Chapter 5Document52 pagesHealth Care USA Chapter 5David Turner100% (1)

- Insurance Meaning, Insurance Act 1938Document23 pagesInsurance Meaning, Insurance Act 1938KARISHMAAT100% (1)

- Rule: Income Taxes: Life-Nonlife Consolidated Returns Tacking Rule RequirementsDocument2 pagesRule: Income Taxes: Life-Nonlife Consolidated Returns Tacking Rule RequirementsJustia.comPas encore d'évaluation

- Analytics: Turning Data Into DollarsDocument20 pagesAnalytics: Turning Data Into DollarsDeloitte Analytics100% (10)

- Reliance Nippon Life Insurance Appoints Mr. Ashish Vohra As New CEO (Company Update)Document3 pagesReliance Nippon Life Insurance Appoints Mr. Ashish Vohra As New CEO (Company Update)Shyam SunderPas encore d'évaluation

- Characteristics of Indigenous BankersDocument4 pagesCharacteristics of Indigenous BankersAnonymous MyMFvSmRPas encore d'évaluation

- 04 04 FIG Questions AnswersDocument65 pages04 04 FIG Questions AnswersAbcdef100% (2)

- OSFI - MCT Guidelines 2011Document46 pagesOSFI - MCT Guidelines 2011Roff AubPas encore d'évaluation

- CrediT TransactionsDocument4 pagesCrediT TransactionsDa YePas encore d'évaluation

- Joint Venture AgreementDocument8 pagesJoint Venture AgreementMatthew DadaPas encore d'évaluation

- Summer Internship ReportDocument77 pagesSummer Internship ReportNicole RobinsonPas encore d'évaluation