Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- What Is Paper-And-Pencil-Tests?Document3 pagesWhat Is Paper-And-Pencil-Tests?IrenePas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Auditing in CIS EnvironmentDocument14 pagesAuditing in CIS EnvironmentLino GumpalPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Auditing in A CIS EnvironmentDocument10 pagesAuditing in A CIS EnvironmentLailanie AcordaPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- Learning ContentDocument3 pagesLearning ContentIrenePas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- ASD Top 4 Mitigation Strategies - List of Software - This Component Provides A Common Application Vendors - Vulnerability Summary - This Component DisplaysDocument2 pagesASD Top 4 Mitigation Strategies - List of Software - This Component Provides A Common Application Vendors - Vulnerability Summary - This Component DisplaysIrenePas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Multiple Choice QuestionsDocument25 pagesMultiple Choice QuestionsJohn Remar Lavina70% (20)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Managing GovernanceDocument2 pagesManaging GovernanceIrenePas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Auditing in CIS EnvironmentDocument1 pageAuditing in CIS EnvironmentIrenePas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Auditing in A CIS EnvironmentDocument10 pagesAuditing in A CIS EnvironmentLailanie AcordaPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- Tenable Network SecurityDocument2 pagesTenable Network SecurityIrenePas encore d'évaluation

- AngelicaDocument5 pagesAngelicaIrenePas encore d'évaluation

- Include PictureDocument1 pageInclude PictureIrenePas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- 1221 4835 1 PB PDFDocument10 pages1221 4835 1 PB PDFIrenePas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- 200Document5 pages200IrenePas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- HHHDocument1 pageHHHIrenePas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- HiiiiiDocument1 pageHiiiiiIrenePas encore d'évaluation

- KKKKDocument1 pageKKKKIrenePas encore d'évaluation

- Philippine Financial Reporting Standard1Document22 pagesPhilippine Financial Reporting Standard1IrenePas encore d'évaluation

- Affirmative ActionDocument1 pageAffirmative ActionIrenePas encore d'évaluation

- 102 Test No. 3 Solutions KeeperDocument19 pages102 Test No. 3 Solutions KeeperIrenePas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Philippine Financial Reporting Standards-2Document13 pagesPhilippine Financial Reporting Standards-2IrenePas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- 202E06Document21 pages202E06foxstupidfoxPas encore d'évaluation

- Student AssesmentDocument1 pageStudent AssesmentKing VegetaPas encore d'évaluation

- Adhalat BillDocument2 pagesAdhalat BillShravan SinghPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

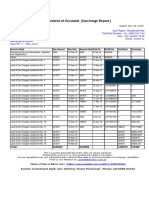

- Surcharge Report BTKSC-P05164Document1 pageSurcharge Report BTKSC-P05164Nasir Badshah AfridiPas encore d'évaluation

- Member List 2021 22 (South - Zone)Document33 pagesMember List 2021 22 (South - Zone)Business PartnerzPas encore d'évaluation

- School Fees 2023Document1 pageSchool Fees 2023Janet NdakalakoPas encore d'évaluation

- FMEA - HCI CONSOLE FLOOR - LHD OKDocument20 pagesFMEA - HCI CONSOLE FLOOR - LHD OKManikandanPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Scaffolding Calculation - Sep-Nov 2019Document2 pagesScaffolding Calculation - Sep-Nov 2019bayuPas encore d'évaluation

- Acuerdo de Comisión Techking Begatell 2020.11.05Document4 pagesAcuerdo de Comisión Techking Begatell 2020.11.05Jenn medinaPas encore d'évaluation

- Cote D' Ivoire StudyDocument62 pagesCote D' Ivoire StudyAli AbdoulayePas encore d'évaluation

- Animal Purchase ContractDocument2 pagesAnimal Purchase ContractScribdTranslationsPas encore d'évaluation

- MDM Empty Formats For Andhra PradeshDocument5 pagesMDM Empty Formats For Andhra PradeshTittu Vijay Bonthu100% (2)

- SOCIAL STUDIES PRACTICE TESTDocument3 pagesSOCIAL STUDIES PRACTICE TESTAnilGoyalPas encore d'évaluation

- Business Plan Evaluation FormDocument5 pagesBusiness Plan Evaluation Formvhle67Pas encore d'évaluation

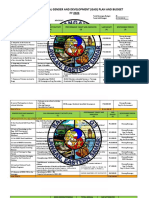

- Barangay Annual Gender and Development (Gad) Plan and Budget FY 2023Document3 pagesBarangay Annual Gender and Development (Gad) Plan and Budget FY 2023Joy Tiozon100% (2)

- Fencing Supplies QuotationDocument1 pageFencing Supplies QuotationHiltonPas encore d'évaluation

- Fixed Deposits - November 22 2021Document1 pageFixed Deposits - November 22 2021Lisle Daverin BlythPas encore d'évaluation

- Economics - Elasticity Grade 12 SHSDocument14 pagesEconomics - Elasticity Grade 12 SHSTanya MiyaPas encore d'évaluation

- Oblicon ContractsDocument2 pagesOblicon ContractsLeo Sandy Ambe CuisPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Basic Engineering Economy PrinciplesDocument10 pagesBasic Engineering Economy PrinciplesCarmela Andrea BuenafePas encore d'évaluation

- Home Office and BranchDocument9 pagesHome Office and BranchLive LovePas encore d'évaluation

- Pastel Accounting 1Document309 pagesPastel Accounting 1Mthunzi Xulu100% (3)

- Optimal Decisions Using Marginal AnalysisDocument6 pagesOptimal Decisions Using Marginal AnalysisShoyo Hinata100% (1)

- Market Structure and Game Theory (Part 4)Document7 pagesMarket Structure and Game Theory (Part 4)Srijita GhoshPas encore d'évaluation

- Simple Moving AverageDocument6 pagesSimple Moving AverageHendrawan SaputroPas encore d'évaluation

- @RTA Market PsychologyDocument10 pages@RTA Market PsychologyPerfect Seboke100% (1)

- Waltham Motors CaseDocument2 pagesWaltham Motors CasetclarkskyPas encore d'évaluation

- 1 Evolution of ManagementDocument56 pages1 Evolution of ManagementYASH SANJAY.INGLEPas encore d'évaluation

- Review - Practical Accounting 1Document2 pagesReview - Practical Accounting 1yes yesnoPas encore d'évaluation

- Pass Book - RWPDocument29 pagesPass Book - RWPpunjab food authority RawalpindiPas encore d'évaluation

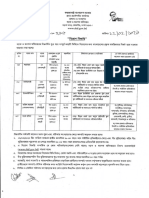

- CircularDocument3 pagesCircularOmar FarukPas encore d'évaluation

- The Fabric of Civilization: How Textiles Made the WorldD'EverandThe Fabric of Civilization: How Textiles Made the WorldÉvaluation : 4.5 sur 5 étoiles4.5/5 (57)

- Sully: The Untold Story Behind the Miracle on the HudsonD'EverandSully: The Untold Story Behind the Miracle on the HudsonÉvaluation : 4 sur 5 étoiles4/5 (103)

- Dirt to Soil: One Family’s Journey into Regenerative AgricultureD'EverandDirt to Soil: One Family’s Journey into Regenerative AgricultureÉvaluation : 5 sur 5 étoiles5/5 (124)

- Faster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestD'EverandFaster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestÉvaluation : 4 sur 5 étoiles4/5 (28)

- Recording Unhinged: Creative and Unconventional Music Recording TechniquesD'EverandRecording Unhinged: Creative and Unconventional Music Recording TechniquesPas encore d'évaluation