Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Winter Semester 2015 16 - Course Allocation ReportDocument18 pagesWinter Semester 2015 16 - Course Allocation ReportVijay VarmanPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- 7c of Ecommerce Britannia and ITCDocument6 pages7c of Ecommerce Britannia and ITCVijay VarmanPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- M&A Bharati Airtel ZaineDocument4 pagesM&A Bharati Airtel ZaineVijay VarmanPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- International Business: Individual AssignmentDocument7 pagesInternational Business: Individual AssignmentVijay VarmanPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- 14MBA0146 - History - 27 03 2015 - 17 12 13Document2 pages14MBA0146 - History - 27 03 2015 - 17 12 13Vijay VarmanPas encore d'évaluation

- About Vit University:: Who We AreDocument2 pagesAbout Vit University:: Who We AreVijay VarmanPas encore d'évaluation

- Thế Giới Di Động 2022Document14 pagesThế Giới Di Động 2022Phạm Thu HằngPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Topic2 Part1Document16 pagesTopic2 Part1Abdul MoezPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Accounting Process: Name: Date: Professor: Section: Score: QuizDocument6 pagesThe Accounting Process: Name: Date: Professor: Section: Score: QuizAllyna Jane Enriquez100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Psak 72 10 Minutes PDFDocument2 pagesPsak 72 10 Minutes PDFMentari AndiniPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Fintelum Opens Investment Into New Tokenisation Project KEEPPDocument3 pagesFintelum Opens Investment Into New Tokenisation Project KEEPPPR.comPas encore d'évaluation

- Module 3Document22 pagesModule 3Suprita Karajgi100% (1)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Deutsche Finan ExcelDocument6 pagesDeutsche Finan ExcelAnonymous VVSLkDOAC1Pas encore d'évaluation

- Birla Sun Life InsuranceDocument17 pagesBirla Sun Life InsuranceKenen BhandhaviPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Assumptions:: Financial FeasibilityDocument3 pagesAssumptions:: Financial FeasibilityHassanRanaPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Mergers, EtcDocument4 pagesMergers, EtcflorynmarianPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Types of StrategiesDocument15 pagesTypes of Strategiesmayaverma123pPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Control of Administrative, Selling and Distribution OverheadDocument17 pagesControl of Administrative, Selling and Distribution OverheadBhavik AmbaniPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- MRK - Fall 2019 - HRM630 - 1 - MC180203268Document2 pagesMRK - Fall 2019 - HRM630 - 1 - MC180203268Z SulemanPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- JOD13969Document2 pagesJOD13969Abhishek SinghviPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Consolidated Financial Statements Dec 312012Document60 pagesConsolidated Financial Statements Dec 312012Inamullah KhanPas encore d'évaluation

- ASSIGNMENT ms2 Ra PDFDocument2 pagesASSIGNMENT ms2 Ra PDFBeomi0% (1)

- U.S. Individual Income Tax Return: Filing StatusDocument14 pagesU.S. Individual Income Tax Return: Filing StatusDavid Dautel100% (1)

- MAA716 - T2 - 2012 v2Document11 pagesMAA716 - T2 - 2012 v2ssusasi4769Pas encore d'évaluation

- Amalgmation, Absorbtion, External ReconstructionDocument12 pagesAmalgmation, Absorbtion, External Reconstructionpijiyo78Pas encore d'évaluation

- Cryptocurrencies and Blockchain Technology - The Future of FinanceDocument14 pagesCryptocurrencies and Blockchain Technology - The Future of FinanceBenjo HodzicPas encore d'évaluation

- Advance Accounting Installment Sales Manual MillanDocument14 pagesAdvance Accounting Installment Sales Manual MillanHades AcheronPas encore d'évaluation

- EPS Bootstrapping Bootstrap Earnings e EctDocument2 pagesEPS Bootstrapping Bootstrap Earnings e Ecthyba ben helalPas encore d'évaluation

- Mutual Funds PerformanceDocument7 pagesMutual Funds PerformanceAli RazaPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Inflation With Capital BudgetingDocument10 pagesInflation With Capital BudgetingRUMA AKTERPas encore d'évaluation

- Annex K-Bank Reconciliation Statement PDFDocument12 pagesAnnex K-Bank Reconciliation Statement PDFRg Abulkhayr Lawi GuilingPas encore d'évaluation

- XLS EngDocument21 pagesXLS EngRudra BarotPas encore d'évaluation

- "The Way To Make Easy: Hardest Money" 2.0Document74 pages"The Way To Make Easy: Hardest Money" 2.0А. Ариунбаяр86% (21)

- Summer Internship Report On Indian Stock MarketsDocument18 pagesSummer Internship Report On Indian Stock Marketssujayphatak070% (1)

- Preventing Sickkness and Rehabilitation of Business UnitsDocument46 pagesPreventing Sickkness and Rehabilitation of Business Unitsmurugesh_mbahit100% (13)

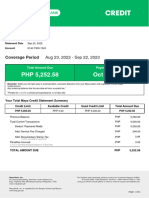

- MayaCredit SoA 2023SEPDocument3 pagesMayaCredit SoA 2023SEPjepoy palaruanPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)