Vous aimerez peut-être aussi

- Introduction to Negotiable Instruments: As per Indian LawsD'EverandIntroduction to Negotiable Instruments: As per Indian LawsÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Banking Ombudsman Scheme 2006Document27 pagesThe Banking Ombudsman Scheme 2006Gurpreet SinghPas encore d'évaluation

- The Banking Ombudsman Scheme 2006 Reserve Bank of India Central Office MumbaiDocument15 pagesThe Banking Ombudsman Scheme 2006 Reserve Bank of India Central Office MumbaiRuchi ChaudharyPas encore d'évaluation

- Banking OmbudsmanDocument14 pagesBanking OmbudsmanAarti MaanPas encore d'évaluation

- The Banking Ombudsman Scheme, 2002Document21 pagesThe Banking Ombudsman Scheme, 2002Meghna MalhotraPas encore d'évaluation

- Banking OmbudsmanDocument26 pagesBanking OmbudsmanVIVEKPas encore d'évaluation

- Banking Ombudsman SchemeDocument27 pagesBanking Ombudsman SchemeRajiv AnanthamurthyPas encore d'évaluation

- Banking Ombudsman Scheme-2006Document50 pagesBanking Ombudsman Scheme-2006advkrishnagandhiPas encore d'évaluation

- Banking OmbudsmanDocument4 pagesBanking Ombudsmananon_41410895Pas encore d'évaluation

- The Reserve Bank - Integrated Ombudsman Scheme, 2021Document18 pagesThe Reserve Bank - Integrated Ombudsman Scheme, 2021Sagnik GangopadhyayPas encore d'évaluation

- RBI Integrates Banking, NBFC and Digital Ombudsman SchemesDocument19 pagesRBI Integrates Banking, NBFC and Digital Ombudsman SchemesAnup KPas encore d'évaluation

- Analysis of The Banking Ombudsman SchemeDocument44 pagesAnalysis of The Banking Ombudsman SchemeSundar Babu50% (2)

- RESERVE BANK INTEGRATED OMBUDSMAN SCHEME PROCEDURESDocument20 pagesRESERVE BANK INTEGRATED OMBUDSMAN SCHEME PROCEDURESBhaveshkumar SangadaPas encore d'évaluation

- RBI-Note Refund Rules-Revised Guidelines140909Document29 pagesRBI-Note Refund Rules-Revised Guidelines140909sonali choudharyPas encore d'évaluation

- Banking Ombudsman: Ashwin Kunal SinghDocument9 pagesBanking Ombudsman: Ashwin Kunal SinghD PPas encore d'évaluation

- Policy 9Document27 pagesPolicy 9sachinash664Pas encore d'évaluation

- Banking Ombudsman: Mr. Indranil Banerjee (Faculty of Banking Law)Document15 pagesBanking Ombudsman: Mr. Indranil Banerjee (Faculty of Banking Law)Amit GroverPas encore d'évaluation

- Reserve Bank of India: Ombudsman Scheme For Digital Transactions, 2019Document27 pagesReserve Bank of India: Ombudsman Scheme For Digital Transactions, 2019Ankit AgarwalPas encore d'évaluation

- Banking Ombudsman Complaint ProcessDocument8 pagesBanking Ombudsman Complaint ProcessManini JaiswalPas encore d'évaluation

- Guideline on Agent BankingDocument15 pagesGuideline on Agent Bankingco samPas encore d'évaluation

- OmbudsmanDocument21 pagesOmbudsmanRAYSPEARPas encore d'évaluation

- CIC Rules RegulationsDocument46 pagesCIC Rules RegulationsthanannjaiPas encore d'évaluation

- Short Title and Commencement: Opening of An Account at An Office of The Banking Department of The BankDocument12 pagesShort Title and Commencement: Opening of An Account at An Office of The Banking Department of The Bankayush_GARG1234567890Pas encore d'évaluation

- Banking Law ProjectDocument17 pagesBanking Law ProjectFaraz SiddiquiPas encore d'évaluation

- Reserve Bank Integrated Ombudsman SchemeDocument19 pagesReserve Bank Integrated Ombudsman SchemeNani AnugaPas encore d'évaluation

- Power of Reserve Bank To Control Advances by Banking CompaniesDocument3 pagesPower of Reserve Bank To Control Advances by Banking CompaniespodderPas encore d'évaluation

- PDIC ACT: KEY AMENDMENTS & FUNCTIONSDocument12 pagesPDIC ACT: KEY AMENDMENTS & FUNCTIONSAmorMeaThereseMendozaPas encore d'évaluation

