Vous aimerez peut-être aussi

- Extreme Buildings Resistant To Seismic ForcesDocument2 pagesExtreme Buildings Resistant To Seismic ForcesSuryasis DasguptaPas encore d'évaluation

- Fast Food Restaurant Business Plan - Financial PlanDocument20 pagesFast Food Restaurant Business Plan - Financial PlanSuryasis DasguptaPas encore d'évaluation

- Concrete Wall in Tropical ClimateDocument11 pagesConcrete Wall in Tropical ClimateSuryasis DasguptaPas encore d'évaluation

- Fast Food Restaurant Business Plan - Strategy and Implementation SummaryDocument18 pagesFast Food Restaurant Business Plan - Strategy and Implementation SummarySuryasis Dasgupta67% (3)

- Concrete Foundations For Tropical ClimatesDocument6 pagesConcrete Foundations For Tropical ClimatesSuryasis DasguptaPas encore d'évaluation

- Farm Structure in Tropical ClimateDocument10 pagesFarm Structure in Tropical ClimateSuryasis DasguptaPas encore d'évaluation

- Illustration Showing The EarthDocument1 pageIllustration Showing The EarthSuryasis DasguptaPas encore d'évaluation

- India Weather Extremes 3rd Week of SeptDocument1 pageIndia Weather Extremes 3rd Week of SeptSuryasis DasguptaPas encore d'évaluation

- Pavement Design Concepts-Flexible PavementsDocument3 pagesPavement Design Concepts-Flexible PavementsSuryasis DasguptaPas encore d'évaluation

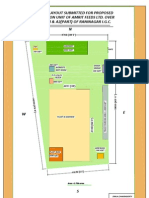

- Plant Layout For Proposed Extension at RaninagarDocument1 pagePlant Layout For Proposed Extension at RaninagarSuryasis DasguptaPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- A Step by Step Guide For Loans AUPDocument2 pagesA Step by Step Guide For Loans AUPDerek RobbinsPas encore d'évaluation

- Eastern Bank Limited: Name: ID: American International University of Bangladesh Course Name: Faculty Name: Due DateDocument6 pagesEastern Bank Limited: Name: ID: American International University of Bangladesh Course Name: Faculty Name: Due DateTasheen MahabubPas encore d'évaluation

- Nuru Ethiopia Final Audit Report 2019Document22 pagesNuru Ethiopia Final Audit Report 2019Elias Abubeker AhmedPas encore d'évaluation

- 19 Ways To Find Fast Cash, More Savings - NerdWalletDocument10 pages19 Ways To Find Fast Cash, More Savings - NerdWalletGeorgios MoulkasPas encore d'évaluation

- Bilal 009Document3 pagesBilal 009Zed ZaryabPas encore d'évaluation

- 362 End Term FRA SecDDocument5 pages362 End Term FRA SecDkhushali goharPas encore d'évaluation

- (Financial Accounting & Reporting 2) : Lecture AidDocument20 pages(Financial Accounting & Reporting 2) : Lecture AidMay Grethel Joy PerantePas encore d'évaluation

- Money & Banking - MGT411 HandoutsDocument149 pagesMoney & Banking - MGT411 HandoutstwinkllesPas encore d'évaluation

- Loan AgreementDocument19 pagesLoan AgreementR GautamPas encore d'évaluation

- CA Related Syllabus For 2024 - 2025Document4 pagesCA Related Syllabus For 2024 - 2025loganathanPas encore d'évaluation

- Intercompany Inventory Transactions: Mcgraw-Hill/Irwin © 2008 The Mcgraw-Hill Companies, Inc. All Rights ReservedDocument22 pagesIntercompany Inventory Transactions: Mcgraw-Hill/Irwin © 2008 The Mcgraw-Hill Companies, Inc. All Rights ReservedFarhan Osman ahmedPas encore d'évaluation

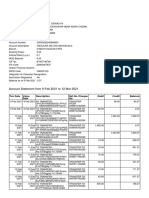

- Account Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceABHINAV DEWALIYAPas encore d'évaluation

- Key Investor Information: Objectives and Investment PolicyDocument2 pagesKey Investor Information: Objectives and Investment PolicyGeorgio RomaniPas encore d'évaluation

- Comparative Analysis On NBFC & Banks NPADocument33 pagesComparative Analysis On NBFC & Banks NPABHAVESH KHOMNEPas encore d'évaluation

- The Mortgage Forgiveness Debt Relief Act and Debt CancellationDocument3 pagesThe Mortgage Forgiveness Debt Relief Act and Debt CancellationPeter Smothers100% (1)

- Book AnswersDocument7 pagesBook AnswersIza ValdezPas encore d'évaluation

- Section 1 - 5Document18 pagesSection 1 - 5Shiela71% (7)

- Sec Cert Sample - Bank AcctDocument2 pagesSec Cert Sample - Bank AcctJennifer Peng NavarretePas encore d'évaluation

- Primary MarketDocument23 pagesPrimary MarketSneha KansalPas encore d'évaluation

- At A Glance Corporate Fact SheetDocument4 pagesAt A Glance Corporate Fact SheetpanchoPas encore d'évaluation

- Westpac Feb4Document2 pagesWestpac Feb4რაქსშ საჰა100% (1)

- Total Current Liabilities: Balance Sheet of Pidilite Industries - in Rs. Cr.Document4 pagesTotal Current Liabilities: Balance Sheet of Pidilite Industries - in Rs. Cr.Vishal GargPas encore d'évaluation

- International Accounting Standard CommitteeDocument2 pagesInternational Accounting Standard Committeeshamrat ronyPas encore d'évaluation

- Shashank Mhadnak: Regular Updating Technical KnowledgeDocument4 pagesShashank Mhadnak: Regular Updating Technical KnowledgeAmit KalsiPas encore d'évaluation

- Assignment - Funds and Other InvestmentsDocument2 pagesAssignment - Funds and Other InvestmentsJane DizonPas encore d'évaluation

- ECGCDocument22 pagesECGCchandran0567Pas encore d'évaluation

- Important: Compound Interest QuestionsDocument12 pagesImportant: Compound Interest QuestionsShraiya ManhasPas encore d'évaluation

- Assignment of Insurance LawDocument11 pagesAssignment of Insurance LawHarish KeluskarPas encore d'évaluation

- What Is Cryptocurrency - CoinbaseDocument2 pagesWhat Is Cryptocurrency - Coinbaseatina tehreemPas encore d'évaluation

- Getting Started With GST Unit 2 8 Mark QuestionsDocument2 pagesGetting Started With GST Unit 2 8 Mark Questionsmanoharchary157Pas encore d'évaluation