Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Social Cognitive Theory - BanduraDocument9 pagesSocial Cognitive Theory - BanduraJiss Palelil100% (1)

- Fundamentals of Accountancy, Business and Management 1Document20 pagesFundamentals of Accountancy, Business and Management 1Lhana Denise100% (5)

- The Rothschilds Stage Revolutions in Tunisia and EgyptDocument10 pagesThe Rothschilds Stage Revolutions in Tunisia and EgyptZeka Sumerian OutlawPas encore d'évaluation

- Chapter 11 - Part 1 - Accounting FranchisesDocument13 pagesChapter 11 - Part 1 - Accounting FranchisesJane Dizon100% (1)

- Cost and Benefit Analysis BookDocument361 pagesCost and Benefit Analysis Book9315875729100% (7)

- Hawk Hardware Store - ProblemDocument17 pagesHawk Hardware Store - ProblemAngelo Labios50% (2)

- Icici Bank Financial AnalysisDocument46 pagesIcici Bank Financial AnalysisPiyush Goyal88% (8)

- Chapter No.17Document5 pagesChapter No.17Kamal SinghPas encore d'évaluation

- 4.3.2.5 Elaborate - Determining AdjustmentsDocument4 pages4.3.2.5 Elaborate - Determining AdjustmentsMa Fe Tabasa0% (1)

- Project of Merger Acquisition SANJAYDocument65 pagesProject of Merger Acquisition SANJAYmangundesanju77% (74)

- Valuing Environmental Impacts: Practical Guidelines For The Use of Value Transfer in Policy and Project AppraisalDocument10 pagesValuing Environmental Impacts: Practical Guidelines For The Use of Value Transfer in Policy and Project AppraisalJiss PalelilPas encore d'évaluation

- 1540644reporting Statistics in APA FormatReporting Statistics in APA FormatDocument9 pages1540644reporting Statistics in APA FormatReporting Statistics in APA FormatJiss PalelilPas encore d'évaluation

- Job Description: Risk/Internal Audit: About EYDocument6 pagesJob Description: Risk/Internal Audit: About EYJiss PalelilPas encore d'évaluation

- Logit Models NotesDocument29 pagesLogit Models Notesnikola001Pas encore d'évaluation

- Agri Econ ModelsDocument23 pagesAgri Econ ModelsJiss PalelilPas encore d'évaluation

- 82 CommonarticulationDocument2 pages82 Commonarticulationramyameena321Pas encore d'évaluation

- Financial Management: Iv Sem - Bcom Chapter - 2 Financing DecisionsDocument5 pagesFinancial Management: Iv Sem - Bcom Chapter - 2 Financing DecisionsJiss PalelilPas encore d'évaluation

- MfsReporting Statistics in APA FormatReporting Statistics in APA FormatReporting Statistics in APA FormatReporting Statistics in APA FormatDocument8 pagesMfsReporting Statistics in APA FormatReporting Statistics in APA FormatReporting Statistics in APA FormatReporting Statistics in APA FormatJiss PalelilPas encore d'évaluation

- Reporting Statistics in APA FormatDocument3 pagesReporting Statistics in APA FormatJiss PalelilPas encore d'évaluation

- 27623ipcc CA Vol1 InitialpagesFinancial Management Chapter-2Document17 pages27623ipcc CA Vol1 InitialpagesFinancial Management Chapter-2Jiss PalelilPas encore d'évaluation

- Voluntary Winding Up in India-A Comparative Analysis: Cia IiiDocument6 pagesVoluntary Winding Up in India-A Comparative Analysis: Cia IiiJiss PalelilPas encore d'évaluation

- Balance of PowerDocument11 pagesBalance of PowerJiss PalelilPas encore d'évaluation

- Income Tax Department Conducts Raids Against Chettinad Group of CompaniesDocument4 pagesIncome Tax Department Conducts Raids Against Chettinad Group of CompaniesJiss PalelilPas encore d'évaluation

- GST tAADFSRFSADocument2 pagesGST tAADFSRFSAJiss PalelilPas encore d'évaluation

- Eco Oooo FSDFSDFSDDocument1 pageEco Oooo FSDFSDFSDJiss PalelilPas encore d'évaluation

- The Political Brain - Bijo Thomas Ittiarah - 1424007Document1 pageThe Political Brain - Bijo Thomas Ittiarah - 1424007Jiss PalelilPas encore d'évaluation

- PeerDocument10 pagesPeerJiss PalelilPas encore d'évaluation

- Questions - Rebate On Bills DiscountedDocument4 pagesQuestions - Rebate On Bills DiscountedJiss Palelil0% (1)

