Vous aimerez peut-être aussi

- Ict and Rural PeopleDocument6 pagesIct and Rural PeopleSatyendra ChauhanPas encore d'évaluation

- Internet addiction linked to depression in adolescentsDocument3 pagesInternet addiction linked to depression in adolescentsSatyendra Chauhan100% (1)

- Cheating and Forgery CaseDocument14 pagesCheating and Forgery CaseSatyendra Chauhan100% (1)

- 356 IPC CaseDocument8 pages356 IPC CaseSatyendra ChauhanPas encore d'évaluation

- In The Court of District & Session Judge, Tis Hazari, Courts, Delhi Case No. of 2016 Memo of Parties in The Matter ofDocument2 pagesIn The Court of District & Session Judge, Tis Hazari, Courts, Delhi Case No. of 2016 Memo of Parties in The Matter ofSatyendra ChauhanPas encore d'évaluation

- Court Judgment ConvictionDocument9 pagesCourt Judgment ConvictionSatyendra ChauhanPas encore d'évaluation

- Polixy RoasterDocument2 pagesPolixy RoasterSatyendra ChauhanPas encore d'évaluation

- 12 Books That Will Make You Feel Extreme Emotions - WhytoRead BooksDocument10 pages12 Books That Will Make You Feel Extreme Emotions - WhytoRead BooksSatyendra ChauhanPas encore d'évaluation

- Jagdeo Prasad Vs StateDocument2 pagesJagdeo Prasad Vs StateSatyendra ChauhanPas encore d'évaluation

- Chapter 13 Reservation PolicyDocument95 pagesChapter 13 Reservation PolicySandip LulekarPas encore d'évaluation

- Arms Act CaseDocument12 pagesArms Act CaseSatyendra ChauhanPas encore d'évaluation

- Rash and Negligen DrivingDocument8 pagesRash and Negligen DrivingSatyendra ChauhanPas encore d'évaluation

- Suit Order Amending Plaint Adding EvidenceDocument4 pagesSuit Order Amending Plaint Adding EvidenceSatyendra ChauhanPas encore d'évaluation

- Judgment of Delhi High CourtDocument10 pagesJudgment of Delhi High CourtSatyendra ChauhanPas encore d'évaluation

- O 12 R 6Document15 pagesO 12 R 6Satyendra ChauhanPas encore d'évaluation

- Court allows withdrawal of withdrawal applicationDocument5 pagesCourt allows withdrawal of withdrawal applicationSatyendra ChauhanPas encore d'évaluation

- O 10 R2Document9 pagesO 10 R2Satyendra ChauhanPas encore d'évaluation

- O 37 R17Document4 pagesO 37 R17Satyendra ChauhanPas encore d'évaluation

- O 7 R11Document4 pagesO 7 R11Satyendra ChauhanPas encore d'évaluation

- O 1 R10Document4 pagesO 1 R10Satyendra ChauhanPas encore d'évaluation

- Court Quashes Dowry Case Due to Spousal ReconciliationDocument6 pagesCourt Quashes Dowry Case Due to Spousal ReconciliationSatyendra ChauhanPas encore d'évaluation

- Delhi HC bail hearing details in CBI case under Official Secrets ActDocument13 pagesDelhi HC bail hearing details in CBI case under Official Secrets ActSatyendra ChauhanPas encore d'évaluation

- Vinay Vs StateDocument6 pagesVinay Vs StateSatyendra ChauhanPas encore d'évaluation

- High Court Writ PetitionDocument71 pagesHigh Court Writ PetitionSatyendra ChauhanPas encore d'évaluation

- Ravinder Vs StateDocument7 pagesRavinder Vs StateSatyendra ChauhanPas encore d'évaluation

- Videocon Vs GailDocument4 pagesVideocon Vs GailSatyendra ChauhanPas encore d'évaluation

- Brij Pal Vs StateDocument7 pagesBrij Pal Vs StateSatyendra ChauhanPas encore d'évaluation

- Delhi HC Quashes FIR in Matrimonial Dispute CaseDocument6 pagesDelhi HC Quashes FIR in Matrimonial Dispute CaseSatyendra ChauhanPas encore d'évaluation

- Rajesh Bajaj Vs StateDocument6 pagesRajesh Bajaj Vs StateSatyendra ChauhanPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Poland Country VersionDocument44 pagesPoland Country VersionAlbert A. SusinskasPas encore d'évaluation

- High-Tech Semiconductor Industry Solutions: Oracle E-Business SuiteDocument11 pagesHigh-Tech Semiconductor Industry Solutions: Oracle E-Business Suitekpankaj7253Pas encore d'évaluation

