Vous aimerez peut-être aussi

- The Future of Your Wealth: How the World Is Changing and What You Need to Do about It: A Guide for High Net Worth Individuals and FamiliesD'EverandThe Future of Your Wealth: How the World Is Changing and What You Need to Do about It: A Guide for High Net Worth Individuals and FamiliesPas encore d'évaluation

- The Ultimate Guide to US Financial Regulations: A Primer for Lawyers and Business ProfessionalsD'EverandThe Ultimate Guide to US Financial Regulations: A Primer for Lawyers and Business ProfessionalsPas encore d'évaluation

- Treasury Research News Bulletin - 27 November 2013Document2 pagesTreasury Research News Bulletin - 27 November 2013r3iherPas encore d'évaluation

- Zztreasury Research - Daily - Global and Asia FX - April 29 2013Document2 pagesZztreasury Research - Daily - Global and Asia FX - April 29 2013r3iherPas encore d'évaluation

- Broadway Industrial Group: Singapore Company Flash NoteDocument3 pagesBroadway Industrial Group: Singapore Company Flash NoteTerence Seah Pei ChuanPas encore d'évaluation

- State Bank of India: Play On Economic Recovery Buy MaintainedDocument4 pagesState Bank of India: Play On Economic Recovery Buy MaintainedPaul GeorgePas encore d'évaluation

- Treasury Research News Bulletin - 25 October 2013Document2 pagesTreasury Research News Bulletin - 25 October 2013r3iherPas encore d'évaluation

- Lendlease Global Commercial REIT: 2Q FY2020 Financial ResultsDocument23 pagesLendlease Global Commercial REIT: 2Q FY2020 Financial ResultsKerie ThamPas encore d'évaluation

- First Resources: Singapore Flash NoteDocument4 pagesFirst Resources: Singapore Flash NotephuawlPas encore d'évaluation

- KFH Research Turkey Focus 2012 A Strained YearDocument2 pagesKFH Research Turkey Focus 2012 A Strained YearkhalidgnPas encore d'évaluation

- StartVII Marketing PresentationDocument33 pagesStartVII Marketing PresentationMartin KoPas encore d'évaluation

- UpdateDocument6 pagesUpdatemtwang100% (1)

- Blog - Fed Watch Nifty FiftyDocument3 pagesBlog - Fed Watch Nifty FiftyOwm Close CorporationPas encore d'évaluation

- Global Macro Commentary July 14Document2 pagesGlobal Macro Commentary July 14dpbasicPas encore d'évaluation

- Long Term Wave Count in IOCDocument4 pagesLong Term Wave Count in IOCanon_483049492Pas encore d'évaluation

- Earnings-Presentation Q4fy2019 01 enDocument61 pagesEarnings-Presentation Q4fy2019 01 enBen HartmannPas encore d'évaluation

- 2013-7-9 DBS Lim&TanDocument6 pages2013-7-9 DBS Lim&TanphuawlPas encore d'évaluation

- IDFC - Poor Start To Q3 - Dec 12, 2014Document5 pagesIDFC - Poor Start To Q3 - Dec 12, 2014KCPas encore d'évaluation

- ESS - Analyst Day Presentation 8 30 21Document43 pagesESS - Analyst Day Presentation 8 30 21Elena DanilaPas encore d'évaluation

- AmBank FX Daily OutlookDocument3 pagesAmBank FX Daily Outlookr3iherPas encore d'évaluation

- IDirect RBIActions Feb16Document4 pagesIDirect RBIActions Feb16umaganPas encore d'évaluation

- Sum of The Charts: "Trading Places": Technical AnalysisDocument31 pagesSum of The Charts: "Trading Places": Technical AnalysisArtur SilvaPas encore d'évaluation

- Auto 03jun16 MoslDocument4 pagesAuto 03jun16 Moslravi285Pas encore d'évaluation

- Weekly EquitiesDocument2 pagesWeekly EquitiesDhirendra KumarPas encore d'évaluation

- 2010 Interim Results Release: 31 August 2010Document19 pages2010 Interim Results Release: 31 August 2010naderpourPas encore d'évaluation

- RBI Monetary Policy ReviewDocument4 pagesRBI Monetary Policy ReviewAngel BrokingPas encore d'évaluation

- Softbank PPT Shareholders-Meeting 40 07 enDocument62 pagesSoftbank PPT Shareholders-Meeting 40 07 enDaniel GoytrPas encore d'évaluation

- Global Market Update - 04 09 2015 PDFDocument6 pagesGlobal Market Update - 04 09 2015 PDFRandora LkPas encore d'évaluation