- PDF Party Od ofDocument3 pagesPDF Party Od ofJiss PalelilPas encore d'évaluation

- PeerDocument10 pagesPeerJiss PalelilPas encore d'évaluation

- Group 2 MediaDocument3 pagesGroup 2 MediaJiss PalelilPas encore d'évaluation

- Foreign PolicyDocument9 pagesForeign PolicyJiss PalelilPas encore d'évaluation

- Case 08A 9s Is The Ither TwermDocument1 pageCase 08A 9s Is The Ither TwermJiss PalelilPas encore d'évaluation

- Abnormal PsychologyDocument2 pagesAbnormal PsychologyJiss PalelilPas encore d'évaluation

- Instruments of Foreign PolicyDocument5 pagesInstruments of Foreign PolicyJiss PalelilPas encore d'évaluation

- Theories of Personality: Sudhesh N.TDocument79 pagesTheories of Personality: Sudhesh N.TJiss PalelilPas encore d'évaluation

- Diplomacy of PreseDocument14 pagesDiplomacy of PreseJiss PalelilPas encore d'évaluation

- Case Study Vijay Mallya - Another Big NaDocument10 pagesCase Study Vijay Mallya - Another Big Najai sri ram groupPas encore d'évaluation

- BUSI 3309 W24 Assignment 1Document6 pagesBUSI 3309 W24 Assignment 1faridahrushdy5Pas encore d'évaluation

- Average Age of InventoryDocument10 pagesAverage Age of Inventoryrakeshjha91Pas encore d'évaluation

- Junior Accountant RoleDocument1 pageJunior Accountant RoleRICARDO PROMOTIONPas encore d'évaluation

- CL-07 ApplicantDocument29 pagesCL-07 ApplicantShivamp6Pas encore d'évaluation

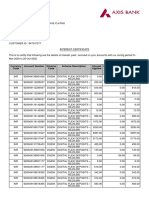

- Interest CertificateDocument2 pagesInterest CertificatesumitPas encore d'évaluation

- Zabala Auto SupplyDocument7 pagesZabala Auto SupplyLeighsen VillacortaPas encore d'évaluation

- Conceptual Framework PPT 090719 PDFDocument53 pagesConceptual Framework PPT 090719 PDFSheena OroPas encore d'évaluation

- FM Project HDFCDocument14 pagesFM Project HDFCsameer_kiniPas encore d'évaluation

- Explanatory Notes For The Completion of Vat Return FormDocument3 pagesExplanatory Notes For The Completion of Vat Return FormTendai ZamangwePas encore d'évaluation

- Chapter 21 The Influence of Monetary and Fiscal Policy On Aggregate DemandDocument50 pagesChapter 21 The Influence of Monetary and Fiscal Policy On Aggregate DemandRafiathsPas encore d'évaluation

- GenMath FormulasDocument2 pagesGenMath FormulasWendy Mae Lapuz100% (1)

- Futures' Bhavcopy Analyser - Setup 1Document6 pagesFutures' Bhavcopy Analyser - Setup 1Sreenivas GuduruPas encore d'évaluation

- New Investment Supports SkySparc Growth StrategyDocument3 pagesNew Investment Supports SkySparc Growth StrategyPR.comPas encore d'évaluation

- Mutual Funds - IntroductionDocument9 pagesMutual Funds - IntroductionMd Zainuddin IbrahimPas encore d'évaluation

- COGM5 Final RequirementDocument24 pagesCOGM5 Final RequirementLadignon IvyPas encore d'évaluation

- W.C PPT by MeDocument70 pagesW.C PPT by Meramr9000Pas encore d'évaluation

- Alanis Parks Department: Analyze and Chart Financial DataDocument7 pagesAlanis Parks Department: Analyze and Chart Financial DataJacob SheridanPas encore d'évaluation

- Form 16Document6 pagesForm 16Pulkit Gupta100% (1)

- Financial Institution & Investment Management - Final ExamDocument5 pagesFinancial Institution & Investment Management - Final Exambereket nigussie100% (4)

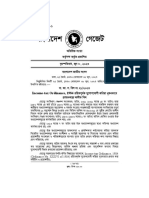

- Bangladesh Gazette - Income Tax Act 2023Document319 pagesBangladesh Gazette - Income Tax Act 2023khaled mosharofPas encore d'évaluation

- Chapter 6 Exclusions From Gross Income PDFDocument12 pagesChapter 6 Exclusions From Gross Income PDFkimberly tenebroPas encore d'évaluation