- How To Configure Ebtax For Vat TaxDocument17 pagesHow To Configure Ebtax For Vat TaxKaushik BosePas encore d'évaluation

- OpenText VIM e InvoicingDocument34 pagesOpenText VIM e InvoicingTJPas encore d'évaluation

- Revenue Recognition With EBSDocument29 pagesRevenue Recognition With EBSSunil KumarPas encore d'évaluation

- MXA000015Document68 pagesMXA000015Nancy ReyesPas encore d'évaluation

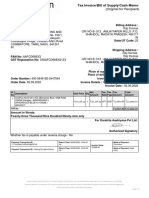

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)RoxdPas encore d'évaluation

- Report Anomalies and Normalization SummaryDocument5 pagesReport Anomalies and Normalization SummaryThomas_GodricPas encore d'évaluation

- SAP-Shortcut KeysDocument56 pagesSAP-Shortcut KeysAnandPas encore d'évaluation

- © 2009 Oracle Corporation - Proprietary and ConfidentialDocument57 pages© 2009 Oracle Corporation - Proprietary and Confidentialkhaleel ofcPas encore d'évaluation

- JD Edwards EnterpriseOne - Accounts Receivable DraftsDocument67 pagesJD Edwards EnterpriseOne - Accounts Receivable DraftsPedro JuaPas encore d'évaluation

- Sales & Service TaxDocument13 pagesSales & Service TaxWeiling TanPas encore d'évaluation

- Atlas Mining VAT Refund CaseDocument35 pagesAtlas Mining VAT Refund CaseDaley CatugdaPas encore d'évaluation

- Per 19 BC 2018 VS Per 9 BC 2021Document8 pagesPer 19 BC 2018 VS Per 9 BC 2021yuliaPas encore d'évaluation

- View your Singtel bill overview and total dueDocument3 pagesView your Singtel bill overview and total duepallab2110Pas encore d'évaluation

- Tax CDocument18 pagesTax Calmira garciaPas encore d'évaluation

- Tax Invoice: S3948174-1 Gary Bailey La Fontanilla 97 14470 EL VISODocument1 pageTax Invoice: S3948174-1 Gary Bailey La Fontanilla 97 14470 EL VISOCarlos Sobral100% (1)

- Advanced Collections 20A Student GuideDocument232 pagesAdvanced Collections 20A Student Guidesuvendu mishraPas encore d'évaluation

- GST Tax Invoice Format For Goods - TeachooDocument2 pagesGST Tax Invoice Format For Goods - TeachooAshish Kamthania SaxenaPas encore d'évaluation

- NormalizationDocument5 pagesNormalizationSowmi DaaluPas encore d'évaluation

- Unit 8 OrdersDocument17 pagesUnit 8 OrdersLuis De La cruz BarriosPas encore d'évaluation

- rpt6422 4499461Document2 pagesrpt6422 4499461D VrkPas encore d'évaluation

- Triumph Gate Technologies: 3 Floor, Nagasuri Plaza, Bank of India, AmeerpetDocument6 pagesTriumph Gate Technologies: 3 Floor, Nagasuri Plaza, Bank of India, Ameerpethemanth kumar100% (1)

- Subject Areas For Transactional Business Intelligence in FinancialsDocument338 pagesSubject Areas For Transactional Business Intelligence in FinancialsrameshPas encore d'évaluation

- User Guide Rpfieu Saft Saft 1.08 enDocument83 pagesUser Guide Rpfieu Saft Saft 1.08 enMafalda Soraia Sousa Jacinto100% (1)

- BA9228-Business Application Software - II - Anna University Chennai MBA Second Semester Syllabus Regulation 2009Document5 pagesBA9228-Business Application Software - II - Anna University Chennai MBA Second Semester Syllabus Regulation 2009Aswin SivaramakrishnanPas encore d'évaluation

- Computation of Adjusted Inventory and Related Accounts2Document4 pagesComputation of Adjusted Inventory and Related Accounts2CJ alandyPas encore d'évaluation

- AmazonDocument2 pagesAmazongoldmine20233Pas encore d'évaluation

- SAP FB70 & FB75 Transaction Code Tutorials: Customer Invoice and Credit Memo PostingDocument14 pagesSAP FB70 & FB75 Transaction Code Tutorials: Customer Invoice and Credit Memo PostingERPDocs100% (6)

- Business Partner - Customer-Vendor Integration S - 4 HANA - SAP BlogsDocument19 pagesBusiness Partner - Customer-Vendor Integration S - 4 HANA - SAP BlogsrobnunesPas encore d'évaluation