- Volatus Aerospace - November 22 PresentationDocument22 pagesVolatus Aerospace - November 22 PresentationTom ChoiPas encore d'évaluation

- Snapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)Document2 pagesSnapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)api-237906069Pas encore d'évaluation

- Tough Fight For Weekly Close: Punter's CallDocument3 pagesTough Fight For Weekly Close: Punter's CallPraveenPas encore d'évaluation

- Important Note On These Presentation Slides, Including The Use of non-IFRS Financial InformationDocument69 pagesImportant Note On These Presentation Slides, Including The Use of non-IFRS Financial InformationAnonymous d2ZSDEPas encore d'évaluation

- Third Quarter 2016 Investment Outlook: Asset Class SectorDocument6 pagesThird Quarter 2016 Investment Outlook: Asset Class SectorAnonymous DJrec2Pas encore d'évaluation

- Beat FDs With US Treasuries - Century FinancialDocument9 pagesBeat FDs With US Treasuries - Century FinancialRayan WarnerPas encore d'évaluation

- Final Wave of Consolidation: Punter's CallDocument4 pagesFinal Wave of Consolidation: Punter's CallAnonymous cCns05JRPas encore d'évaluation

- Snapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)Document2 pagesSnapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)api-237906069Pas encore d'évaluation

- Snapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)Document2 pagesSnapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)api-237906069Pas encore d'évaluation

- IMP Investor Presentation Apr 2020Document40 pagesIMP Investor Presentation Apr 2020Capital AdvisorPas encore d'évaluation

- AmBank FX Weekly OutlookDocument5 pagesAmBank FX Weekly Outlookr3iherPas encore d'évaluation

- Broadway Industrial: Singapore Result SnapshotDocument3 pagesBroadway Industrial: Singapore Result SnapshotTerence Seah Pei ChuanPas encore d'évaluation

- ISJ Wockhardt Update October 2011Document3 pagesISJ Wockhardt Update October 2011Hardik JainPas encore d'évaluation

- ANZ Banking ReportDocument4 pagesANZ Banking ReportMathewDunckleyPas encore d'évaluation

- Chart Watch: Sterling - On Key LevelsDocument11 pagesChart Watch: Sterling - On Key LevelstimurrsPas encore d'évaluation

- Yes Bank - EnamDocument3 pagesYes Bank - Enamdeepak1126Pas encore d'évaluation

- Snapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)Document2 pagesSnapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)api-237906069Pas encore d'évaluation

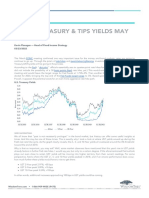

- Blog - Where Treasury TIPS Yields May Be HeadedDocument5 pagesBlog - Where Treasury TIPS Yields May Be HeadedOwm Close CorporationPas encore d'évaluation

- USD Wealth Premier 2023 Fund: February 2014 Investment ObjectiveDocument1 pageUSD Wealth Premier 2023 Fund: February 2014 Investment ObjectiveErwin Dela CruzPas encore d'évaluation

- Mid-Quarter Monetary Policy ReviewDocument3 pagesMid-Quarter Monetary Policy ReviewAngel BrokingPas encore d'évaluation

- MTF (BSPL) Stock Pick - TATASTEEL - 17102023Document3 pagesMTF (BSPL) Stock Pick - TATASTEEL - 17102023riddhi SalviPas encore d'évaluation

- Cappuccino Notes: An Investment Offering A Enhanced Exposure To A Portfolio of Underlying AssetsDocument3 pagesCappuccino Notes: An Investment Offering A Enhanced Exposure To A Portfolio of Underlying AssetsLameunePas encore d'évaluation

- EWM Fund 2 FactsheetDocument2 pagesEWM Fund 2 FactsheetNicky TsaiPas encore d'évaluation

- Intermediate Bond Strategy HSPDocument2 pagesIntermediate Bond Strategy HSPLoganBohannonPas encore d'évaluation

- Midas290711-Flashnote Buy DBSVDocument3 pagesMidas290711-Flashnote Buy DBSVkei00Pas encore d'évaluation

- Interest Rates InflationDocument3 pagesInterest Rates InflationHans WidjajaPas encore d'évaluation

- Technical Stock PickDocument3 pagesTechnical Stock PickGauriGanPas encore d'évaluation

- Daily Market Update 21.10.2013Document2 pagesDaily Market Update 21.10.2013Randora LkPas encore d'évaluation

- Snapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)Document2 pagesSnapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)api-237906069Pas encore d'évaluation

- Economy: Sep-13 Inflation Clocked in at 7.39% Yoy: He EllDocument2 pagesEconomy: Sep-13 Inflation Clocked in at 7.39% Yoy: He ElljibranqqPas encore d'évaluation