- Branch Licensing PolicyDocument10 pagesBranch Licensing Policyma_sadamPas encore d'évaluation

- Guideline On Provision and Distribution of Financial Products - ENGDocument33 pagesGuideline On Provision and Distribution of Financial Products - ENGsrinuindian007Pas encore d'évaluation

- DoorDocument4 pagesDoorapi-3807149Pas encore d'évaluation

- Final Project 123.docx45Document45 pagesFinal Project 123.docx45tarerakeshPas encore d'évaluation

- (Appointment of Internal Ombudsman by Non-Banking Financial Companies - 126IONBFCSDocument7 pages(Appointment of Internal Ombudsman by Non-Banking Financial Companies - 126IONBFCSTUSHAR KRISHNAPas encore d'évaluation

- The Banking Companies Rules 1963Document4 pagesThe Banking Companies Rules 1963Jia BilalPas encore d'évaluation

- Powers of Reserve Bank of IndiaDocument9 pagesPowers of Reserve Bank of IndiaPayalRajputPas encore d'évaluation

- Procedure For ParticipationDocument3 pagesProcedure For Participationrajkumar0606Pas encore d'évaluation

- Banking MohtasibDocument5 pagesBanking MohtasibGujjarPas encore d'évaluation

- Banking Regulation Act.Document26 pagesBanking Regulation Act.ratneshiilm0% (1)

- Licensing and Supervision of Banking Business Directives To Authorize The Business of Interest Free Banking Directives Number SBB/51/2011Document3 pagesLicensing and Supervision of Banking Business Directives To Authorize The Business of Interest Free Banking Directives Number SBB/51/2011Afework AtnafsegedPas encore d'évaluation

- NBE Directives Raise Minimum Bank Capital RequirementsDocument7 pagesNBE Directives Raise Minimum Bank Capital RequirementsAfework Atnafseged100% (3)

- Winding Up Banking Company ProcedureDocument13 pagesWinding Up Banking Company ProcedureVinay KumarPas encore d'évaluation

- The Banking Ombudsman Scheme: Annual Report 2006-2007Document63 pagesThe Banking Ombudsman Scheme: Annual Report 2006-2007Deepesh AgrawalPas encore d'évaluation

- Banking Ombudsman Scheme in India: A Brief AnalysisDocument18 pagesBanking Ombudsman Scheme in India: A Brief AnalysisVicky DPas encore d'évaluation

- Winding Up of Banking CompanyDocument13 pagesWinding Up of Banking CompanySaurabh ModPas encore d'évaluation

- NBFC23022018Document17 pagesNBFC23022018RAMANAN MAGESHPas encore d'évaluation

- Bank Term Deposit Scheme, 2006Document4 pagesBank Term Deposit Scheme, 2006Sundar RajPas encore d'évaluation

- The Banking Ombudsman Scheme, 2002 Table of Contents PreliminaryDocument40 pagesThe Banking Ombudsman Scheme, 2002 Table of Contents PreliminaryRanjan Roy JacobPas encore d'évaluation

- Commercial Banking and Transnational Trade Finance in IndiaDocument56 pagesCommercial Banking and Transnational Trade Finance in IndiaArunav Guha Roy0% (1)

- Unit - 3 Structure and Formation of Bank and Financial InstitutionsDocument17 pagesUnit - 3 Structure and Formation of Bank and Financial InstitutionsAnkit AgarwalPas encore d'évaluation

- Final Abp Sonia Notice-Of-meeting May-2019Document7 pagesFinal Abp Sonia Notice-Of-meeting May-2019Quant_GeekPas encore d'évaluation

- Banking Act 2004 Act 673Document38 pagesBanking Act 2004 Act 673asafoabe4065100% (1)

- Rules and Regulations For Cooperative BanksDocument11 pagesRules and Regulations For Cooperative Banksfrescy mosterPas encore d'évaluation

- Assignment Fin815Document11 pagesAssignment Fin815sacheal unibenPas encore d'évaluation

- Banking Ombudsman Scheme ExplainedDocument5 pagesBanking Ombudsman Scheme ExplainedAkashPas encore d'évaluation

- Guidelines For Rural Banking LicenceDocument4 pagesGuidelines For Rural Banking LicenceKingston Nkansah Kwadwo EmmanuelPas encore d'évaluation

- Exchange Control - Foreign Exchange Bureaux de Change - OrdeDocument9 pagesExchange Control - Foreign Exchange Bureaux de Change - OrdeKelvin RugonyePas encore d'évaluation

- Maths FormulaDocument17 pagesMaths Formulaenjoy begening lifePas encore d'évaluation