- Sunrise Shareholder Information DocumentDocument455 pagesSunrise Shareholder Information DocumentCalimeroPas encore d'évaluation

- China September CPIDocument4 pagesChina September CPIAnonymous Ht0MIJPas encore d'évaluation

- Features: Tracking TechnicalDocument3 pagesFeatures: Tracking TechnicalbodaiPas encore d'évaluation

- Sawasdee SET: S-T Retracement, Opportunity To BuyDocument14 pagesSawasdee SET: S-T Retracement, Opportunity To BuybodaiPas encore d'évaluation

- TH Property Sector Update 20180509Document5 pagesTH Property Sector Update 20180509bodaiPas encore d'évaluation

- Morning Brief - E - 2018103918368Document18 pagesMorning Brief - E - 2018103918368bodaiPas encore d'évaluation

- TH Consumer and Hospitality Sector Update 20180509 RHBDocument14 pagesTH Consumer and Hospitality Sector Update 20180509 RHBbodaiPas encore d'évaluation

- Energy & Power 1Q19 PDFDocument25 pagesEnergy & Power 1Q19 PDFbodaiPas encore d'évaluation

- Mark-To-Actual Revision of Lower Provision, But Headwind Trend RemainsDocument11 pagesMark-To-Actual Revision of Lower Provision, But Headwind Trend RemainsbodaiPas encore d'évaluation

- TH Property Sector Update 20180509Document5 pagesTH Property Sector Update 20180509bodaiPas encore d'évaluation

- Morning Brief - E - 20170726093031Document25 pagesMorning Brief - E - 20170726093031bodaiPas encore d'évaluation

- Sawasdee: Support: 1575, 1570 Resistance: 1585. 1590 Market StrategyDocument10 pagesSawasdee: Support: 1575, 1570 Resistance: 1585. 1590 Market StrategybodaiPas encore d'évaluation

- Company Report - IMPACT - E - 20180219081453Document8 pagesCompany Report - IMPACT - E - 20180219081453bodaiPas encore d'évaluation

- Morning Brief - E - 20170721100634Document24 pagesMorning Brief - E - 20170721100634bodaiPas encore d'évaluation

- Morning Breif - E - 20170801095547Document22 pagesMorning Breif - E - 20170801095547bodaiPas encore d'évaluation

- ImagesDocument9 pagesImagesbodaiPas encore d'évaluation

- Big PursuitDocument8 pagesBig PursuitbodaiPas encore d'évaluation

- Sawasdee: Support: 1575, 1570 Resistance: 1585. 1590 Market StrategyDocument10 pagesSawasdee: Support: 1575, 1570 Resistance: 1585. 1590 Market StrategybodaiPas encore d'évaluation

- ImagesDocument11 pagesImagesbodaiPas encore d'évaluation

- ImagesDocument11 pagesImagesbodaiPas encore d'évaluation

- Morning Brief - E - 20170222092647Document27 pagesMorning Brief - E - 20170222092647bodaiPas encore d'évaluation

- ImagesDocument6 pagesImagesbodaiPas encore d'évaluation

- Sci FinestDocument8 pagesSci FinestbodaiPas encore d'évaluation

- Fish or Cut BaitDocument10 pagesFish or Cut BaitbodaiPas encore d'évaluation

- Bangkok Chain Hospital: A New Lease of LifeDocument11 pagesBangkok Chain Hospital: A New Lease of LifebodaiPas encore d'évaluation

- Time Will PassDocument43 pagesTime Will PassbodaiPas encore d'évaluation

- Sawasdee: Support: 1575, 1565 Resistance: 1580, 1590 MarketDocument10 pagesSawasdee: Support: 1575, 1565 Resistance: 1580, 1590 MarketbodaiPas encore d'évaluation

- 20161223092340Document3 pages20161223092340bodaiPas encore d'évaluation

- ImagesDocument8 pagesImagesbodaiPas encore d'évaluation

- The Erawan Group: Book Now, Good Price GuaranteedDocument10 pagesThe Erawan Group: Book Now, Good Price GuaranteedbodaiPas encore d'évaluation

- 20161223175636Document26 pages20161223175636bodaiPas encore d'évaluation

- Aps Lit@tb 110615 93817Document2 pagesAps Lit@tb 110615 93817bodaiPas encore d'évaluation

- NASA: 45607main NNBE Interim Report1 12-20-02Document91 pagesNASA: 45607main NNBE Interim Report1 12-20-02NASAdocumentsPas encore d'évaluation

- Extent of Small Scale Fish Farming in Three DistriDocument13 pagesExtent of Small Scale Fish Farming in Three DistriMartin Ayoba MubusoPas encore d'évaluation

- Cash-Handling Policy: IntentDocument3 pagesCash-Handling Policy: IntentghaziaPas encore d'évaluation

- Intel Corporation Analysis: Strategical Management - Tengiz TaktakishviliDocument12 pagesIntel Corporation Analysis: Strategical Management - Tengiz TaktakishviliSandro ChanturidzePas encore d'évaluation

- Interpretive Dance RubricDocument1 pageInterpretive Dance RubricWarren Sumile67% (3)

- RPMDocument35 pagesRPMnisfyPas encore d'évaluation

- The List of Official United States National SymbolsDocument3 pagesThe List of Official United States National SymbolsВікторія АтаманюкPas encore d'évaluation

- OpenELIS Lab Data - Admin Guide (For Bahmni)Document6 pagesOpenELIS Lab Data - Admin Guide (For Bahmni)Hiến LưuPas encore d'évaluation

- A Game Is A Structured Form of PlayDocument5 pagesA Game Is A Structured Form of PlayNawa AuluddinPas encore d'évaluation

- Rguhs Dissertation Titles 2015Document5 pagesRguhs Dissertation Titles 2015PaySomeoneToWriteAPaperForMeSingapore100% (1)

- Case 1 - Mr. ReyesDocument3 pagesCase 1 - Mr. ReyesJasper Andrew AdjaraniPas encore d'évaluation

- Precontraint 502S2 & 702S2Document1 pagePrecontraint 502S2 & 702S2Muhammad Najam AbbasPas encore d'évaluation

- 1 Reviewing Number Concepts: Coursebook Pages 1-21Document2 pages1 Reviewing Number Concepts: Coursebook Pages 1-21effa86Pas encore d'évaluation

- Josephine Morrow: Guided Reflection QuestionsDocument3 pagesJosephine Morrow: Guided Reflection QuestionsElliana Ramirez100% (1)

- Ethereum WorldDocument41 pagesEthereum WorldHarihara Gopalan SPas encore d'évaluation

- Where The Boys Are (Verbs) : Name Oscar Oreste Salvador Carlos Date PeriodDocument6 pagesWhere The Boys Are (Verbs) : Name Oscar Oreste Salvador Carlos Date PeriodOscar Oreste Salvador CarlosPas encore d'évaluation

- WHO SOPs Terms DefinitionsDocument3 pagesWHO SOPs Terms DefinitionsNaseem AkhtarPas encore d'évaluation

- Cone Penetration Test (CPT) Interpretation: InputDocument5 pagesCone Penetration Test (CPT) Interpretation: Inputstephanie andriamanalinaPas encore d'évaluation

- Offsites Engineering Works For The Erbil Refinery 40,000 B/D Expansion ProjectDocument12 pagesOffsites Engineering Works For The Erbil Refinery 40,000 B/D Expansion ProjectSardar PerdawoodPas encore d'évaluation

- Becg Unit-1Document8 pagesBecg Unit-1Bhaskaran Balamurali0% (1)

- The Apollo Parachute Landing SystemDocument28 pagesThe Apollo Parachute Landing SystemBob Andrepont100% (2)

- Econ 281 Chapter02Document86 pagesEcon 281 Chapter02Elon MuskPas encore d'évaluation

- Spring 2021 NBME BreakdownDocument47 pagesSpring 2021 NBME BreakdownUmaPas encore d'évaluation

- Problematical Recreations 5 1963Document49 pagesProblematical Recreations 5 1963Mina, KhristinePas encore d'évaluation

- Peralta v. Philpost (GR 223395, December 4, 2018Document20 pagesPeralta v. Philpost (GR 223395, December 4, 2018Conacon ESPas encore d'évaluation

- Rajiv Gandhi Govt. Polytechnic Itanagar (A.P) : Web Page DesigningDocument13 pagesRajiv Gandhi Govt. Polytechnic Itanagar (A.P) : Web Page Designingkhoda takoPas encore d'évaluation

- FR Cayat Vs COMELEC PDFDocument38 pagesFR Cayat Vs COMELEC PDFMark John Geronimo BautistaPas encore d'évaluation

- Presentation2 Norman FosterDocument10 pagesPresentation2 Norman FosterAl JhanPas encore d'évaluation

- Marimba ReferenceDocument320 pagesMarimba Referenceapi-3752991Pas encore d'évaluation

- Shell Aviation: Aeroshell Lubricants and Special ProductsDocument12 pagesShell Aviation: Aeroshell Lubricants and Special ProductsIventPas encore d'évaluation