- Banking OmbudsmanDocument4 pagesBanking OmbudsmanAshok SutharPas encore d'évaluation

- Fil-R-01 Mobile Financial Services Regulation Eng Final Website 4-4-2016 - 5Document10 pagesFil-R-01 Mobile Financial Services Regulation Eng Final Website 4-4-2016 - 5Maria MidiriPas encore d'évaluation

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanD'EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanPas encore d'évaluation

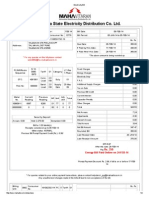

- Electricity BillDocument2 pagesElectricity Billrahuldbajaj2011Pas encore d'évaluation

- People vs. Sindiong and Pastor (77 Phil. 1000)Document2 pagesPeople vs. Sindiong and Pastor (77 Phil. 1000)Cherry Ann Cubelo NamocPas encore d'évaluation

- Natwestbank Basic AccountDocument12 pagesNatwestbank Basic AccountPmsakda HemthepPas encore d'évaluation

- OTB Notice 2020 08 20 19 15 50 176254Document4 pagesOTB Notice 2020 08 20 19 15 50 17625469j8mpp2scPas encore d'évaluation

- Rom2010augm27 893098023 602445287Document79 pagesRom2010augm27 893098023 602445287Mandar KubalPas encore d'évaluation

- Mudarabah Financing AgreementDocument8 pagesMudarabah Financing AgreementEthica Institute of Islamic Finance™100% (2)

- Beverly Perkins OIG ReportDocument439 pagesBeverly Perkins OIG ReportChris GothnerPas encore d'évaluation

- RBI Payment NotificationDocument1 pageRBI Payment Notificationvinay0717Pas encore d'évaluation

- On-Line Payment SercurityDocument5 pagesOn-Line Payment SercurityAvleen KhuranaPas encore d'évaluation

- Aefpm5487a 2023Document4 pagesAefpm5487a 2023enjoy enjoy enjoyPas encore d'évaluation

- Remittance 241109Document2 pagesRemittance 241109donal8123Pas encore d'évaluation

- ROI Based Training Needs Analysis: Diederick StoelDocument6 pagesROI Based Training Needs Analysis: Diederick StoelMelwyn BastianPas encore d'évaluation

- Hsbcuk Account Closure FormDocument6 pagesHsbcuk Account Closure FormZaid SolkarPas encore d'évaluation

- Impact of Information Technology in Accounting SystemDocument73 pagesImpact of Information Technology in Accounting SystemMichaelPas encore d'évaluation

- Site Rental 24 Dec 2021Document16 pagesSite Rental 24 Dec 2021Wega BluemartPas encore d'évaluation

- TAXATION SCHEMES EXPLAINEDDocument7 pagesTAXATION SCHEMES EXPLAINEDLeonard CañamoPas encore d'évaluation

- The Law of Negotiable Instruments: Learning ObjectivesDocument12 pagesThe Law of Negotiable Instruments: Learning ObjectivesHikmah EdiPas encore d'évaluation

- UntitledDocument8 pagesUntitledGreat WhizdomPas encore d'évaluation

- WSC2024 Packages v1.0Document42 pagesWSC2024 Packages v1.0magunPas encore d'évaluation

- Muscle Up Gym Financial ReportDocument1 pageMuscle Up Gym Financial ReportAlireza KafaeiPas encore d'évaluation

- Oblicon - Codal (1193-1220)Document3 pagesOblicon - Codal (1193-1220)Joan MaanoPas encore d'évaluation

- How Much Do You Owe? $46.60 Here's A Breakdown of Your TotalDocument4 pagesHow Much Do You Owe? $46.60 Here's A Breakdown of Your TotalMuhammad NaeemPas encore d'évaluation

- Electronic Payment SystemDocument5 pagesElectronic Payment Systemsudeep1907100% (1)

- Obligations NotesDocument22 pagesObligations NotesVivian BulataoPas encore d'évaluation

- Expense Manager User GuideDocument15 pagesExpense Manager User Guidegbg@polka.co.zaPas encore d'évaluation

- Banking ProjectDocument21 pagesBanking Projectjigna kelaPas encore d'évaluation

- List of Documents For TrustDocument4 pagesList of Documents For TrustSunil SoniPas encore d'évaluation

- Cards Schedule ChargesDocument1 pageCards Schedule ChargesRaju ReddyPas encore d'évaluation

- Pgm2017 ProsDocument76 pagesPgm2017 ProsAnto PaulPas encore d'évaluation